Fact-checked by the CapitalLendingNews editorial team

Roughly 9% of U.S. adults earned money from short-term gig tasks in 2024, according to the Federal Reserve’s 2024 Survey of Household Economics and Decisionmaking, yet the mortgage system those workers encounter was designed for someone with a W-2, a single employer, and a paycheck that looks the same every two weeks. The gap between what you earn and what a lender will agree to count as qualifying income can be jarring for anyone pursuing a gig worker mortgage rate in early 2025. Conventional 30-year fixed rates hovered near 7% entering 2025, and gig workers who cannot satisfy standard documentation rules routinely get quoted rates 125 to 300 basis points above that, before factoring in credit score or down payment adjustments.

The scale of the mismatch is not trivial. Fannie Mae’s January 2025 Mortgage Lender Sentiment Survey of nearly 200 senior mortgage executives found that 83% of lenders report that digital gig economy income is difficult to use when approving mortgage applications. That is a structural, institutional problem, not a personal income problem, and it helps explain why the same borrower profile can generate rate offers that differ by a full percentage point or more depending on which lender they approach first. Meanwhile, 49% of gig workers said they wished their pay was more consistent, a finding that reflects the income volatility underwriters are trained to penalize.

This article gives gig workers a detailed, honest map of what the mortgage market actually looks like in early 2025: why conventional qualification rules work against variable-income borrowers, which loan types offer the best trade-off between rate and documentation flexibility, how to build a financial profile that improves your odds before you apply, and when the math genuinely favors waiting rather than buying now at a punishing rate. By the end, you will have the information to make a loan-type decision based on real costs, not just what a lender tells you is possible.

Key Takeaways

- 83% of mortgage lenders report that digital gig economy income is difficult to use in loan approvals, making lender selection one of the highest-leverage decisions a gig worker can make.

- Non-QM bank statement loans carry a rate premium of 125 to 300 basis points above conventional rates, on a $400,000 loan, even the floor premium adds roughly $333 to $1,000 per month to your payment.

- A gig worker earning $120,000 but deducting $40,000 in legitimate business expenses may only qualify on $80,000 of income under conventional underwriting, cutting borrowing power by one-third.

- Switching from a Schedule C income qualification to a bank statement loan can increase purchasing power by up to 55%, in one documented case, from a $180,000 purchase to a $280,000 purchase, without any change in actual income.

- A 700+ credit score is the practical minimum target for gig workers seeking Non-QM financing; every tier below 720 triggers additional rate adjustments on an already expensive product.

- Non-QM should be treated as a bridge product: borrowers who build two years of strong net income on tax returns can refinance into conventional financing and recapture 100 to 300 basis points in rate savings.

In This Guide

- Why Gig Workers Face a Different Mortgage Market in Early 2025

- The Core Qualification Problem: How Tax Returns Work Against You

- Loan Options Ranked by Rate Cost and Documentation Flexibility

- What Underwriters Actually Look For, and What Triggers a Denial

- How to Build a Mortgage-Ready Financial Profile Before You Apply

- The Real Rate Premium: What Non-QM Actually Costs Over Time

- Choosing the Right Lender: Why This Decision Matters More for Gig Workers

- Honest Concessions: When Buying Now Is the Wrong Move

Why Gig Workers Face a Different Mortgage Market in Early 2025

The mortgage market entering 2025 is expensive for everyone. The average 30-year fixed rate sat near 7% in January and February, well above the sub-3% rates that defined 2021. But the starting rate is rarely the rate gig workers are actually quoted. A conventional conforming loan requires documentation that most platform-based earners cannot supply in standard form: two years of W-2s, consistent employer verification, and predictable monthly income. Those who fall outside that box get routed to non-qualified mortgage (Non-QM) products, where the pricing is calibrated to reflect additional lender risk.

The scope of the problem is wider than most discussions acknowledge. Data from the Bank of America Institute, cited in Fannie Mae’s Q4 2024 Mortgage Lender Sentiment Survey research, found that 3.8% of Bank of America customers received income from gig platforms via direct deposits or debit cards, surpassing the previous peak from early 2022. That share has been growing steadily, yet lender underwriting systems have not kept pace. The result is a workforce that is expanding faster than the financial infrastructure built to serve it.

What makes February 2025 particularly difficult is the combination of elevated base rates and a secondary market that is still working out how to price gig income risk consistently. Fannie Mae’s lender survey found that 46% of lenders want more prescriptive secondary-market guidelines for gig income, while 26% want more flexibility. The two camps cannot even agree on the direction of the solution. That disagreement filters down to individual borrowers in the form of wildly inconsistent rate offers across lenders, even for identical income profiles.

83% of mortgage lenders report that digital gig economy income is difficult to use in loan approvals, and 46% want more prescriptive secondary-market guidelines on how to assess it, according to Fannie Mae’s January 2025 Mortgage Lender Sentiment Survey.

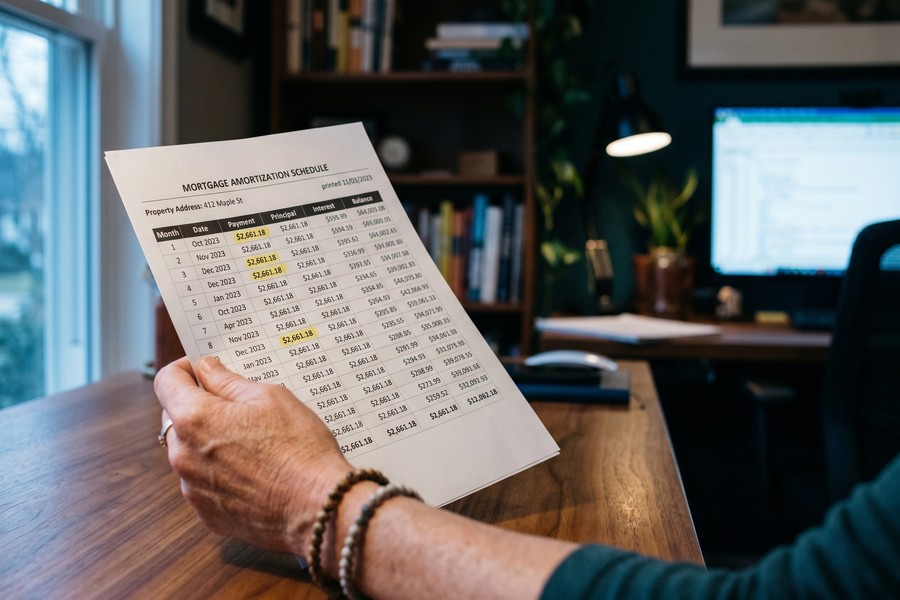

The Rate Arithmetic That Gig Workers Need to See

At a 7% conventional rate on a $400,000 30-year fixed loan, the principal and interest payment is approximately $2,661 per month. Add 150 basis points for a mid-tier Non-QM product and the rate becomes 8.5%, pushing the payment to roughly $3,076. That is a difference of $415 per month, or about $4,980 per year. At the top of the Non-QM range (10%), the payment climbs to $3,510, a gap of nearly $850 per month compared to the conventional baseline. These are not hypothetical scenarios; they reflect where gig worker rate offers are actually landing in early 2025.

Understanding this arithmetic matters before any lender conversation begins. Knowing the premium you are being asked to pay lets you evaluate whether the purchasing power gained from a bank statement qualification justifies the rate cost, and whether a refinance path exists to recapture it within a reasonable timeframe. Walking in without that context makes it easy to accept a quote that does not serve your financial interests.

The Core Qualification Problem: How Tax Returns Work Against You

The most common source of confusion for gig workers approaching mortgage lenders is the gap between gross income and qualifying income. Under conventional underwriting rules, and most lenders follow Fannie Mae’s framework, Schedule C net income is what counts, not the gross deposits flowing into your bank account. A graphic designer earning $120,000 in platform fees who deducts $40,000 in legitimate business expenses (software, equipment, home office, health insurance) shows $80,000 of net income on Schedule C. That $80,000 is the number an underwriter uses to calculate how much mortgage they can approve.

Per the Fannie Mae Selling Guide (B3-3.5-01), lenders must assess self-employed borrowers’ income stability and business viability using two years of signed federal tax returns, cash flow analysis tools such as Form 1084 and the Income Calculator, and an evaluation of whether the business can continue generating sufficient income to meet the mortgage obligation. This is a thorough, multi-step process, and every deduction you legitimately claim reduces the income figure that feeds into it.

The IRS Taxpayer Advocate Service notes that gig economy workers must report income from 1099-NEC and 1099-K forms and make quarterly estimated tax payments. These same records, and the deductions claimed on them, directly shape the qualifying income a mortgage underwriter will use.

The Two-Year Averaging Rule and Declining Income

Conventional lenders average the net income from the two most recent tax years to arrive at a monthly qualifying figure. Earning $90,000 net in 2022 and $70,000 net in 2023 averages to $80,000 annually, roughly $6,667 per month. That is already a conservative figure. But when income is declining year over year, many underwriters will use the lower year’s number rather than the average, treating the downward trend as evidence that the higher figure is not sustainable. A single bad business year can wipe out the benefit of a strong prior year entirely.

The reverse situation, a gig worker with a weak 2022 and a strong 2023, is where a less-discussed strategy applies. When the most recent return has not yet been filed at the time of application, a loan officer working with your CPA can sometimes structure the timing so that your stronger year is on file before the underwriter runs the income calculation. Filing a weaker year first when a stronger year already exists on paper is a costly mistake that most borrowers make by default because they do not coordinate with a mortgage professional before April 15. Gig workers expecting a strong income year should have this conversation in January or February, not after tax season closes.

The Schedule C Trap: Deductions Versus Qualifying Income

The tension between tax optimization and mortgage qualification is real and irresolvable in a single tax year. A CPA focused exclusively on minimizing tax liability will encourage maximum deductions. A mortgage loan officer looking at the same returns will see a smaller qualifying income figure and a smaller loan approval. The practical solution is to decide, 12 to 18 months before you plan to apply, which priority matters more for that specific tax year. The answer is not always the one that maximizes your refund.

Some gig workers find a middle path: they claim necessary deductions but stop claiming optional or marginal ones they would otherwise take, accepting a slightly higher tax bill in exchange for a significantly higher qualifying income. Whether that trade-off makes financial sense depends on your marginal tax rate, the size of the loan you are trying to qualify for, and the rate premium you would otherwise pay on a Non-QM product. Run that calculation explicitly rather than making the decision by default. For more on how income documentation shapes borrowing power across platforms, see our article on how gig economy workers pay a higher effective interest rate than traditional employees.

Loan Options Ranked by Rate Cost and Documentation Flexibility

Gig workers in 2025 have four realistic mortgage paths. They differ significantly on both rate and documentation requirements, and the best choice depends on your income type, tax return profile, credit score, and how urgently you need to close. Below is an honest comparison of the main options.

| Loan Type | Qualification Basis | Rate vs. Conventional | Best For |

|---|---|---|---|

| Conventional (Conforming) | 2-year tax returns, Schedule C net income | Baseline (near 7%) | 2+ years of strong net income, 700+ credit score |

| FHA / VA | Same income rules as conventional, lower down payment | +0 to +25 bps | Gig workers with qualifying net income but limited savings |

| Bank Statement Non-QM | 12 or 24 months of bank deposits | +125 to +300 bps | High gross income, large deductions, cannot show net income |

| 1099 / P&L Only | 1099 totals or CPA-prepared P&L statement | +150 to +275 bps | Clean 1099 flows without complex expense structures |

| Asset Depletion / DSCR | Liquid assets or rental property cash flow | +175 to +350 bps | Gig workers with substantial savings or investment property |

The Bank Statement Loan: Most Misunderstood Option

The bank statement loan is the most consequential option on this list for gig workers with high gross income and large deductions. Instead of reviewing Schedule C net income, lenders analyze 12 or 24 months of personal or business bank deposits, apply an expense factor (commonly 50% for personal accounts, 10 to 50% for business accounts with a CPA letter), and use the resulting figure as qualifying income. A gig worker depositing $5,500 per month on average qualifies on roughly that amount rather than the much lower Schedule C figure.

The documented purchasing-power gap is significant. In one lender case study cited in Fannie Mae’s research, the same borrower qualified for a $180,000 purchase on tax return income versus a $280,000 purchase on bank statement income. That is a 55% increase in buying power from switching loan types alone, without any change in actual earnings. The rate cost is real, though, and anyone comparing these paths should model the monthly payment difference explicitly before choosing the bank statement route on purchasing power alone.

Asset Depletion and DSCR Loans: Niche but Legitimate

Two less-discussed options deserve attention for specific gig worker profiles. Asset depletion loans allow lenders to treat a borrower’s liquid assets (savings, investment accounts, retirement accounts with a haircut) as if they were income, dividing the total by the loan term in months to create a monthly qualifying figure. A gig worker with $600,000 in liquid assets could qualify on a notional $2,500 per month of “income” from that pool over a 20-year term, regardless of what their tax returns show.

DSCR (debt service coverage ratio) loans apply to gig workers who also own rental or investment property. Here, the property’s rental income relative to the mortgage payment determines qualification; the borrower’s personal income is largely irrelevant. A property generating $2,200 per month in rent against a proposed $1,800 mortgage payment produces a DSCR of 1.22, which meets most lenders’ minimum threshold of 1.20. These products carry higher rate premiums than bank statement loans but serve a specific population of gig workers well. Our article on digital lending for gig workers between contracts covers how to borrow during income gaps more broadly.

Earning across multiple gig platforms, say, Uber, DoorDash, and Instacart, aggregate all three 1099 income streams into a single qualifying figure rather than presenting them separately. Most applicants undercount their total by treating each platform as a distinct, partial income source. A lender who sees three small streams may discount them; one who sees a combined gross of $72,000 reads a full-time gig income.

What Underwriters Actually Look For, and What Triggers a Denial

Most borrowers think underwriters are primarily checking credit scores. Credit matters, but for gig workers, the three signals that drive approval decisions are income stability trend, continuance of income, and depth of reserves. Understanding these helps you prepare documentation strategically rather than reactively.

Income stability trend refers to whether your net qualifying income is flat, rising, or declining over the review period. Flat or rising income is acceptable; it shows the gig business is at least holding steady. Declining income over two consecutive years is a red flag even if the absolute figure is still relatively high. An underwriter who sees $120,000 in year one and $90,000 in year two will not average to $105,000. They will often use $90,000 and wonder whether next year will be $65,000.

Continuance of Income: Proving Tomorrow’s Earnings Today

Continuance of income is the underwriter’s attempt to verify that your gig income is likely to persist through the loan term. For W-2 employees, this is easy: submit an employment verification letter. Gig workers must demonstrate that their client base, platform activity, or contract flow shows no signs of winding down. Platform earnings statements showing consistent or growing monthly totals help. A letter from a long-term client confirming ongoing work helps more. Gaps in platform activity, even seasonal ones, can trigger questions about whether income will continue.

Reserves are the third pillar. Most lenders want to see at least three to six months of mortgage payments sitting in liquid accounts after closing. For a gig worker on a Non-QM loan with a $3,000 monthly payment, that means $9,000 to $18,000 must remain in the bank after the down payment clears. Reserves signal that the borrower can absorb a slow month or two without defaulting, which matters more for variable-income borrowers than it does for salaried ones.

Less-Discussed Denial Triggers

Several documentation problems derail gig worker applications that would otherwise survive on income numbers alone. The most common is mixing personal and business bank accounts. When deposits from gig platforms flow into the same account as personal spending, cash flow analysis becomes unreliable and lenders may discount or disqualify the income entirely. Separating accounts is a prerequisite for a clean bank statement loan application, and it should happen at least 12 months before you plan to apply.

Large unexplained deposits in the months before application are another common problem. A $15,000 transfer from a family member, an insurance payout, or a one-time freelance project that inflates one month’s deposits will prompt documentation requests. When those deposits cannot be sourced and seasoned, they may be excluded from the income average, or flag the application for additional scrutiny. Preparing a paper trail for any unusual deposit before the underwriter asks for it is far easier than explaining it under deadline pressure.

Mixing personal and business bank accounts is one of the most common reasons gig worker bank statement loan applications stall or get denied. When gig deposits and personal spending run through the same account, lenders cannot cleanly calculate qualifying income, and they will not give you the benefit of the doubt. Open a dedicated business account at least 12 months before applying.

How to Build a Mortgage-Ready Financial Profile Before You Apply

The gig workers who get the best rate offers are not necessarily the ones with the highest gross income. They are the ones who have spent 12 to 18 months deliberately preparing their financial profile to look as clean and predictable as possible to an underwriter. That preparation follows a specific sequence.

Start with account separation: one bank account for gig income deposits, one for personal spending. This is not optional for bank statement loan applicants. It is the foundation that makes the rest of the income analysis possible. Once accounts are separated, the 12-month deposit history begins to build. Every month of clean, consistent gig deposits into a dedicated account strengthens the bank statement loan case.

The Credit Score Threshold Reality

Credit score tiers are not just a qualifier for gig workers pursuing Non-QM financing. They determine the rate pricing tier you land in. Most Non-QM lenders structure their pricing grids around 620, 660, 680, 700, and 720+ credit score bands. Crossing from 699 to 700 can reduce your rate by 25 to 50 basis points on a bank statement loan. Crossing from 719 to 720 can reduce it by another 25 to 50 basis points. On a $400,000 loan, a 50-basis-point rate improvement translates to roughly $125 per month in savings, and sustained over a 10-year hold period, that compounds significantly.

A 700+ credit score is the practical minimum target for competitive Non-QM pricing. Getting there from, say, 660 requires reducing credit utilization below 30%, clearing any derogatory marks that can be disputed, and avoiding new credit inquiries in the 6 months before application. With a score currently below 680, spending 6 to 12 months on credit repair before applying is likely to generate a rate improvement that more than offsets the delay. Our article on debt-to-income ratio on digital lending platforms explains in detail how DTI and credit score interact to shape your application outcome.

Tax Filing Strategy: A Conversation to Have Before April 15

The tax return filed this spring will be part of the two-year income average the underwriter uses for any gig worker planning to apply for a mortgage in 2025. When 2024 was a strong income year and 2023 was weaker, filing the 2024 return before applying adds a stronger data point to the average. When 2024 was weaker and 2023 was stronger, there may be a narrow window to apply using only the 2023 return before the 2024 return becomes available, though this requires careful coordination with a loan officer on timing.

This conversation must happen between a CPA and a mortgage professional, preferably before February 28 when a spring application is planned. Most articles on gig worker mortgages ignore this entirely. The tax filing decision is not just an accounting choice; it is a mortgage strategy decision, and treating it as such can materially change the qualifying income figure an underwriter sees. Also worth considering: the decision to wait for rates to drop or lock in what you can qualify for today deserves the same deliberate analysis.

Per the Fannie Mae Selling Guide (B3-3.2-02), borrowers qualifying with income from multiple employment sources simultaneously, including self-employment, must meet the documentation requirements for each specific income type. Gig workers with blended income from both W-2 employment and platform work must document both streams fully, but they can combine them into a single qualifying income figure.

The Real Rate Premium: What Non-QM Actually Costs Over Time

The 125 to 300 basis point premium that Non-QM loans carry over conventional rates is not arbitrary pricing. Non-QM and Non-Prime 30-day delinquency rates have been running above 7%, compared to sub-2% for conventional conforming loans. That default rate differential is what lenders are pricing when they quote 8.5% on a bank statement loan versus 7% on a conventional. Understanding the pricing rationale does not make the cost easier to absorb, but it does frame the decision correctly: you are paying for risk-based pricing, not lender arbitrariness.

The monthly cost differential deserves to be modeled explicitly rather than acknowledged in the abstract. For a $400,000 30-year loan:

| Rate | Monthly P&I Payment | vs. 7% Conventional | 10-Year Additional Cost |

|---|---|---|---|

| 7.00% (Conventional) | $2,661 | Baseline | Baseline |

| 8.25% (Non-QM Floor) | $3,007 | +$346/month | +$41,520 |

| 8.75% (Non-QM Mid) | $3,143 | +$482/month | +$57,840 |

| 10.00% (Non-QM High) | $3,510 | +$849/month | +$101,880 |

These are not edge cases. They represent the actual range where gig worker Non-QM loans are pricing in early 2025. The 10-year additional cost column is what makes the purchasing power gain from a bank statement qualification more complicated than it looks at first glance. Qualifying for a $280,000 purchase instead of a $180,000 purchase is valuable, but when the rate on the $280,000 loan is 9.5% and the alternative conventional rate would be 7%, the monthly payment on the larger, more expensive loan may exceed what the borrower can sustainably manage.

The Refinance-Out Strategy

Non-QM financing should be treated as a bridge, not a permanent solution. The path that makes this loan type financially rational is the refinance. A gig worker who takes a bank statement Non-QM loan at 8.75% today and then spends the next two years building a clean, rising net income profile on their tax returns can refinance into a conventional loan when those two years of returns are on file. When conventional rates have dropped to, say, 6% by 2027, the rate improvement of 275 basis points would reduce the monthly payment on a $280,000 balance by approximately $500. The Non-QM loan effectively purchased the home and the time needed to qualify conventionally.

The honest caveat: this strategy requires two things to happen simultaneously. Your tax return profile must improve, and conventional rates must decline. Neither is guaranteed. A gig worker should not enter a Non-QM loan assuming the refinance will materialize on any particular timeline. Build the financial profile as if the refinance opportunity might not come for three to five years, and if it arrives sooner, treat it as a bonus. For a deeper analysis of rate lock timing decisions, see our coverage of whether to lock your rate early or float it when the Fed signals a pause.

At a $400,000 loan, the Non-QM rate premium floor of 125 basis points adds roughly $333 to $1,000 per month compared to a conventional loan, translating to $4,000 to $12,000 in additional annual interest cost, before any credit score adjustments.

Choosing the Right Lender: Why This Decision Matters More for Gig Workers

For a salaried borrower, lender selection affects the rate by perhaps 25 to 50 basis points, meaningful but limited. For a gig worker, lender selection affects both the rate and whether the income is counted at all. As Fannie Mae’s research showed, 83% of lenders report difficulty using digital gig income in approvals, and the 46% who want more prescriptive guidelines and the 26% who want more flexibility disagree on how to solve the problem. That disagreement shows up in concrete underwriting decisions.

Some lenders use a 12-month bank statement window; others require 24 months. A gig worker with a strong 2024 but a weaker 2023 is significantly better served by a 12-month underwriter. Some lenders apply a flat 50% expense factor to personal bank deposits regardless of actual business costs; others accept a CPA-prepared profit and loss statement that may reflect a much lower actual expense ratio, resulting in a higher qualifying income. Asking these questions before submitting an application is not excessive. It is the difference between qualifying and not.

Concrete Shopping Criteria

When evaluating lenders, gig workers should ask four specific questions. First: do they use 12-month or 24-month bank statement averages? Second: do they apply a standard expense factor or accept a CPA-prepared P&L that reflects actual costs? Third: do they allow income aggregation from multiple gig platforms into a single qualifying figure? Fourth: what credit score tier triggers their best Non-QM pricing, and what documentation do they need to underwrite blended income streams?

Lenders who specialize in Non-QM products will answer these questions fluently. Lenders who primarily process conventional loans and treat Non-QM as an afterthought often cannot. The quality of the answer to question three, multi-platform income aggregation, is one of the fastest diagnostic tests. A lender who has underwritten multiple gig workers will understand immediately why combining Uber, DoorDash, and Instacart 1099 income into one figure matters. A lender who has not will ask you to document them separately and potentially undercount the total.

| Lender Variable | Better for Gig Workers | Worse for Gig Workers |

|---|---|---|

| Bank Statement Window | 12 months (captures strong recent year) | 24 months (averages in a weak prior year) |

| Expense Factor | CPA-prepared P&L accepted | Flat 50% applied regardless of actual costs |

| Multi-Platform Income | Aggregated into single qualifying figure | Treated as separate, potentially discounted streams |

| Reserve Requirement | 3 months PITIA | 6–12 months PITIA |

| DTI Maximum | 50% or higher (Non-QM) | 43% or lower (conventional standard) |

Fintech lenders and portfolio lenders are increasingly experimenting with alternative income documentation: payroll data aggregators, platform API data, and cash flow analysis tools that go beyond paper bank statements. Our article on how fintech lenders use payroll data to approve borrowers banks would reject covers the mechanics in detail.

The CFPB’s ability-to-repay framework requires lenders to verify income using reasonably reliable third-party records and to consider income, assets, debt obligations, DTI ratio, and credit history when evaluating non-traditional borrowers. Critically, the CFPB notes that qualified mortgages typically carry lower rates than Non-QM alternatives, which is why qualifying conventionally, even partially, is always worth pursuing first.

Honest Concessions: When Buying Now Is the Wrong Move

Most articles on gig worker mortgages conclude with encouragement: you can qualify, here’s how, go apply. That is not always the right advice. There is a specific profile of gig worker for whom buying in early 2025 at Non-QM rates is genuinely the wrong financial decision, and it is worth naming it directly.

In year one of consistent gig income, with a flat or declining income trend and a credit score below 680, you are looking at a rate offer in the 9.5% to 10.5% range on a bank statement loan, when approval is even possible. At those rates on a $350,000 loan, the monthly payment exceeds $3,200. Renting a comparable home in many markets while spending 12 to 18 months building a stronger financial profile may cost significantly less on a monthly basis and position you for a materially better rate offer when you do buy.

The Dual Assumption Problem in the Refinance Strategy

The refinance-out strategy is sound when both conditions are met: your net income on tax returns improves over two years, and conventional rates decline enough to make refinancing worthwhile after closing costs. The problem is treating both as reliable. Conventional rates may stay at or above 7% through 2026. The Federal Reserve has signaled that rate cuts will be gradual, not dramatic. A gig worker’s net income on returns may not improve if they continue maximizing deductions or experience a business slowdown.

Buying a home at 9.5% today on the assumption that you will refinance to 6.5% in two years requires two independent favorable outcomes to materialize on the same timeline. That is a legitimate bet with a strong income trend, a 720+ credit score, and deep reserves. With any of those three conditions uncertain, it becomes a fragile one. The honest position: Non-QM is a tool that works well for specific, financially strong gig workers and is a trap for those who stretch to use it prematurely.

Entering a Non-QM loan at 9% or higher on the assumption that you will refinance into a conventional product within two years requires both your tax return income and market interest rates to cooperate simultaneously. Neither is guaranteed. Model the scenario where you stay in the Non-QM loan for five years, if that payment is unsustainable, the purchase is premature regardless of how compelling the property is.

For gig workers weighing the rent-versus-buy decision in this environment, our analysis of renting vs. buying in your 30s and how to run the numbers provides a structured framework for making that call before committing to either path.

Real-World Example: A Freelance Designer Navigating the Non-QM Decision

Consider an illustrative example: a freelance UX designer, 34 years old, who has been working independently for three years after leaving a salaried position. Her gross annual income from three platform clients runs approximately $110,000, but her Schedule C net income after deducting software subscriptions, equipment, home office costs, and professional development totals $72,000. Her credit score is 715, she has $55,000 saved for a down payment and reserves, and she is targeting a $380,000 home purchase in a mid-sized metropolitan market.

On the conventional path, her qualifying income of $72,000, averaged with a slightly lower $68,000 from the prior year, produces a monthly qualifying income of roughly $5,833. At a 43% DTI ceiling, she can support approximately $2,508 per month in total debt payments. After accounting for property taxes, insurance, and a small existing student loan payment, she qualifies for a mortgage payment of about $1,900, which at 7% gets her to roughly a $285,000 loan. She cannot afford the $380,000 target on conventional financing without a larger down payment.

On the bank statement loan path, her 12-month average of gross deposits across all three clients totals $9,100 per month. The lender applies a 40% expense factor using a CPA-prepared P&L (rather than the standard 50% flat factor), producing a qualifying income of $5,460 per month, nearly the same as the conventional figure. Because the bank statement lender allows a 50% DTI, she qualifies for a higher total debt payment. At 8.75% on a Non-QM product, she qualifies for a loan of approximately $345,000. Still short of the $380,000 target, but materially closer, and she has the $55,000 to bridge the gap with a 10% down payment on the $380,000 price.

The trade-off is explicit: the bank statement loan at 8.75% produces a monthly P&I payment of approximately $2,715, compared to the $1,900 she could sustain conventionally on a smaller loan. Her reserves after closing drop to about $17,000, just under six months of payments. She proceeds, with the clear plan to monitor her two-year income trend and target a refinance to conventional when her 2025 and 2026 tax returns reflect consistent $80,000+ net income. The Non-QM loan buys her the home and the time to build the conventional-qualifying profile. But she does it with eyes open: if rates do not fall and her net income does not grow, she stays in the Non-QM product for years, at a cost that is real and significant.

Your Action Plan

-

Separate your bank accounts immediately

Open a dedicated business checking account for all gig platform deposits and stop routing personal spending through it. A clean 12-month deposit history in a separate account is the foundational requirement for any bank statement loan application. The clock starts the day you separate accounts, so do not wait until you are ready to apply.

-

Have the CPA-loan officer conversation before filing your taxes

Planning to apply for a mortgage in 2025 means connecting a mortgage loan officer with your CPA before April 15. The decision of whether to maximize deductions or preserve qualifying income for the year you plan to apply can change your approved loan amount significantly. This conversation has to happen before you file, not after.

-

Get your credit score to 700+ before applying

Pull your credit reports from all three bureaus and identify any derogatory marks, high-utilization accounts, or errors. Reduce revolving balances below 30% of credit limits, dispute any errors in writing, and avoid new credit applications for at least six months before submitting a mortgage application. Each tier above 700 unlocks better Non-QM pricing.

-

Aggregate your multi-platform income into a single qualifying figure

Collect all 1099 forms and bank statements that document each income stream across every platform. When presenting your application, make clear to the lender that these are simultaneous, ongoing income sources that should be combined into one qualifying total. Ask explicitly whether their underwriting process allows multi-platform income aggregation before choosing a lender.

-

Model the rate premium cost before choosing a loan type

Use an amortization calculator to compare your monthly payment and 10-year total interest cost at the conventional rate you could qualify for versus the Non-QM rate you are being quoted. When the purchasing power gain from the Non-QM path justifies the additional monthly cost and you can sustain that payment without the refinance materializing, proceed. When the math only works assuming a refinance within two years, stress-test that assumption carefully.

-

Shop at least three lenders with Non-QM product lines

Ask each lender the four diagnostic questions: 12-month or 24-month bank statement window, standard expense factor or CPA P&L accepted, multi-platform income aggregation allowed, and what credit score tier triggers best pricing. The answers will differ, and the lender whose methodology aligns best with your income profile will likely offer a meaningfully better rate.

-

Build reserves beyond the minimum requirement

Target six months of full housing payment (principal, interest, taxes, and insurance) in liquid accounts after closing costs and down payment. Lenders may require only three months, but deeper reserves improve approval odds, sometimes unlock better pricing tiers, and provide the actual financial buffer a gig worker needs in a slow-income month.

-

Set a refinance trigger, not a refinance hope

Entering a Non-QM loan means defining the specific conditions that will prompt you to apply for a refinance: for example, two years of tax returns showing $85,000+ net income and conventional rates at or below 6.5%. Review those conditions annually and engage a loan officer when both are approaching. Treating the refinance as a vague future possibility rather than a tracked goal means it may never happen.

Frequently Asked Questions

Can gig workers get a conventional mortgage, or do they always need Non-QM?

Gig workers can qualify for conventional conforming loans, but they must meet the same income documentation standards as any self-employed borrower: two years of signed federal tax returns, a two-year self-employment history, and net income that supports the requested loan amount at a DTI of 43% or below. When Schedule C net income is sufficient to qualify at current conventional rates, the conventional path is almost always preferable because the rate is lower. Non-QM becomes necessary only when tax return income is too low to qualify, or when the borrower has less than two years of consistent gig income history.

How do lenders calculate income for a gig worker?

For conventional loans, lenders average the Schedule C net income from the two most recent tax years and divide by 24 to arrive at a monthly qualifying figure. For bank statement Non-QM loans, lenders average 12 or 24 months of gross bank deposits, apply an expense factor (typically 40 to 50%), and use the resulting figure as monthly income. For 1099-based Non-QM products, lenders may accept total annual 1099 income reduced by an estimated expense percentage. The income calculation method varies by loan type and lender, which is why the lender selection decision matters enormously for gig workers.

Does having income from multiple gig platforms help or hurt a mortgage application?

It helps, provided the income is documented cleanly and presented as an aggregated total. Per the Fannie Mae Selling Guide (B3-3.2-02), borrowers qualifying with income from multiple sources simultaneously must meet documentation requirements for each income type, but the incomes can be combined into a single qualifying figure. The practical problem is that applicants often present each platform as a separate, partial income source, which can lead underwriters to discount or question each stream individually. Present combined income with supporting documentation for each platform and make the aggregation explicit.

What credit score do gig workers need to get a Non-QM mortgage?

Most Non-QM lenders have a minimum credit score floor of 620, but the rates at that floor are typically in the 10% to 11% range on bank statement products in the current environment. The meaningful threshold for competitive Non-QM pricing is 700+, with additional improvement at 720+. Gig workers below 700 should strongly consider spending 6 to 12 months on credit improvement before applying, because the rate reduction from crossing that threshold is typically worth more in lifetime interest savings than the delay costs in rent.

What is a bank statement loan and how does it work for gig workers?

A bank statement loan is a Non-QM mortgage product that qualifies borrowers based on their bank deposit history rather than their tax returns. The lender typically reviews 12 or 24 months of personal or business bank statements, calculates the average monthly deposits, applies an expense factor to estimate the net income, and uses that figure for qualification. For gig workers with high gross income and large Schedule C deductions, bank statement loans can unlock significantly more purchasing power than conventional loans, but at a rate premium of 125 to 300 basis points above conventional rates in the current market.

How do I prove to a lender that my gig income will continue?

Continuance of income is established through a combination of documentation and trend analysis. Platform earnings statements showing consistent or growing monthly activity are the baseline. A history of repeat clients (documented through contracts, emails, or platform transaction records) strengthens the case further. For gig workers with seasonal income patterns, a written explanation of the seasonal cycle, supported by multi-year data showing the pattern is consistent, can prevent an underwriter from flagging a predictable slow month as evidence of income decline. Some lenders also accept a letter from a platform operator confirming the account is in good standing.

Can I use both W-2 income and gig income to qualify for a mortgage?

Yes. Working a salaried position while also earning gig income means both streams can be used to qualify, provided each is documented according to its respective income type requirements. W-2 income is documented through employer verification and pay stubs. Gig income is documented through tax returns or bank statements, depending on the loan type. Per Fannie Mae’s Selling Guide, borrowers with multiple simultaneous income sources must meet the documentation standard for each type. The combined qualifying income from both sources can substantially increase the loan amount available compared to either income stream alone.

What is the downside of waiting to buy a home as a gig worker?

Waiting has real costs: rent paid during the delay does not build equity, home prices may rise during the preparation period, and there is no guarantee that the qualification landscape will be meaningfully more favorable in 12 to 18 months. The strongest argument for waiting is when the rate premium you would pay today is so significant that renting costs less monthly and the financial profile improvement is achievable within a specific, realistic timeframe. Waiting indefinitely without a clear set of qualifying milestones to hit is not a strategy. It is procrastination dressed as financial prudence.

What are DSCR loans and who are they best suited for among gig workers?

DSCR (debt service coverage ratio) loans qualify the borrower based on the rental income of an investment property, not the borrower’s personal income. The lender divides the property’s gross rental income by the proposed mortgage payment; if the ratio exceeds 1.20 (meaning the property generates at least 20% more income than the mortgage costs), the loan is typically approvable. DSCR loans are best suited for gig workers who already own or are purchasing an investment property, and who have difficulty documenting personal income sufficient to qualify conventionally. They carry higher rate premiums than bank statement loans but solve the income documentation problem entirely for eligible properties.

Is it possible to refinance from a Non-QM loan into a conventional mortgage?

Yes, and this is the intended exit strategy for many Non-QM borrowers. Once a gig worker has two years of tax returns on file showing strong, stable, or rising net income that satisfies conventional underwriting standards, they can apply to refinance into a conventional conforming loan and recapture 100 to 300 basis points in rate savings. The refinance requires meeting the same qualification criteria as a new purchase loan, including DTI, credit score, and LTV requirements. Closing costs for a refinance typically range from 2% to 5% of the loan balance, so the rate improvement must be large enough and the expected hold period long enough to justify the cost. See our analysis of fixed vs. adjustable rate loans for self-employed borrowers for additional context on structuring the loan term during this refinance planning window.

Sources

- Federal Reserve Board, 2024 Survey of Household Economics and Decisionmaking: Employment and Gig Work

- Federal Reserve Board, 2024 Survey of Household Economics and Decisionmaking: Income and Expenses

- Fannie Mae Research and Insights, Leveraging Variable and Gig Income to Expand Access to Homeownership (January 2025)

- Fannie Mae Selling Guide, B3-3.5-01: Underwriting Factors and Documentation for Self-Employed Borrowers

- Fannie Mae Selling Guide, B3-3.2-02: Standards for Employment-Related Income

- Consumer Financial Protection Bureau, What Is a Qualified Mortgage?

- IRS Taxpayer Advocate Service, An Introduction to Tax Forms for Gig Economy Workers (February 2024)

- AmeriSave, Self-Employed Mortgage Guide: Strategies to Get Approved (citing BLS data on self-employed workers)

- Consumer Financial Protection Bureau, Regulation Z: Ability-to-Repay and Qualified Mortgage Standards

- U.S. Bureau of Labor Statistics, Employed Persons by Class of Worker and Part-Time Status

- CapitalLendingNews, How Gig Economy Workers Pay a Higher Effective Interest Rate Than Traditional Employees

- CapitalLendingNews, Digital Lending for Gig Workers Between Contracts: How to Borrow During Income Gaps

- CapitalLendingNews, Debt-to-Income Ratio on Digital Lending Platforms: The Number That Quietly Kills Your Application

- CapitalLendingNews, How Fintech Lenders Are Using Payroll Data to Approve Borrowers Banks Would Reject

- CapitalLendingNews, Fixed vs Adjustable Rate Loans for Self-Employed Borrowers: Key Differences Explained