Digital Loan Stacking: Why Borrowing From Multiple Platforms at Once Quietly Backfires

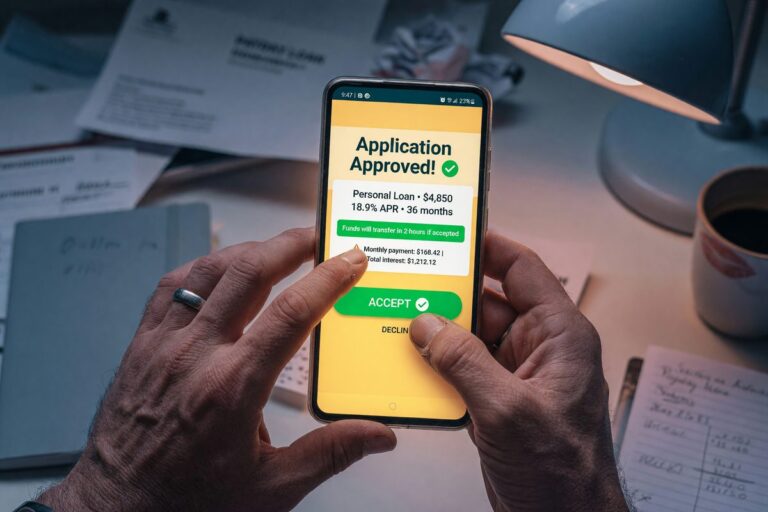

Borrowers who take a second loan within 15 days are 4x more likely to default. See how overlapping payments can consume 40-60% of monthly income.

Borrowers who take a second loan within 15 days are 4x more likely to default. See how overlapping payments can consume 40-60% of monthly income.

Newly sober borrowers who complete a credit-builder digital loan see average 48-point score gains in a year—but only if you can commit to reliable monthly payments.

Most digital lender soft pull offers range $25,000–$50,000, but lenders build in a 20–30% safety buffer. See how to maximize your prequalified amount.

43% of digital lenders now use cash flow, rent payments, and payroll data alongside credit scores. See how these alternative signals unlock approvals for credit-invisible borrowers.

Mainstream lenders auto-deny recent bankruptcies, but secured products and credit unions with manual review still approve. See which platforms say yes and what rates to expect.

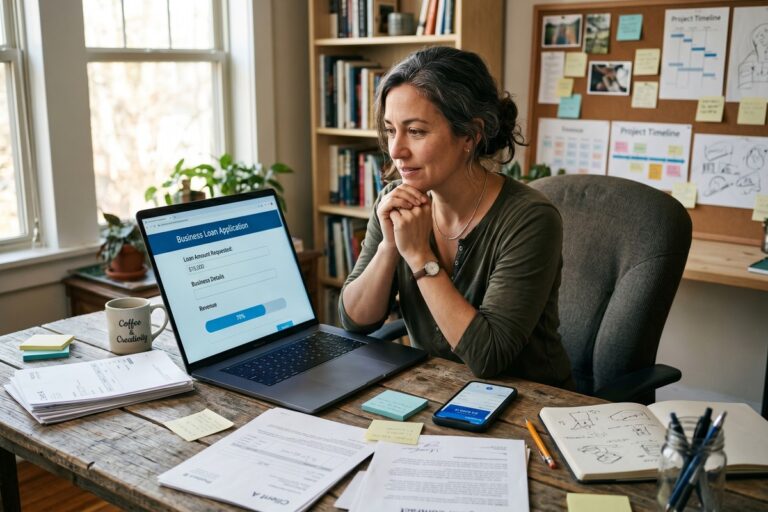

AI loan matching platforms deliver the biggest payoff for borrowers under 680 FICO or those comparing 10+ lenders at once. The real difference: whether you get genuinely different offers or just re-ranked duplicates.

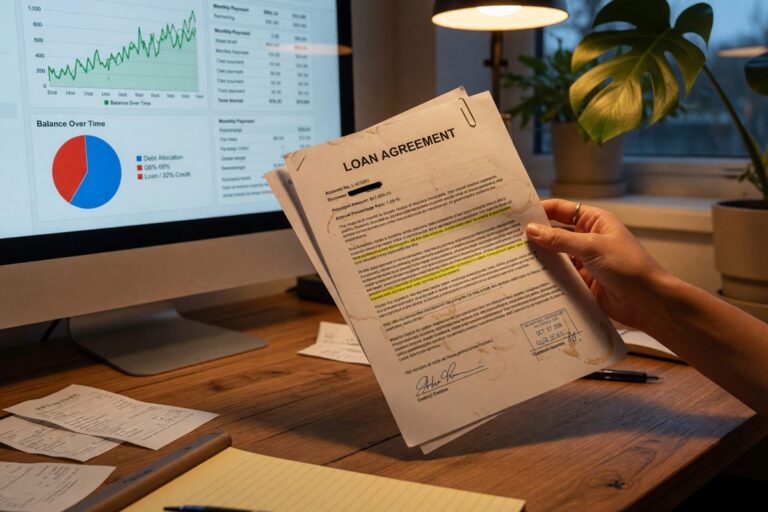

Refinancing cuts your rate only if it drops 1-2%+ and you have 3+ years left. Origination fees up to 8% often erase monthly savings—here's how to do the math.

Lenders keep your financial data for at least 7 years after closing—and often sell it. Here's when to request deletion and how to protect yourself from marketing abuse.

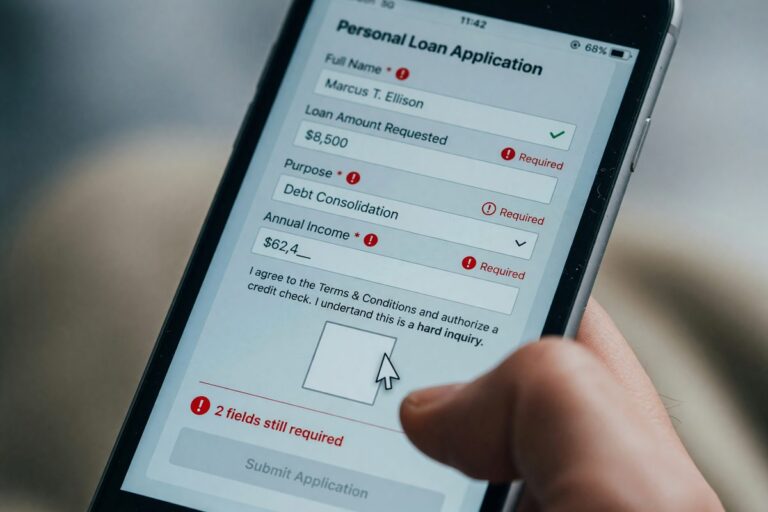

First-time borrowers with thin credit files lose more from pre-application errors than seasoned borrowers do. Here's what happens in those ten minutes before you click submit.

Gig workers average a 45% loan approval rate vs. 67% for W-2 earners—but it's a documentation gap, not a credit gap. Here's how to close it.