Fintech Small Business Loan Pricing in 2026: When the 14–99% APR Makes Sense

Fintech small business loans carry APRs of 14–99% versus 6.8–11% at banks. See when speed justifies the premium and when traditional lending wins.

Fintech small business loans carry APRs of 14–99% versus 6.8–11% at banks. See when speed justifies the premium and when traditional lending wins.

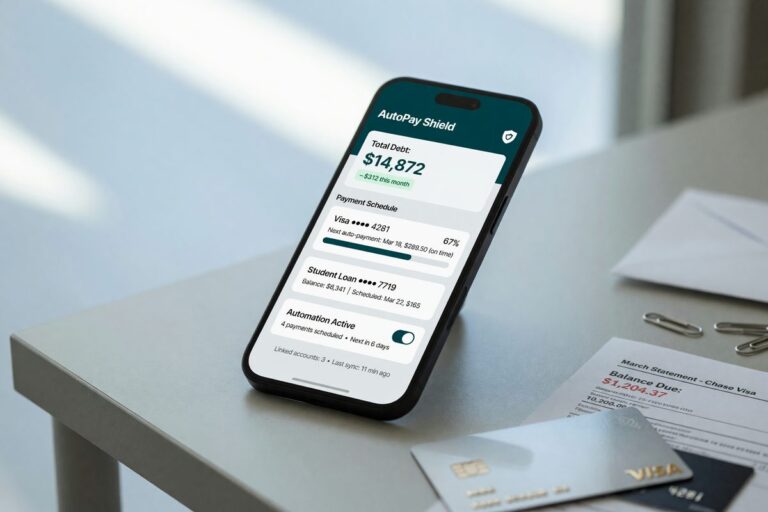

Automated fintech debt repayment pays off if you earn stable income and carry $5,000+ in debt—but app fees can erase savings faster than you think. See when it's worth it.

BNPL hit $156.7B in 2025 and earned wage access costs $1–$5 vs. 400% APR payday loans. See which fintech credit products match your actual cash problem.

Only 55% of single parents have savings for emergencies. See how fintech tools let you build a starter fund and tackle debt simultaneously without erasing progress.

Payroll advances cost less for one emergency, but repeat users hit APRs over 100%. Personal loans win if you need $500+ or multiple advances yearly.

A 620 credit score and applying within 60 days of peak earnings can make or break your approval. Here's how timing—not creditworthiness—determines your odds.

A $7.2 trillion market by 2030—embedded lending is reshaping how people borrow, skipping banks entirely through apps like Shopify and Uber.

Fintech algorithms cap most first-time borrowers at $10K–$15K, but a DTI below 36% and verified income can push your limit to $50,000 or more. Here's how the math works.

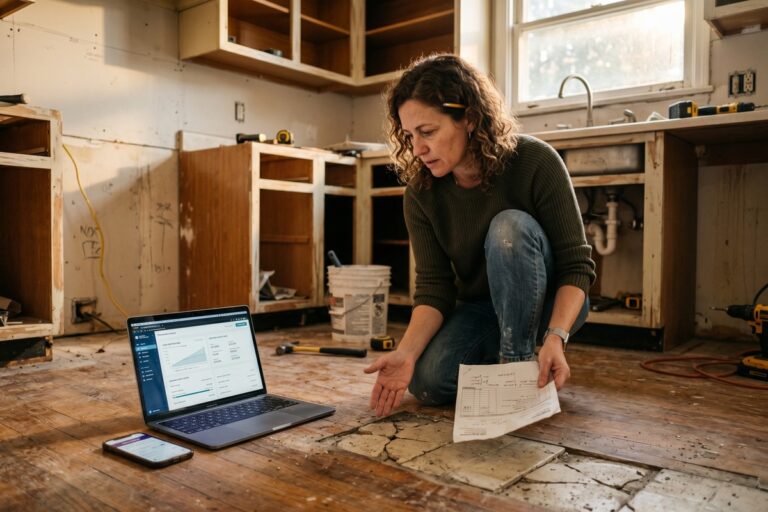

Banks reject multi-property landlords despite positive cash flow. Fintech platforms approve in 24-10 days, use rental income for underwriting, and require no property lien—letting you renovate and raise rents while keeping equity intact.

Fintech installment loans average 11–13% APR vs 21.5% for revolving credit—here's why the loan wins for repairs over $5,000 and the credit line wins under.