Fact-checked by the CapitalLendingNews editorial team

Quick Answer

To use fintech pre-approval strategies effectively, collect at least 3 competing offers using soft-pull tools within a 14-day window to protect your credit score, then present the best competing offer to your preferred lender and ask them to match or beat the rate or fees. Most borrowers complete this process in under a week and can realistically negotiate a lower origination fee or a rate reduction of 0.25% or more.

Fintech pre-approval strategies give borrowers a concrete negotiating position before they ever sit down with a lender. By using soft-pull pre-approval tools from platforms like SoFi, Upstart, and Credible to gather competing offers, you arrive at the table with documented alternatives rather than a general sense that better deals might exist. According to the Consumer Financial Protection Bureau, a pre-approval does not bind you to a lender, and shopping and comparing loan offers is the single most reliable path to securing better terms.

The opportunity here is real, and most borrowers are leaving it on the table. Freddie Mac research shows that applying with multiple mortgage lenders can save borrowers up to $1,200 per year, and the CFPB estimates that if just 20% of homebuyers obtained one additional mortgage quote, they would collectively save $4 billion annually., fintech lending platforms have expanded well beyond mortgages into personal loans, auto financing, and small business credit, making the multi-offer strategy accessible across virtually every loan type.

This guide is for borrowers who want more than a loan approval. Whether you are financing a vehicle, consolidating debt, or buying a home, the steps below will show you how to build a pre-approval stack, use it as live negotiating ammunition, protect your credit score throughout the process, and close with better terms than the first offer you were given.

Key Takeaways

- Nearly half of mortgage borrowers apply with only one lender, according to CFPB research, meaning collecting multiple fintech pre-approvals already puts you ahead of most of the market before negotiations begin.

- Freddie Mac data shows comparison-shopping can save borrowers up to $1,200 per year on mortgage payments, a figure that applies before any active negotiation takes place.

- Multiple mortgage or auto loan hard inquiries made within a 14-to-45-day window count as a single inquiry under most FICO scoring models, according to myFICO, making wide pre-approval shopping nearly credit-neutral.

- A Federal Reserve research note documents that FinTech lenders held approximately 14% of all U.S. personal loans as of end-2022, operating under a complex multilayered regulatory environment.

- The CFPB has warned that some fintech comparison-shopping platforms accept payments from lenders to manipulate results, per a CFPB circular on steered comparison results, making it essential to verify that the tool you use surfaces neutral, unsponsored offers.

- A single hard credit inquiry typically causes a 5-to-10-point temporary drop in credit score, with most scores recovering within 3-to-6 months, according to myFICO, a risk that is manageable when timed correctly.

In This Guide

- Step 1: Why Pre-Qualification and Pre-Approval Are Not the Same Thing

- Step 2: How Fintech Pre-Approval Tools Work, and What They See That You Don’t

- Step 3: How to Build a Pre-Approval Stack Across Multiple Lenders

- Step 4: How to Use Competing Pre-Approval Offers to Negotiate Better Terms

- Step 5: How to Protect Your Credit Score Throughout the Pre-Approval Process

- Step 6: Matching the Right Fintech Tool to Your Loan Type

- Step 7: Keeping Negotiating Leverage Alive Through Closing

- Frequently Asked Questions

Step 1: Why Pre-Qualification and Pre-Approval Are Not the Same Thing

The single most common mistake borrowers make with fintech pre-approval strategies is treating a soft-pull pre-qualification as though it carries the same weight as a verified pre-approval. It does not, and lenders know the difference immediately.

How to Do This

A pre-qualification is an estimate. The lender or platform runs a soft credit pull, takes your self-reported income and debt at face value, and returns a rate range. No documents are verified, and there is no conditional commitment to lend. A verified pre-approval, by contrast, involves the lender pulling a hard copy of your credit report, reviewing documentation (pay stubs, tax returns, or bank statements), and issuing a conditional commitment letter stating the amount and rate they are prepared to offer. That letter is what gives you real negotiating power.

Many fintech platforms market pre-qualification results using language like “pre-approved” or “you’re matched” in their interface. Before you use any offer as negotiating ammunition, confirm in writing whether the rate you received came from a verified review of your financial documents or from a soft-pull estimate. Ask directly: “Is this a conditional commitment backed by document verification, or a rate estimate based on self-reported information?” A lender who won’t answer clearly is telling you something.

What to Watch Out For

If you present a soft-pull pre-qualification letter to a competing lender as though it were a verified pre-approval, you may lose credibility in the negotiation. Underwriters recognize the difference, and some will call your bluff. Rely only on offers that include the lender’s name, the specific rate and loan amount, and a statement that the offer is subject to final underwriting, not just marketing copy.

The CFPB advises consumers that a pre-approval letter does not bind them to a lender, it is a conditional commitment from the lender to them. That means you can collect several verified pre-approvals without any obligation to use any of them, giving you a risk-free way to build negotiating leverage.

Step 2: How Fintech Pre-Approval Tools Work, and What They See That You Don’t

Fintech pre-approval tools operate on AI-driven underwriting models that evaluate far more than a FICO score. Understanding what these systems are looking at lets you surface your strongest data before the review runs, which directly influences the rate you are offered.

How to Do This

Platforms like Upstart have publicly described underwriting models that evaluate over 1,000 data variables, including cash flow patterns, employment history, educational background, and account behavior. LendingClub and SoFi use similar alternative data frameworks. This is genuinely good news for borrowers who have strong financial behavior but a thin traditional credit file. If you have been paying rent on time, maintaining consistent account balances, or running a stable freelance income, a fintech underwriting engine may value that data in ways a traditional bank would not.

To take advantage of this, proactively link your bank accounts, payroll accounts, and any rent-reporting services when you initiate a pre-approval. Many platforms give you the option to share more data in exchange for a more accurate rate, and borrowers with strong cash flow who take this step often receive better offers than their FICO score alone would suggest. You can read more about how this works mechanically in our article on how fintech lenders use payroll data to approve borrowers banks would reject.

The soft-pull mechanics work as follows: most fintech pre-approval flows use only a soft credit inquiry at the initial quote stage, meaning your credit score is not affected. Only when you formally accept an offer and proceed to full application does a hard inquiry typically occur. Always confirm this before clicking “apply.”

What to Watch Out For

Be honest about the black-box problem. Regulations now require lenders to provide plain-language explanations for adverse credit decisions, but borrowers rarely see the full weighting behind their offered rate. If you receive a rate that surprises you, you can ask the lender for the specific factors that influenced it. That answer may reveal a correctable issue, an error on your credit report, a high utilization figure, or an income discrepancy, that you can address before negotiating.

According to a Federal Reserve research note, FinTech lenders held approximately 14% of all U.S. personal loans as of end-2022, a share that has grown steadily as alternative data models have expanded access to borrowers underserved by traditional scoring.

Step 3: How to Build a Pre-Approval Stack Across Multiple Lenders

Building a pre-approval stack means deliberately collecting verified offers from three or more lenders before committing to any one of them. This is the foundational move in any fintech pre-approval strategy, and most borrowers skip it entirely.

How to Do This

Start by deciding whether to use a marketplace aggregator or apply individually. Platforms like Credible and LendingTree let you complete one application and receive rate quotes from multiple lenders simultaneously. The efficiency is real: one session can produce four to eight rate quotes with a single soft pull. The trade-off is that some marketplaces accept referral fees from lenders, which can influence which results appear most prominently. The CFPB has issued explicit guidance warning that comparison-shopping tools which accept payments from lenders to manipulate or suppress results may violate federal consumer financial protection law. Always check whether the quotes you receive are sorted by APR rather than sponsored placement.

For individual applications, target a mix of fintech-native lenders, a traditional bank or credit union you already have a relationship with, and one marketplace quote. This combination tends to produce a wider rate spread, giving you stronger material to work with in negotiation. Applying individually takes more time but guarantees you are seeing each lender’s full, unfiltered offer. Understanding your debt-to-income ratio before applying across platforms is worth doing first, it is the number that most quietly determines how competitive your offers will be.

The rate-shopping window matters here. FICO scoring models treat multiple mortgage or auto loan inquiries made within a specific window as a single hard pull. That window is 14 days under some older FICO models and up to 45 days under more recent versions. Because you cannot know in advance which model your lender uses, default to the tighter 14-day window as your target for completing all applications. This is a genuine knowledge gap that most borrowers carry into the process: articles often say “apply within 30 days” as a round number without acknowledging that the 14-day window still applies to some models in active use.

What to Watch Out For

Do not confuse volume with quality. Collecting eight offers from the same type of lender (all personal loan fintech platforms, for example) gives you less negotiating range than collecting three offers from structurally different lenders. A credit union offer, a fintech platform offer, and a traditional bank offer create a broader comparison table and more credible competition when you bring them to the negotiating table.

Timing your applications around the end of a calendar month or fiscal quarter can improve your results. Loan officers working toward volume quotas have measurably more flexibility to approve fee waivers or rate concessions in the final days of a reporting period. For bank and credit union lenders, this is typically the last week of the month. For fintech platforms with quarterly targets, the last two weeks of March, June, September, and December are worth targeting if your timeline allows it.

| Pre-Approval Method | Typical Time to Offers | Number of Offers | Credit Impact | Best For |

|---|---|---|---|---|

| Marketplace Aggregator (Credible, LendingTree) | 10–20 minutes | 4–8 lenders | 1 soft pull | Personal loans, student refinancing |

| Individual Fintech Applications (Upstart, SoFi) | 15–30 minutes each | 1 per application | Soft pull at pre-approval stage | Borrowers with alternative credit data to surface |

| Bank or Credit Union Pre-Approval | 1–3 business days | 1 per institution | Often hard pull at pre-approval | Existing customers leveraging relationship pricing |

| Mortgage-Specific Tools (Rocket Mortgage, Better) | 20–45 minutes | 1 per platform | Soft pull initially; hard pull at full application | Home purchase or refinance comparison |

| Auto Fintech Pre-Approval (Credit unions + fintech) | 5–15 minutes | 1–3 per session | Soft pull at pre-approval | Buyers going to dealership with offer in hand |

Step 4: How to Use Competing Pre-Approval Offers to Negotiate Better Terms

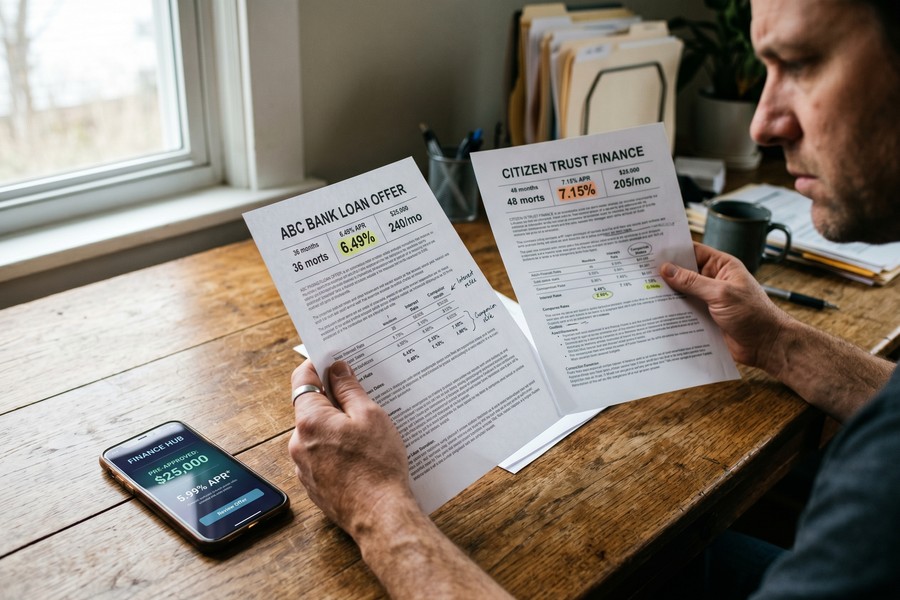

Once you hold two or more verified pre-approval letters with different rates or fee structures, you have the most direct tool available for negotiating: documented proof that another lender will give you better terms. The key is knowing what to say, what to ask for, and what lenders will and will not move on.

How to Do This

Contact your preferred lender, whether that is the one with the best customer service, the existing bank relationship, or the loan structure you prefer, and say directly: “I’ve received a competing pre-approval from [Lender Name] at [X]% with a [Y]% origination fee. I’d prefer to work with you. Are you able to match or beat those terms?” That framing is specific enough to require a real response, and it signals that you have done the work.

Realistic concessions look like this: a rate reduction of 0.125% to 0.25% on a personal loan or mortgage is achievable with a strong competing offer. A full origination fee waiver (often 1% to 3% of the loan amount) is harder to get but not uncommon when the competing offer has a materially lower fee. What lenders will almost never move on: the loan amount limits set by their underwriting criteria, prepayment penalty requirements that are baked into their loan product structure, or rates on government-backed loans where pricing is largely standardized.

Go beyond the interest rate. The CFPB instructs borrowers to request and review multiple Loan Estimates side-by-side, noting that comparing origination charges across lenders is the best way to identify a competitive offer. Use this document as your line-item negotiating tool. Other negotiable terms include auto-pay discounts (typically 0.25% off your rate for enrolling in autopay, which most lenders offer but few borrowers ask about explicitly), flexible repayment start dates, and the removal of prepayment penalties if the competing offer does not include them.

Understanding how loan term length affects total interest cost is worth doing before this conversation. A lender who won’t reduce your rate may still agree to a shorter term that costs you less overall. Our article on how loan term length quietly controls how much interest you pay walks through the math in detail.

What to Watch Out For

The counter-offer conversation only works if your competing offers are genuine and comparable. If you present a personal loan rate from a marketplace aggregator to a mortgage lender, they will dismiss it. Ensure that the competing offers you cite are the same loan type, similar loan amount, and similar term length. Mismatched comparisons undermine your credibility and give the lender an easy reason to decline.

Some fintech lenders have tiered pricing structures where the rate you see in the pre-approval stage adjusts at full application based on documentation review. Always ask whether the pre-approval rate is a firm conditional offer or a range subject to further review. Presenting a “floor” rate that may not apply to your final application as a negotiating chip can backfire when the numbers are verified.

Step 5: How to Protect Your Credit Score Throughout the Pre-Approval Process

Credit score protection is the most common reason borrowers hesitate to collect multiple pre-approvals, and it is also the concern most frequently overstated. The actual risk is small and manageable when you understand how the inquiry rules work.

How to Do This

At the pre-approval stage, confirm with every lender whether their initial review uses a soft or hard pull. Most fintech platforms use only a soft pull for preliminary offers. A soft pull does not appear on your credit report to other lenders and does not affect your score. Only when you formally accept an offer and advance to full underwriting does a hard pull typically occur.

A single hard inquiry causes a 5-to-10-point temporary drop in credit score for most borrowers, according to myFICO. Most scores recover within 3-to-6 months. That is a real but modest cost for a potentially significant improvement in loan terms. When you are comparing it against the potential savings from a 0.25% rate reduction on a $30,000 loan over five years, the math generally favors shopping.

For mortgage and auto loans specifically, FICO’s rate-shopping exception treats multiple hard inquiries of the same loan type made within a window as a single inquiry. Some FICO models use a 14-day window; newer versions (FICO 9 and FICO 10) use a 45-day window. Because you cannot determine in advance which model your lender is using, the safest approach is to complete all your applications within 14 days. That window is narrow, which is exactly why building your shortlist of lenders before you begin and preparing your documents in advance matters.

What to Watch Out For

Be cautious about applying for unrelated credit products, new credit cards, store financing, or a HELOC, during the same period you are collecting loan pre-approvals. Those inquiries are not covered by the rate-shopping exception and will each count individually. Keep the inquiry picture clean for at least 90 days before you begin your pre-approval stack. Also worth noting: if you are applying for a joint loan, both applicants’ credit reports are reviewed. Our article on how co-borrowers with mismatched credit scores affect the interest rate on a joint loan covers the specific dynamics in that scenario.

Before starting your pre-approval process, pull your own credit reports from AnnualCreditReport.com, the federally mandated free source, and review them for errors. Disputing an inaccuracy before lenders review your file can improve your score without any new financial action, sometimes by more than 20 points. This step is free, takes about 30 minutes, and has no credit impact.

Step 6: Matching the Right Fintech Tool to Your Loan Type

The best fintech pre-approval platform for a personal loan is not the best platform for a mortgage. Matching your tool to your loan type determines both the quality of offers you receive and how much negotiating weight those offers carry.

How to Do This

For personal loans, the strongest soft-pull pre-approval platforms include Upstart (which uses alternative data most aggressively and is worth using if your FICO score doesn’t fully reflect your financial health), SoFi (which offers rate-match guarantees in some markets and is strong for borrowers with solid income documentation), and LendingClub (which is particularly useful for debt consolidation comparisons). All three issue conditional offers before a hard pull.

For mortgages, Rocket Mortgage and Better offer digital pre-approval flows that are faster than most traditional lenders, but their pre-approval letters carry real weight with sellers only when accompanied by income and asset verification. Credible is useful as a mortgage rate comparison starting point. Keep in mind that fintech mortgage pre-approvals may carry less weight than a traditional bank’s letter in a competitive real estate market, particularly with sellers or listing agents who view fintech lenders as less certain to close.

For auto loans, obtaining a pre-approved offer from a fintech lender or credit union before visiting a dealership is one of the clearest applications of this strategy. The CFPB advises consumers to obtain a pre-approved loan offer before shopping for a vehicle, specifically because having a loan offer in hand creates negotiating leverage with the dealer’s financing department. Concentrating your auto loan applications within 14 days keeps the credit impact minimal.

Fintech lenders often carry lower overhead costs than traditional banks. In practice, this translates to more flexibility on origination fees and repayment structures for personal and small business loans. However, it does not automatically mean lower APRs across the board. For borrowers with excellent credit, a traditional bank or credit union may still offer the most competitive rate. Fintech’s structural advantage is most pronounced for borrowers in the middle of the credit spectrum, roughly 620 to 740 FICO, where alternative data can change the outcome meaningfully. If you are considering using a fintech platform for student loan refinancing specifically, our guide on using a fintech app to refinance student loans covers the additional factors that apply.

What to Watch Out For

Avoid applying for loan types your profile doesn’t currently support just to create the appearance of competing offers. If a platform quotes you a personal loan rate that reflects a stronger credit profile than you actually have (due to a soft-pull estimate that hasn’t verified income), using that quote as leverage for a mortgage application will break down at verification. Use only offers generated by applications where your real documentation was reviewed.

For borrowers with inconsistent or non-traditional income, such as gig workers or seasonal employees, fintech platforms that evaluate bank account cash flow can be structurally more favorable than traditional lenders. Platforms like Upstart and some credit union digital tools consider monthly cash flow patterns, which may reflect your true repayment capacity better than a W-2-based income calculation. If this describes your situation, our article on digital lending for gig workers between contracts is directly relevant.

Step 7: Keeping Negotiating Leverage Alive Through Closing

Most borrowers treat the pre-approval stage as the negotiation. The better approach is to treat it as the opening move. Significant leverage remains available between pre-approval and closing, and most borrowers walk past it.

How to Do This

Pre-approval letters expire. Most fintech and traditional lender pre-approvals are valid for 60 to 90 days. If your timeline extends beyond that, or if market rates shift meaningfully during the process, request a refreshed pre-approval rather than letting it expire quietly. A refreshed offer based on current conditions may reflect a better rate, or it may confirm that locking in now is the right call. Either way, you are making an informed decision.

Once you are past pre-approval and moving toward closing, request a Loan Estimate, the standardized form that lenders are required to provide under the Truth in Lending Act (TILA) and RESPA. The CFPB has published clear guidance: lenders cannot charge fees beyond a credit report pull before issuing this estimate. Review the Loan Estimate line by line. Origination charges, underwriting fees, application fees, and rate lock fees all appear here, and each one is a potential negotiation point. If a competing lender’s Loan Estimate shows a lower origination charge, bring both documents to your preferred lender and ask them specifically to match the fee, not just the rate.

Junk fees are real. “Administrative fees,” “processing fees,” and “document preparation fees” are not standardized costs, they are revenue items that vary by lender and are frequently waived when a borrower asks. A lender who waives a $500 processing fee in response to a competing Loan Estimate has effectively improved your terms without touching the interest rate, which is exactly the kind of concession most borrowers never think to request.

What to Watch Out For

Watch for fee increases between the Loan Estimate and the final Closing Disclosure. Lenders are bound by tolerance limits on how much certain fees can change, but some fee categories have no cap. Review the Closing Disclosure carefully against your Loan Estimate, and push back in writing on any increase that wasn’t disclosed. The CFPB’s complaint system is a legitimate escalation path if a lender makes unauthorized changes to fees after you’ve locked a rate.

One honest limitation of this entire strategy: it works best when you have time. Borrowers under time pressure, closing in 10 days, needing funds urgently, have less leverage. The 14-day window strategy requires planning. If you are in a time-constrained situation, focus on the marketplace aggregator approach to get multiple quotes in a single session, then concentrate your negotiation on fee waivers, which are easier for lenders to approve quickly than rate changes.

Do not make major financial changes between pre-approval and closing. Opening new credit accounts, changing jobs, or making a large purchase on credit can alter your debt-to-income ratio or credit profile and cause the lender to revise or rescind the offer. The pre-approval you negotiated hard for can disappear if your financial picture changes before the hard pull at full underwriting.

Frequently Asked Questions

Does getting pre-approved by multiple fintech lenders hurt my credit score?

Pre-approvals that use soft pulls do not affect your credit score at all. For pre-approvals that require a hard pull (common at banks and credit unions, and at the full application stage for fintech loans), multiple mortgage or auto loan hard inquiries made within a 14-day window count as a single inquiry under most FICO scoring models. A single hard inquiry typically causes a 5-to-10-point temporary drop, according to myFICO, with recovery in 3 to 6 months, a manageable cost relative to the savings from comparison-shopping.

How many pre-approvals should I get before negotiating?

At least three is the practical minimum for meaningful negotiation. With fewer than three offers, you lack the spread needed to identify whether any offer is genuinely competitive, and lenders know it. Three to five offers from structurally different lenders (one fintech platform, one credit union or bank, one marketplace quote) gives you a credible comparison and real leverage. The CFPB emphasizes that shopping and comparing offers is the most reliable path to better terms.

What should I actually say to a lender when presenting a competing pre-approval offer?

Be direct and specific: “I’ve received a competing pre-approval from [Lender Name] at [X]% APR with a [Y]% origination fee. I prefer to work with you. Can you match or beat those terms?” That phrasing names the competing lender (which forces the lender to take it seriously), states the specific numbers, and expresses a preference that gives the lender a reason to act. Realistic outcomes include a rate reduction of 0.125% to 0.25%, a partial or full origination fee waiver, or both. Lenders are rarely willing to move on rate alone without a documented competing offer to justify the exception internally.

Is a fintech pre-approval as good as a bank pre-approval for a home purchase?

For negotiating loan terms, a verified fintech pre-approval is equally valid. For reassuring a home seller in a competitive market, a traditional bank or credit union pre-approval letter often carries more weight with listing agents who view established institutions as more certain to close. Platforms like Rocket Mortgage and Better have worked to build seller-facing credibility, but some sellers and agents still prefer to see a letter from a recognizable institution. Using both a fintech pre-approval (for negotiating your rate) and a bank pre-approval (for making an offer) is a legitimate dual-track approach.

Can I negotiate loan terms after I’ve already been pre-approved?

Yes, and this is one of the most underused moves in the process. Once you have a Loan Estimate from one lender, you can bring it to another lender and ask them to beat specific line items, including origination fees, underwriting fees, and rate lock fees. The CFPB specifically instructs borrowers to compare Loan Estimates side by side and use that comparison to identify competitive offers. Negotiation does not end at pre-approval, it continues through the Loan Estimate and Closing Disclosure stages.

What fintech platforms give the best pre-approval odds for borrowers with thin credit files?

Platforms that use alternative data models are the strongest choice for borrowers with limited credit history. Upstart explicitly evaluates cash flow, employment patterns, and education in addition to credit score. SoFi gives significant weight to income stability and career trajectory. Both issue soft-pull pre-approvals before committing to a hard inquiry. Proactively linking bank accounts that show consistent deposits and positive cash flow can improve the offer you receive from these platforms, since the underwriting model will factor in account behavior data you have actively surfaced.

How long does a fintech pre-approval last, and what happens if it expires?

Most fintech and bank pre-approvals are valid for 60 to 90 days. After that, the lender considers your financial data stale and the conditional commitment is no longer binding. If your pre-approval expires before you close, request a refresh. A refreshed pre-approval requires a new credit pull and documentation review, but it also gives you current market rates, which may be better or worse than the original offer. If rates have moved favorably during your process, expiration can actually work in your favor.

Should I use a fintech loan aggregator like LendingTree or apply directly to each lender?

Aggregators offer speed and convenience: one application can return four to eight rate quotes with a single soft pull, which is useful for an initial market scan. The trade-off is that the CFPB has warned that some comparison platforms accept payments from lenders to influence result rankings. Use aggregators as a starting point to understand the rate range available to you, then apply directly to your top two or three candidates for verified pre-approvals that carry real negotiating weight. Direct applications take more time but produce cleaner, unsponsored offers.

What other loan terms besides the interest rate can I negotiate with fintech lenders?

Origination fees (typically 1% to 8% of the loan amount on personal loans), auto-pay discounts (often 0.25% off your rate), prepayment penalty removal, flexible repayment start dates, and administrative fee waivers are all realistic negotiation targets. Many fintech lenders have internal flexibility on fees even when rate changes require underwriter approval. Reviewing the full Loan Estimate line by line and asking specifically about each fee category is the most direct way to identify what is negotiable with a given lender.

Sources

- Consumer Financial Protection Bureau, Explore Loan Options and Pre-Approval Guidance

- Consumer Financial Protection Bureau, Request and Review Multiple Loan Estimates

- Consumer Financial Protection Bureau, Guidance on Rigged Comparison-Shopping Results

- Consumer Financial Protection Bureau, Buying a Car: Pre-Approval and Negotiating Guidance

- Federal Reserve Board, FEDS Note: FinTech-Issued Personal Loans in the U.S.

- myFICO, Credit Checks and Inquiries: Hard vs. Soft Pulls Explained

- Federal Reserve Board, Consumer Credit Statistical Release (G.19)