Fact-checked by the CapitalLendingNews editorial team

In the third quarter of 2024, portfolio loans accounted for roughly 31.5% of new mortgage originations, up from under 25% in 2022, according to Urban Institute data. That growth is not a coincidence. Rising home prices and a sharp increase in self-employed borrowers have pushed a growing share of creditworthy Americans outside the boundaries of conforming loan guidelines, forcing them to seek financing from lenders who set their own rules. For many of these borrowers, understanding the portfolio loan mortgage rate structure is the difference between securing a property and walking away empty-handed.

The core tension is this: the Federal Housing Finance Agency set the 2024 baseline conforming loan limit at $766,550 for single-unit properties, with a high-cost area ceiling of $1,149,825. Any mortgage above those thresholds cannot be purchased by Fannie Mae or Freddie Mac, effectively excluding it from the conventional secondary market. But it is not just loan size that causes problems. Conventional underwriting also requires W-2 income documentation, caps financed investment properties at 10, and prohibits interest-only or balloon structures under CFPB Qualified Mortgage rules. A retiree with $5 million in investments and $60,000 in documented annual income can be a worse mortgage candidate on paper than a schoolteacher earning $80,000 a year.

This article lays out exactly how portfolio loans differ from conventional mortgages in structure and cost, what drives the rate premium and by how much, when paying that premium is defensible, and how high-asset borrowers can negotiate the best terms available. You will leave with a clear framework for deciding which product actually fits your situation and a concrete action plan for finding the right lender.

Key Takeaways

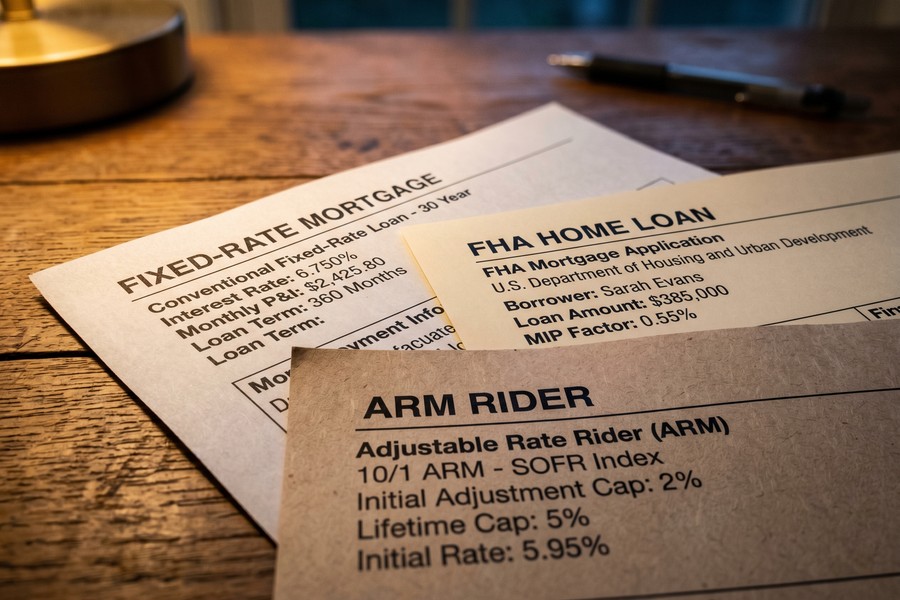

- The 2024 FHFA conforming loan limit is $766,550 for single-unit properties; any mortgage above this threshold becomes non-conforming and must be held in a lender’s portfolio or structured as a jumbo loan.

- Portfolio loan mortgage rates typically run 0.5 to 2 percentage points above conventional rates; on a $300,000 loan, that spread adds $175 to $420 per month and $50,000 to $150,000 in total interest over 30 years.

- A high-credit borrower with a 60% loan-to-value ratio can often secure a portfolio loan near 6.75%, while a borrower with complex financials at higher LTV may land at 8.5%, a 1.75-point spread within portfolio products alone.

- Conventional Fannie Mae guidelines cap financed investment properties at 10; portfolio and blanket loans carry no such ceiling, making them the only viable path for investors who have hit that limit.

- Asset depletion divisors vary by lender from 60 to 120 months, meaning the same $2 million portfolio can qualify a borrower for anywhere from $1.2 million to $1.8 million depending on methodology, so rate shopping alone is insufficient.

- Under CFPB Qualified Mortgage rules, conventional conforming loans cannot include interest-only periods, balloon payments, or negative amortization; portfolio loans can offer all three, which is a structural flexibility that sophisticated borrowers can use strategically.

In This Guide

- Why High-Asset Borrowers Often Cannot Get a Conventional Loan

- What a Portfolio Loan Mortgage Rate Actually Buys You

- The Asset Depletion Workaround: Qualifying Without W-2 Income

- Rate Structure Comparison: Fixed, Interest-Only, and Balloon Terms

- Where Portfolio Loan Rates Come From and How to Negotiate Them

- Portfolio Loans for Real Estate Investors: The Property Limit Problem

- Honest Cost-Benefit Framework: When the Higher Rate Is Worth It

- How to Find and Vet a Portfolio Lender as a High-Asset Borrower

Why High-Asset Borrowers Often Cannot Get a Conventional Loan

The paradox is frustrating but straightforward: conventional mortgage underwriting was built around the W-2 employee. Fannie Mae and Freddie Mac guidelines assess creditworthiness primarily through adjusted gross income documented by pay stubs and tax returns. A borrower with $5 million in investment accounts but $60,000 in reported AGI (after business deductions or retirement withdrawals) will often show a debt-to-income ratio above the 43% threshold that most conventional programs require, triggering a denial despite substantial net worth. The system measures cash flow, not wealth.

Several borrower profiles run into this ceiling repeatedly. Retirees drawing from brokerage accounts rather than receiving a pension show minimal “income” on paper. Self-employed business owners who run legitimate deductions through their returns reduce their taxable income to a fraction of what they actually control. Trust beneficiaries receive distributions that vary year to year and don’t fit neatly into income averaging formulas. Real estate investors who already own multiple financed properties hit the conforming property count cap before they can expand their portfolios further.

The Self-Employed Write-Off Trap

For self-employed borrowers, the same tax strategy that reduces their IRS liability works against them at the loan application stage. A business owner who reports $450,000 in gross receipts but deducts $350,000 in legitimate expenses shows $100,000 in AGI. On a $2 million home, the resulting debt-to-income ratio eliminates conventional eligibility, not because the borrower lacks resources but because the documentation method doesn’t align with the underwriting model. This is one of the main reasons the non-QM and portfolio loan market has expanded significantly over the past two years.

Understanding how your debt-to-income ratio affects your loan application is essential before approaching any lender, conventional or otherwise. Knowing your DTI going in prevents surprises at underwriting and helps you frame the conversation with a portfolio lender accurately.

Fannie Mae’s standard guidelines allow financing on up to 10 properties simultaneously for investment purposes, but most conventional lenders internally cap clients at 4 financed properties before requiring jumbo or portfolio alternatives. The gap between policy and practice catches many investors off guard.

Property Count Ceiling: A Hard Wall for Investors

For real estate investors, the property count ceiling is often the most concrete barrier. Conventional programs funded through the secondary market cap financed investment properties at 4 under most lender overlays and at 10 under Fannie Mae’s maximum guidelines. Once an investor hits that ceiling, a portfolio or blanket loan is not a preference, it is the only avenue available. No amount of strong credit or large down payment changes that math under conforming rules.

What a Portfolio Loan Mortgage Rate Actually Buys You

A portfolio loan is any mortgage that a lender originates and retains on its own balance sheet rather than selling into the secondary market. Because the lender is not bound by Fannie Mae, Freddie Mac, or FHA purchase requirements, it can set its own underwriting criteria, accept alternative income documentation, offer non-standard loan structures, and approve borrowers that conforming guidelines would reject. The rate premium reflects the lender’s higher risk of holding an asset that cannot be easily offloaded.

That premium is real and worth quantifying precisely. At 0.5 to 2 percentage points above a comparable conventional rate, the cost on a $300,000 loan ranges from $175 to $420 per month in additional principal and interest payments. Stretched over 30 years, that gap compounds to somewhere between $50,000 and $150,000 in total additional interest paid. On a $1 million loan, the numbers are proportionally larger and should factor into any decision that treats portfolio financing as a long-term hold rather than a bridge to conventional refinancing.

Portfolio vs. Jumbo vs. Non-QM: Getting the Terms Straight

One of the most common points of confusion in this space is that “portfolio loan,” “jumbo loan,” and “non-QM loan” are frequently used interchangeably, when in fact they describe overlapping but distinct categories. A jumbo loan is defined by size: any mortgage exceeding the FHFA conforming loan limit. A jumbo loan can be either a conventional product (if it meets all GSE underwriting criteria except size) or a portfolio product. A non-QM loan is defined by its deviation from CFPB Qualified Mortgage standards. Some portfolio loans are QM-compliant; many are not. The term “portfolio loan” itself refers to the retention method, not the loan’s features or regulatory status.

This distinction matters because rate comparisons break down if you conflate the terms. A well-documented jumbo loan from a large bank may carry a rate only 0.25 points above conventional. An asset depletion or DSCR-based portfolio loan from a community bank or non-QM lender may carry a rate 1.5 to 2 points higher. Comparing them as though they are the same product produces misleading conclusions.

Portfolio loans accounted for approximately 31.5% of new mortgage originations in Q3 2024, up from under 25% in 2022, reflecting rising home prices and the growth of self-employed and investor borrower segments that conventional underwriting cannot serve.

| Loan Type | Rate vs. Conventional | Key Features | Typical Borrower Profile |

|---|---|---|---|

| Conventional Conforming | Baseline | 30-yr fixed, GSE-backed, QM-compliant | W-2 employee, standard DTI |

| Jumbo (Bank-Held) | +0.10% to +0.50% | Exceeds $766,550 limit, full-doc | High earner, strong income docs |

| Portfolio (Asset Depletion) | +0.50% to +1.50% | Alt-income qualification, non-QM eligible | Retiree, investor, trust beneficiary |

| Portfolio (DSCR) | +0.75% to +2.00% | Rental income-based, no personal income check | Real estate investor |

| Blanket Portfolio Loan | +1.00% to +2.50% | Multiple properties, one note | Landlord with 5+ properties |

The Asset Depletion Workaround: Qualifying Without W-2 Income

For borrowers who have substantial investment assets but limited documented income, asset depletion methodology (sometimes called asset dissipation) offers a path forward. The concept is straightforward: the lender divides a borrower’s verified liquid assets by a defined number of months to arrive at a hypothetical monthly income figure, which is then used to calculate DTI. A $2 million portfolio divided by 120 months produces a $16,667 monthly qualifying income. That same portfolio divided by 60 months doubles the figure to $33,333.

The divisor matters enormously, and it varies by lender. Some community banks and non-QM lenders use 60 months; others use 84 or 120. That variation alone explains why two lenders reviewing identical financial statements can qualify the same borrower for a $1.2 million mortgage at one institution and a $1.8 million mortgage at another. Rate shopping is necessary, but it is insufficient on its own. You also need to compare the underwriting methodology, because the qualifying loan amount is just as important as the rate attached to it.

Which Assets Count and How They’re Discounted

Not all assets receive equal treatment under asset depletion programs. Cash and cash equivalents are typically credited at 100% of face value. Taxable brokerage accounts generally receive 80 to 100% credit. Retirement accounts such as IRAs and 401(k)s are usually discounted to 60 to 70% because of the tax liability and early withdrawal penalties associated with liquidation. Life insurance cash value may be counted at 70 to 80%. Cryptocurrency holdings, when accepted at all, are discounted to 50 to 60% given their price volatility.

Irrevocable trusts present a particular challenge. If the borrower does not control the principal, most lenders exclude it entirely from asset depletion calculations. Revocable living trusts where the borrower retains full control are treated more favorably, often at the same rate as other liquid assets.

The Double-Counting Trap

One detail that trips up borrowers and even some advisors is the double-counting problem: any assets earmarked for down payment, closing costs, and required reserves must be subtracted from the pool before the depletion calculation begins. A borrower who plans to put $500,000 down on a $2 million home, with $30,000 in closing costs and six months of reserves, may need to set aside $600,000 before the asset depletion clock starts. If their total investment portfolio is $1.5 million, only $900,000 is eligible for the calculation, producing a very different qualifying income than the gross portfolio value suggests. This surprise at underwriting is one of the most common and avoidable planning failures in the high-net-worth mortgage process.

Do not run asset depletion estimates using your total portfolio value. You must subtract funds committed to the down payment, closing costs, and required post-closing reserves before calculating your qualifying income. Using the gross figure inflates expectations and leads to underwriting surprises that can delay or kill a purchase.

Rate Structure Comparison: Fixed, Interest-Only, and Balloon Terms

Conventional conforming loans exist within a narrow structural range, by design. Under CFPB Qualified Mortgage guidelines, these loans cannot include negative amortization, interest-only periods, or balloon payments. The protection is real and meaningful for typical consumers who need predictable long-term amortization. For high-asset borrowers, however, those same constraints can be counterproductive.

Portfolio loans face no such structural prohibition. They can be written as 30-year fixed, 15-year fixed, adjustable-rate, interest-only for 5 to 10 years, or balloon loans due in 7 to 10 years. That flexibility is simultaneously the most powerful tool and the most significant risk in the product category.

Why a High-Asset Borrower Might Prefer Interest-Only

The conventional wisdom is that interest-only loans are dangerous because the borrower builds no equity. For most borrowers, that is correct. For a high-net-worth borrower, the calculation runs differently. If a borrower’s after-tax investment portfolio is generating an 8% annual return and their mortgage rate is 7%, the rational capital allocation is to keep money deployed in the portfolio rather than paying down principal. An interest-only period preserves liquidity and keeps capital working in higher-yield positions. The same logic that governs business capital structure applies here.

This is not a strategy suited to every high-asset borrower. It requires genuine liquidity, discipline, and a realistic assessment of investment return assumptions. But the availability of the interest-only structure through portfolio lending is a legitimate wealth management tool that competitors in this space consistently overlook. Understanding the relationship between loan term structure and total interest cost is critical before choosing any amortization schedule.

Balloon Structures: Planned Exit or Hidden Risk

A balloon mortgage requires full repayment of the remaining principal at a defined future date, typically 5, 7, or 10 years. For a borrower who expects to sell the property within that window, or who anticipates refinancing into a conventional product once their income documentation improves, the lower rate on a balloon structure may make sense. The risk is real: if the property hasn’t appreciated, if rates have risen, or if the borrower’s financial situation has deteriorated, the balloon payment can force a sale or default at the worst possible time. Any borrower considering a balloon structure needs a clear, specific exit plan before signing.

| Structure | Monthly Payment (per $1M) | QM Eligible | Best For | Key Risk |

|---|---|---|---|---|

| 30-Yr Fixed | ~$6,650 at 7.0% | Yes | Long-term hold, income stability | Opportunity cost of locked capital |

| 15-Yr Fixed | ~$8,988 at 6.75% | Yes | Accelerated payoff | Higher monthly cash demand |

| 10-Yr Interest-Only | ~$5,833 at 7.0% (interest only) | No | Liquidity preservation, capital deployment | No equity build, payment shock at reset |

| 7-Yr Balloon | ~$6,391 at 6.75% | No | Short-term hold, planned refinance | Refinancing risk at maturity |

| 5/1 ARM Portfolio | ~$5,996 at 6.25% initial | Potentially | Rate-sensitive investors | Adjustment risk after fixed period |

Where Portfolio Loan Rates Come From and How to Negotiate Them

There is no centralized exchange for portfolio loan rates. Unlike the conventional market, where Fannie Mae and Freddie Mac pricing grids create a transparent baseline, portfolio lenders price individually based on their cost of funds, balance sheet capacity, loan characteristics, and the value they assign to the overall banking relationship. Two lenders reviewing the same borrower and property can quote rates 100 basis points apart. That variance makes disciplined comparison-shopping a core part of the process, not an afterthought.

Community banks and credit unions are the most common source of true portfolio lending. They originate loans they intend to hold, build pricing around depositor relationships, and are frequently willing to customize terms for high-value clients who will place substantial assets under management with the institution. Some of the most competitive portfolio loan rates available in October 2024 are not advertised publicly; they surface through relationships, referrals, and mortgage brokers who specialize in non-QM and alternative documentation lending.

Negotiating Leverage Points

A high-asset borrower has more negotiating leverage than they typically realize. Loan-to-value ratio is the most powerful variable. A borrower coming in at 60% LTV (putting 40% down) represents substantially lower default risk than one at 80% LTV, and that differential should be reflected in the rate offered. In practice, the spread between a 60% LTV portfolio loan and one at 75 to 80% LTV can reach 100 to 175 basis points on its own.

Secondary leverage points include the depth of the existing banking relationship, the borrower’s debt service coverage ratio on any investment properties, and the willingness to place investable assets under management at the lending institution. Some lenders will reduce the mortgage rate by 25 to 50 basis points in exchange for moving $2 to $5 million in investment assets to their wealth management division. That tradeoff requires careful evaluation of investment management fees against the mortgage savings, but it can produce a genuinely better rate. Understanding how jumbo loan rates have shifted for high-balance borrowers following recent Fed decisions provides useful context when entering rate negotiations.

Before approaching a portfolio lender, calculate your loan-to-value ratio precisely and gather documentation showing your net worth well above the loan amount. Lenders price portfolio loans largely on perceived risk, and a clean presentation of a 55% to 60% LTV position with documented liquid reserves can shift the conversation from “can we approve this” to “what rate can we offer.”

What to Scrutinize Beyond the Rate

The headline rate is not the whole cost picture on a portfolio loan. Origination fees on portfolio and non-QM loans commonly run 1 to 3%, versus 0.5 to 1% on conventional mortgages. Prepayment penalties, which are prohibited on QM loans under CFPB rules but permissible on portfolio products, can add 1 to 3% of the outstanding balance if the borrower pays off or refinances within the first 3 to 5 years. And some lenders that market products as “portfolio loans” actually plan to sell them to third-party investors, which changes servicing arrangements, loan modification rights, and the nature of the lender relationship. Always ask directly whether the lender intends to retain the loan in-house for the life of the loan, and get the answer in writing.

Portfolio Loans for Real Estate Investors: The Property Limit Problem

For real estate investors, the property count ceiling is not a theoretical constraint. Fannie Mae’s conforming guidelines cap financed investment properties at 10, and many lenders apply stricter internal overlays that reduce that ceiling to 4 or 6 properties before requiring alternatives. Once an investor reaches the cap, conventional market access closes regardless of credit score, income, or equity position. Portfolio lending is not a preference at that point; it is the only available path.

Investors who have hit the conforming ceiling often encounter DSCR loans (debt service coverage ratio loans) as the primary portfolio product offered by non-QM lenders. These loans underwrite based on the property’s rental income rather than the borrower’s personal income. A property with $4,000 per month in rental income and a proposed mortgage payment of $3,000 per month carries a DSCR of 1.33, which meets the 1.25 minimum threshold most DSCR lenders require. No W-2, no tax returns, no personal income verification. The rate is higher, typically 1 to 2 points above conventional, but the structure solves the access problem that conforming guidelines create.

Blanket Loans: Consolidation With Trade-offs

Investors with 5 or more rental properties may encounter blanket loans, which consolidate multiple properties under a single note. The administrative simplicity is real: one payment, one lender relationship, one set of loan terms. The risk concentration is equally real. If the investor experiences financial difficulty, the lender has a security interest in all the properties simultaneously, making it harder to sell one asset to resolve a cash flow problem without triggering the cross-collateralization provisions. Blanket loans frequently carry the highest rate premiums in the portfolio loan category, 1 to 2.5 points above conventional, and prepayment provisions can be complex.

Landlords managing multiple properties should also review how renovation financing options for multi-property investors interact with existing portfolio loan covenants before taking on additional debt secured by the same collateral pool.

A real estate investor with 10 financed properties has reached Fannie Mae’s hard ceiling for conventional mortgages. Property 11 and beyond must be financed through portfolio lenders, DSCR programs, or commercial structures, regardless of the investor’s credit score or equity position.

Honest Cost-Benefit Framework: When the Higher Rate Is Worth It

The clearest decision rule is this: if you qualify for a conventional loan with full income documentation and a loan amount within conforming limits, the portfolio loan rate premium almost never justifies taking the portfolio product. The math rarely closes. On a $600,000 loan at a 1.5-point premium, the additional cost over 30 years exceeds $120,000. No borrower should pay that voluntarily when a conforming alternative is available.

The decision changes when conventional financing is simply not available. In that scenario, the “cost” of the portfolio loan premium is not an overpayment; it is the price of market access. The borrower’s alternative is not a cheaper loan, it is no loan. That reframe matters for how you evaluate the numbers. A portfolio loan that lets you acquire a property generating $5,000 per month in rental income is worth the rate premium if the net cash flow remains positive after the higher debt service.

The PMI Offset

One frequently missed calculation involves private mortgage insurance. Conventional loans below 20% down require PMI, which typically runs 0.5 to 1.5% of the loan amount annually, adding $125 to $375 per month on a $300,000 loan. Some portfolio lenders waive PMI entirely, even at 10 to 15% down, because they are setting their own credit guidelines and are not bound by GSE PMI requirements. In those cases, the portfolio loan’s rate premium may be partially or fully offset by the elimination of PMI, making the effective monthly cost closer to the conventional option than the rate comparison alone suggests. Always calculate total monthly cost, not just rate.

The Refinance Exit Strategy

Portfolio loans work best when treated as a stage in a longer financing plan, not a permanent solution. A self-employed borrower two years into a new business venture may not yet have two years of filed tax returns showing stable self-employment income, which conventional lenders require. A portfolio loan bridges that gap. Once the borrower has filed two years of returns with sufficient income, they can refinance into a conventional or conforming jumbo product and access the better rate. The question of whether to lock in today’s rates or wait for conditions to improve is worth revisiting at the point of any refinance decision.

Under the CFPB’s ability-to-repay framework, small creditors that retain loans in portfolio receive special Qualified Mortgage provisions, including an exemption from the standard 43% DTI limit. This regulatory pathway is one reason community banks can approve portfolio loans for high-asset borrowers that larger conventional lenders cannot touch.

| Scenario | Portfolio Loan Worth It? | Reasoning |

|---|---|---|

| Qualifies for conventional | No | Rate premium adds $50K–$150K over 30 years for no additional benefit |

| Self-employed, 1 year of returns | Yes, short-term | Bridge to conventional refinance after 2nd year of returns |

| 10th investment property | Yes, required | Conventional guidelines prohibit additional financed properties |

| Retiree, $4M portfolio, $55K AGI | Yes, possibly | Asset depletion may provide access; rate depends on LTV and methodology |

| Low LTV (<60%), strong DSCR | Often yes | Negotiated rate near 6.75% can be competitive; PMI elimination may offset premium |

| Foreign national buyer | Yes, required | No conventional options available; portfolio is the only path |

How to Find and Vet a Portfolio Lender as a High-Asset Borrower

Finding a portfolio lender is not like searching for a conventional rate quote. The best options are not always visible on comparison sites or advertised on lender websites. Community banks and credit unions with strong deposit bases are the most natural source; they have the balance sheet capacity to hold loans and the relationship-banking culture to offer custom terms. Many operate locally or regionally, which means geography matters more in this search than in conventional lending.

A mortgage broker who specializes in non-QM and alternative documentation lending is often the most efficient entry point. These brokers maintain relationships with 20 to 50 specialty lenders, including some that do no direct consumer advertising. They can present a borrower’s profile to multiple portfolio lenders simultaneously, surface competing offers, and compare not just rates but underwriting methodologies, fee structures, and servicing retention practices. The broker’s value in this market is substantially higher than in the conventional mortgage market, where rates are more commoditized.

Vetting a Portfolio Lender: Beyond the Rate Sheet

Before committing to any portfolio lender, ask four specific questions. First, does the lender retain the loan in its own portfolio for the life of the loan, or might it be sold to a third-party investor despite the “portfolio” label? Second, are there prepayment penalties, and if so, what is the structure (typically 3% in year 1, 2% in year 2, 1% in year 3, stepping down to zero)? Third, what are the origination fees as a percentage of the loan amount, and how do they compare to the present value of the rate difference versus a higher-rate product with no fees? Fourth, what happens if the lender’s financial condition changes? A smaller community bank holding a large portfolio of non-QM loans carries different counterparty risk than a well-capitalized credit union.

High-asset borrowers evaluating fixed versus adjustable structures should also review how fixed and adjustable rate loan structures differ for self-employed borrowers, as the considerations in that analysis translate directly to the portfolio loan context.

The CFPB’s ability-to-repay rules require portfolio lenders to make a reasonable, good-faith determination that the borrower can repay, even for non-QM loans. This means a portfolio lender cannot simply approve any borrower regardless of financial standing. The underwriting is flexible, but it is not absent.

| Lender Type | Typical Rate Range (Oct 2024) | Origination Fees | Prepayment Penalty | Best For |

|---|---|---|---|---|

| Community Bank | 6.75%–7.75% | 0.5%–1.5% | Rarely | Relationship borrowers, primary residence |

| Credit Union | 6.50%–7.50% | 0.5%–1.0% | Rarely | Members with existing accounts |

| Non-QM Specialty Lender | 7.25%–9.00% | 1.5%–3.0% | Common (3-2-1) | Alt-doc, investor, DSCR loans |

| Private / Hard Money | 9.00%–13.00% | 2.0%–5.0% | Variable | Short-term fix-and-flip or bridge |

| Wealth Mgmt. Division | 6.50%–7.25%* | 0.5%–1.0% | Rarely | UHNW clients placing assets with the bank |

*Rate reduction contingent on placing $2M+ in AUM with the lending institution’s wealth management division.

Some lenders market mortgages as “portfolio loans” while reserving the right to sell them to third-party investors after origination. If the loan is sold, your servicer may change, your relationship with the original lender may not protect you in a hardship scenario, and any rate concessions tied to an asset management relationship may not transfer. Always verify servicing retention in writing before closing.

Real-World Example: A Retiring Executive’s Path Through Asset Depletion Lending

Consider an illustrative example: a 62-year-old former technology executive who retired in early 2023 and is now purchasing a $1.8 million primary residence in a high-cost metropolitan area. Her liquid assets total $4.2 million across a taxable brokerage account ($2.4 million), a rollover IRA ($1.6 million), and cash savings ($200,000). Her documented AGI for 2023 was $78,000, entirely from IRA distributions and a small consulting retainer. She has no existing mortgage debt and a 790 credit score.

Her first application was to a large conventional lender. The proposed $1.44 million loan (20% down on a $1.8 million purchase) produced a debt-to-income ratio of 125% based on her documented income, leading to an automatic denial. She next approached three portfolio lenders through a non-QM mortgage broker. After subtracting the $360,000 down payment, $28,000 in estimated closing costs, and $120,000 in required six-month reserves from her eligible assets, the eligible pool for asset depletion was $2.47 million in the taxable account (discounted at 90% to $2.22 million) and $1.12 million in the IRA (discounted at 70% to $784,000), for a total of $3.0 million in eligible assets.

Lender A divided the $3.0 million by 120 months, producing a $25,000 monthly qualifying income and a DTI of 32% on the proposed loan, well within their 43% guideline. They quoted a 30-year fixed portfolio rate of 7.875% with 1.5 points, or a 10-year interest-only structure at 7.5% with 1.75 points. Lender B used a 84-month divisor, generating $35,714 in monthly qualifying income, a DTI of 22%, and a rate of 7.375% fixed for 30 years with 1.0 point. Lender C offered a relationship rate of 7.0% with 0.75 points if she moved $1.5 million in IRA assets to their wealth management platform, where advisory fees ran 0.85% annually.

After modeling all three scenarios, she selected Lender B’s 30-year fixed at 7.375% with 1.0 point. The all-in monthly payment was $9,933 on the $1.44 million loan. She also ran the numbers on waiting two years to document another $156,000 in IRA distributions annually, which would have allowed a conventional refinance at an estimated 7.0% rate, saving approximately $300 per month. Given her intent to hold the property for 15 or more years, she plans to refinance within 24 months once the income documentation supports a conforming jumbo application. The portfolio loan is a bridge, not a permanent structure, and entering it with that exit plan clearly defined is what makes the rate premium defensible.

Your Action Plan

-

Determine Whether You Actually Need a Portfolio Loan

Before pursuing portfolio financing, exhaust conventional options. Pull your most recent two years of tax returns and calculate your AGI. Check whether a jumbo conventional loan (full income documentation, loan amount above $766,550) might be available to you. If your documented DTI stays below 43% on the proposed payment, a conventional or conforming jumbo product will almost always produce a better rate. Portfolio lending should be the solution to a specific problem, not a default choice.

-

Map Your Asset Depletion Eligibility Accurately

List all liquid assets by type: cash, taxable brokerage, IRA/401(k), life insurance cash value, and any other eligible categories. Apply the discount rates lenders typically use (100% for cash, 80 to 90% for taxable brokerage, 60 to 70% for retirement accounts). Then subtract your estimated down payment, closing costs, and required post-closing reserves. The remaining figure is your eligible depletion base, which is what lenders will actually use in their calculations.

-

Calculate Your Target Loan Amount and LTV

Set your target loan amount based on the property purchase price and intended down payment. Compute the resulting LTV. If you can reach 60% LTV or below by adjusting your down payment, do so; the rate reduction is often 75 to 175 basis points, which more than offsets the opportunity cost of deploying additional capital at closing on most properties.

-

Engage a Non-QM Mortgage Broker, Not Just a Direct Lender

A broker with access to 20 or more non-QM and portfolio lenders can surface competing offers, compare asset depletion divisors and discount rates across institutions, and identify lenders willing to negotiate relationship-based rate reductions. The broker fee (typically 1 to 2% of the loan amount) is frequently recovered in the rate differential they negotiate relative to a single-lender direct application.

-

Compare Total Cost, Not Just Rate

For each lender offer, build a total cost model that includes the interest rate, origination points, other closing fees, any PMI obligations (or lack thereof), and prepayment penalty risk. Translate the rate difference into a total dollar figure over your expected holding period, not over 30 years if you plan to sell or refinance in 7 years. A 0.5-point lower rate with a 1.5-point prepayment penalty is a worse deal than a 0.25-point higher rate with no prepayment penalty if you plan to refinance within 3 years.

-

Confirm Servicing Retention and Loan Terms in Writing

Before signing any portfolio loan commitment, ask the lender directly whether the loan will be held in their portfolio for the life of the loan or whether it may be sold. Obtain the answer in the loan documents, not just in conversation. Also confirm the full terms of any prepayment penalty, the rate adjustment schedule on any variable-rate structure, and the balloon payment date and amount if applicable.

-

Build the Refinance Exit Timeline Into Your Plan

If your situation is temporary (new self-employment, one year of tax returns, recently inherited assets), set a specific date at which you will reassess conventional refinancing eligibility. For self-employed borrowers, that is usually 24 months after filing the second year of returns with sufficient income. Mark the date, track your documented income carefully in the interim, and work with a CPA who understands that your tax filing strategy affects your mortgage qualification as much as your tax liability.

-

Evaluate the Interest-Only Option Honestly

If a portfolio lender offers both a fully-amortizing and an interest-only structure, model both carefully. Compare the monthly payment difference against what you could realistically earn by keeping that capital deployed in your investment portfolio, net of taxes. If your portfolio is generating returns that genuinely exceed the mortgage rate after tax, the interest-only structure may be the more efficient choice. If your return assumptions are optimistic or the margin is thin, the fully-amortizing structure provides more certainty and equity accumulation.

Frequently Asked Questions

What is a portfolio loan mortgage rate and why is it higher than a conventional rate?

A portfolio loan mortgage rate is the interest rate charged on a mortgage that a lender originates and retains on its own balance sheet rather than selling to Fannie Mae, Freddie Mac, or another investor. Because the lender cannot offload the loan and recycle capital through the secondary market, it bears the full credit and liquidity risk. That retained risk is priced into the rate, typically at 0.5 to 2 percentage points above comparable conventional loans. The premium compensates the lender for setting its own underwriting standards and accepting borrowers or loan structures that the conforming market would not allow.

Are all jumbo loans portfolio loans?

No, and this is one of the most common points of confusion in mortgage research. A jumbo loan is defined purely by size: any mortgage above the FHFA conforming loan limit ($766,550 for most markets in 2024). Many jumbo loans are originated and sold to large private investors or held by major banks under their own jumbo programs with full income documentation and conventional-style underwriting. Those are not portfolio loans in the functional sense, even if they exceed conforming limits. A portfolio loan, by contrast, is any loan held in-house by the originating lender, regardless of size. The overlap is real but not complete.

How does asset depletion income qualification work for mortgage purposes?

Asset depletion methodology converts verified liquid assets into a hypothetical monthly income figure that lenders use to calculate debt-to-income ratio. The basic formula: total eligible assets divided by the lender’s chosen divisor (commonly 60, 84, or 120 months) equals qualifying monthly income. Asset types are discounted before the calculation: cash at 100%, taxable brokerage at 80 to 100%, retirement accounts at 60 to 70%, and so on. Critically, any assets committed to the down payment, closing costs, and required post-closing reserves must be excluded from the calculation before the divisor is applied.

Can I negotiate a portfolio loan mortgage rate?

Yes, and more directly than you can negotiate a conventional rate. Portfolio lenders price individually and weight factors like LTV, the depth of the banking relationship, and the borrower’s willingness to place assets under management at the institution. A borrower coming in at 60% LTV with a clean credit profile and existing deposit relationships has meaningful negotiating room. Getting competing offers from multiple lenders (through a non-QM broker) and presenting them to your preferred lender is a proven way to improve terms. Rate concessions of 25 to 75 basis points are achievable through active negotiation.

What happens at the end of a balloon payment portfolio loan?

At maturity of a balloon loan, the full remaining principal balance becomes due. If the borrower has not sold the property or refinanced before that date, they must either pay the balloon in full, negotiate a loan extension with the existing lender (not guaranteed), or refinance with a new lender. Refinancing risk is the central danger: if rates have risen substantially, if the property has declined in value, or if the borrower’s financial situation has weakened, the refinancing terms may be unfavorable or unavailable. Balloon structures are appropriate only when the borrower has a specific, credible exit plan in place before origination.

Do portfolio loans have prepayment penalties?

Many do, though it varies by lender and product type. Conventional conforming loans and government loans (FHA, VA) cannot legally include prepayment penalties under federal consumer protection rules. Portfolio loans are not subject to those prohibitions if structured as non-QM products. Common prepayment penalty structures are stepped: 3% of the outstanding balance in year 1, 2% in year 2, and 1% in year 3, declining to zero thereafter. On a $1 million loan, a year-1 penalty represents $30,000, which is a significant cost if you refinance or sell sooner than expected. Read the prepayment terms before signing, not after.

How many investment properties can I finance with a conventional loan?

Fannie Mae guidelines allow a single borrower to finance up to 10 investment properties simultaneously, but many individual lenders apply stricter internal overlays that cap the number at 4 or 6 before requiring alternative products. Once you reach your lender’s financed property ceiling, you cannot use conventional financing for additional acquisitions regardless of your creditworthiness. Portfolio loans, DSCR loans, and blanket mortgage structures become the only viable paths for continuing to expand an investment property portfolio.

Is an interest-only portfolio loan a red flag?

Not inherently, though it requires clear-eyed analysis. Under CFPB Qualified Mortgage rules, conventional conforming loans cannot include interest-only periods. Portfolio loans can. For borrowers who need to minimize monthly cash outlay, or who are rationally choosing to keep capital deployed in higher-yielding investments rather than paying down mortgage principal, an interest-only period is a legitimate financial planning tool. The red flag is using an interest-only structure to qualify for a loan that the borrower cannot actually afford when the interest-only period ends and the payment resets to full amortization. Know exactly what your fully-amortizing payment will be and whether you can sustain it before choosing the interest-only structure.

Can a portfolio loan be refinanced into a conventional mortgage later?

Yes, and this is often the intended strategy. A borrower who takes a portfolio loan because they have only one year of self-employment returns on file can refinance into a conventional or conforming jumbo product once they have two years of returns showing stable income. Similarly, a retiree whose Social Security income increases, or who begins receiving consistent IRA distributions that can be documented, may qualify for conventional refinancing after 12 to 24 months. The portfolio loan bridges the gap; the conventional refinance captures the better long-term rate. Borrowers who plan this exit strategy from the start should specifically avoid portfolio loan structures that carry long prepayment penalty periods, since a 5-year prepayment penalty would prevent a refinance during the most logical window.

Should I use a mortgage broker or go directly to a portfolio lender?

For most high-asset borrowers seeking portfolio financing, a non-QM mortgage broker adds more value than a direct lender relationship does at the outset. Brokers maintain access to dozens of portfolio and non-QM lenders, can present your profile to multiple institutions simultaneously, compare both rates and underwriting methodologies (which differ significantly across lenders), and can surface lenders who do not advertise publicly. Once you have identified a preferred lender through the broker process, you may choose to establish a direct relationship for future transactions. But the initial search and competitive quoting process is nearly always more efficient through a broker with deep non-QM expertise than through a direct approach to two or three lenders.

Sources

- Federal Housing Finance Agency, FHFA Announces Conforming Loan Limit Values for 2024

- Consumer Financial Protection Bureau, What Is a Qualified Mortgage?

- Consumer Financial Protection Bureau, Ability-to-Repay and Qualified Mortgage: Guide for Lenders

- Freddie Mac Single-Family, Loan Limit Values for 2024

- Consumer Financial Protection Bureau, ATR/QM Small Entity Compliance Guide

- Federal Reserve, Selected Interest Rates (H.15 Release)

- Internal Revenue Service, Publication 590-B: Distributions from Individual Retirement Arrangements

- Capital Lending News, How Jumbo Loan Interest Rates Have Shifted for High-Balance Borrowers Since the Fed’s Last Move

- Capital Lending News, Fixed vs Adjustable Rate Loans for Self-Employed Borrowers: Key Differences Explained

- Capital Lending News, Debt-to-Income Ratio on Digital Lending Platforms: The Number That Quietly Kills Your Application

- Capital Lending News, How Loan Term Length Quietly Controls How Much Interest You Actually Pay

- Capital Lending News, Should You Wait for Rates to Drop or Lock In What You Can Qualify For Today?