Fact-checked by the CapitalLendingNews editorial team

Quick Answer

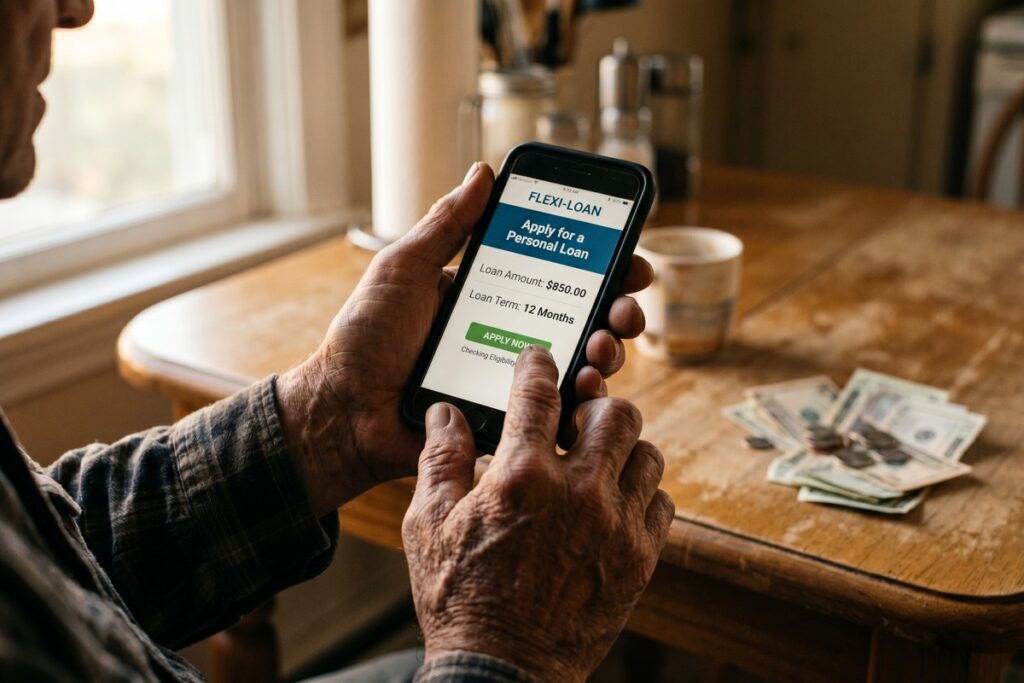

Seniors on fixed income can access digital loans fixed income options by documenting all income sources (Social Security, pension, 401(k) distributions), calculating their debt-to-income ratio before applying, using soft-inquiry prequalification tools across multiple lenders, and reviewing Truth-in-Lending disclosures before accepting. Most online applications take 15 to 30 minutes to complete, with funding in as little as one to two business days.

Getting a digital loan on a fixed income is entirely possible, but it requires a different strategy than what a salaried borrower would use. Under the Equal Credit Opportunity Act (ECOA), lenders are legally prohibited from denying credit solely because income comes from Social Security or other public assistance programs, which means fixed-income seniors start from a stronger legal position than many assume. The real barrier is math: a tight budget leaves almost no room for a new monthly payment, and lenders know it. According to an Employee Benefit Research Institute poll reported by CNBC, 68% of retirees ages 62 to 75 carried outstanding credit card debt in 2024, up from 40% in 2022, a sign that more older Americans are turning to credit to cover gaps their income cannot.

What makes this moment different is the scale of the pressure. The Senior Citizens League’s 2024 Loss of Buying Power study found that the average Social Security benefit has lost 20% of its buying power since 2010. Meanwhile, the digital lending market has matured to a point where seniors with smartphones, 78% of adults 65 and older owned one, per Pew Research Center, can access loan products that were simply unavailable a decade ago. The challenge is knowing which products are appropriate, which are dangerous, and how to present a fixed income in the most accurate light.

This guide is written for adults on Social Security, pension income, or other fixed retirement income who need to borrow responsibly. By following the steps below, you will know how to calculate whether a loan is truly affordable, how to document your income properly, which digital lenders are realistic options, and how to protect yourself from the predatory outfits that specifically target this demographic.

Key Takeaways

- The Equal Credit Opportunity Act prohibits lenders from refusing or discounting Social Security income during underwriting, according to the Consumer Financial Protection Bureau, but a debt-to-income ratio above 43% will still disqualify most applicants regardless of income source.

- Total debt held by Americans aged 70 and older grew 36.2% over five years through Q1 2025, making them the fastest-growing age group of borrowers, per an analysis of Federal Reserve Bank of New York data.

- The average Social Security benefit has lost 20% of its buying power since 2010, according to The Senior Citizens League’s 2024 study, which is why so many fixed-income seniors are seeking loans to cover everyday costs.

- Reporting your gross Social Security income (before Medicare Part B deductions) rather than your net bank deposit gives lenders a more accurate and favorable picture of your qualifying income, a documentation distinction most applicants miss.

- Older adults who qualify for but are not enrolled in benefits programs leave an estimated $30 billion in assistance unclaimed annually, according to the National Council on Aging’s BenefitsCheckUp program, making non-debt solutions the right first step for many.

- Financial exploitation of older adults costs an estimated $27 billion annually according to the FDIC, which is why recognizing predatory digital lenders is as important as finding legitimate ones.

In This Guide

- Why Borrowing on a Fixed Income Is a Different Problem Entirely

- What Do Lenders Actually See When a Senior Applies for a Digital Loan?

- Which Digital Loan Options Are Realistic for Seniors on Fixed Income?

- How Do I Know If I Can Actually Afford a New Loan on My Fixed Income?

- How Do I Apply for a Digital Loan Online as a Senior Step by Step?

- How Do I Spot Scam Lenders Targeting Seniors Online?

- Should I Try Non-Debt Alternatives Before Taking Out a Digital Loan?

- Frequently Asked Questions

Step 1: Why Borrowing on a Fixed Income Is a Different Problem Entirely

The core challenge for fixed-income seniors is not simply qualifying for a loan. It is that any new monthly payment immediately competes with rent, prescriptions, and groceries on a budget that does not grow. A salaried worker who takes on a new loan payment can theoretically earn more next year. A retiree on Social Security cannot. That structural difference changes the entire risk calculation.

The Debt-to-Income Squeeze

The debt-to-income ratio (DTI) is the number lenders focus on most, and it is the silent disqualifier for many fixed-income applicants whose credit scores are perfectly acceptable. DTI is calculated by dividing your total monthly debt obligations by your gross monthly income. Most conventional lenders want to see a DTI below 36%, and they will rarely approve anyone above 43%. A retiree receiving $1,800 per month in Social Security who already carries $500 per month in minimum debt payments has a DTI of roughly 28%, workable, but with very little room. Adding even a modest $250 monthly loan payment pushes that DTI to 42%, right at the edge of disqualification. Understanding this arithmetic before applying is the single most important preparation step.

Legal Protections That Already Exist

The CFPB is explicit: lenders are prohibited from discounting or refusing to consider income derived from public assistance programs, including Social Security and SSI, when evaluating a loan application. Credit scoring systems may not disfavor applicants aged 62 or older. The National Credit Union Administration (NCUA) supervises federal credit unions for compliance with these same ECOA fair lending requirements. Knowing this matters because some lenders still behave as though age or income source is a legitimate reason to deny credit, and borrowers who know the law are in a position to push back.

Debt in retirement has become statistically normal, not exceptional. GAO data shows the share of older households (age 50 and above) carrying debt rose from 58% in 1989 to 71% in 2016, with median debt nearly tripling in inflation-adjusted terms. The question has shifted from whether seniors should borrow to how they can do so safely, within a budget that genuinely has no slack to absorb a mistake.

The CFPB’s Office for Older Americans estimates that over 23 million Americans age 60 and older are economically insecure, which means the pressure driving seniors toward digital loans is widespread, not an edge case.

Step 2: What Do Lenders Actually See When a Senior Applies for a Digital Loan?

When a senior submits an online loan application, underwriters, whether human or algorithmic, evaluate four core factors: income documentation, credit score, DTI ratio, and collateral. How each one plays out is meaningfully different for a retiree than for a salaried worker, and understanding those differences prevents avoidable rejections.

Income Documentation: The Gross vs. Net Trap

One of the most consequential and least-discussed distinctions in senior lending is the difference between gross and net Social Security income. Lenders calculate DTI using gross benefit amounts, the figure before Medicare Part B premium deductions. The standard Medicare Part B premium is $185 per month, and many enrollees pay more if income-related surcharges (IRMAA) apply. A senior who reports only the net amount that deposits in their bank account is underreporting their qualifying income and may appear less creditworthy than they actually are. Always report gross benefit amounts and document them with the official SSA benefits verification letter, available at no cost through the Social Security Administration’s website.

The Income Source Bias Problem

Some lenders’ systems are optimized for W-2 income verification, and loan officers may not proactively count pension allotments, 401(k) distributions, annuity payments, or investment dividends when reviewing an application. This is a documentation failure, not an income reality. Borrowers must assert every countable income source explicitly and provide documentation for each one: award letters, 1099-R forms, brokerage statements, or annuity payment confirmations. As our guide on how fintech lenders use non-traditional data to approve borrowers banks would reject explains, newer platforms are improving at reading alternative income signals, but the burden of documentation still falls on the applicant.

Informal Age Cutoffs: What They Are and How to Respond

Some lenders impose informal age cutoffs, a reluctance to approve applicants over 75, for instance, even though the ECOA explicitly prohibits age-based discrimination in credit decisions. This behavior is often not stated directly. It shows up as unexplained denials or requests for documentation that younger borrowers would never face. If you suspect age discrimination played a role in a denial, you have the right to request the specific reasons for the decision in writing. A denial based solely on age or the type of income received is reportable to the CFPB at consumerfinance.gov.

A credit score above 670 does not guarantee approval if your DTI ratio is already elevated. Many seniors are surprised to learn their credit is fine but their budget arithmetic is the problem. Calculate DTI before applying so you are not blindsided by a denial that damages your score and leaves you no better off.

Step 3: Which Digital Loan Options Are Realistic for Seniors on Fixed Income?

The realistic loan options for a fixed-income senior depend primarily on one factor: homeownership status. Renters are limited to unsecured personal loans from online lenders or credit unions. Homeowners have a broader set of options, including home equity products and reverse mortgages, but broader does not always mean better, and each comes with trade-offs worth understanding clearly.

For Renters: Unsecured Personal Loans and Credit Union Products

Online personal loan marketplaces such as Credible, Upgrade, and Universal Credit allow borrowers to compare offers from multiple lenders with a single soft inquiry. Loan amounts typically range from $1,000 to $50,000, with APRs ranging broadly based on credit profile. Federal credit unions are structurally friendlier to fixed-income applicants than most banks: they are capped at a maximum interest rate of 18% APR by law, they tend to use relationship-based underwriting, and they often have lower minimum income requirements than commercial digital lenders. If you are already a member of a credit union, start there.

For Homeowners: Home Equity and Reverse Mortgage Options

Homeowners have access to home equity loans, home equity lines of credit (HELOCs), and Home Equity Conversion Mortgages (HECMs), the FHA-insured reverse mortgage available to homeowners aged 62 and older. A HECM eliminates the monthly payment obligation entirely by converting equity to cash and deferring repayment until the home is sold or vacated, which makes it one of the few borrowing mechanisms that genuinely does not add to monthly budget strain. The trade-off is real: a HECM reduces the estate’s value, carries ongoing mortgage insurance premiums, and can become complicated if a surviving spouse is not a co-borrower. For more on how loan structure affects total cost over time, see our analysis of how loan term length quietly controls how much interest you actually pay.

The Options Most Articles Skip

Two borrowing mechanisms are almost never mentioned in senior lending content despite being among the most favorable options available. First, CD-secured loans: if you hold a certificate of deposit at a credit union or bank, many institutions will lend against it at a rate only 1 to 2 percentage points above the CD rate. The credit check is minimal since the deposit serves as collateral, and the interest cost is modest. Second, life insurance policy loans: if you hold a whole life or universal life insurance policy with accumulated cash value, you can borrow against that value with no credit check and no income verification. The loan accrues interest against the policy’s death benefit, but there is no monthly payment obligation. Both options require existing assets, but for seniors who have those assets, the terms are far more favorable than most unsecured digital loans.

As of Q4 2025, total outstanding personal loan debt in the U.S. reached $276 billion, the highest in 20 years of available data, with 26.4 million Americans holding a personal loan, according to a LendingTree analysis of TransUnion data. Personal loans are not a niche product; they are mainstream, and the approval infrastructure now exists across hundreds of online platforms.

| Loan Type | Best For | Typical APR (Jan 2026) | Credit Check Required | Monthly Payment | Key Trade-Off |

|---|---|---|---|---|---|

| Credit Union Personal Loan | Renters with fair-to-good credit | 9% – 18% (capped by law) | Yes | Yes | Must be a member; may have lower limits |

| Online Marketplace Loan (Upgrade, Universal Credit) | Borrowers comparing multiple offers quickly | 9.99% – 35.99% | Soft inquiry for prequalification | Yes | Wide rate range; origination fees of 1%–9% |

| CD-Secured Loan | Seniors with existing CDs who want low rates | CD rate + 1% to 2% | Minimal (collateral-based) | Yes | Requires existing deposit; locks CD funds |

| Life Insurance Policy Loan | Seniors with whole/universal life cash value | 5% – 8% (policy-set) | None | None required | Reduces death benefit; accrues interest silently |

| HECM Reverse Mortgage | Homeowners 62+ who want no monthly payment | Variable or fixed; current MCA rates near 6%–7% | Yes (financial assessment) | None required | Reduces home equity; fees are significant |

| HELOC | Homeowners needing flexible access to funds | Prime + 0.5% to 2% (roughly 8%–10% in Jan 2026) | Yes | Interest-only during draw period | Variable rate can rise; home is collateral |

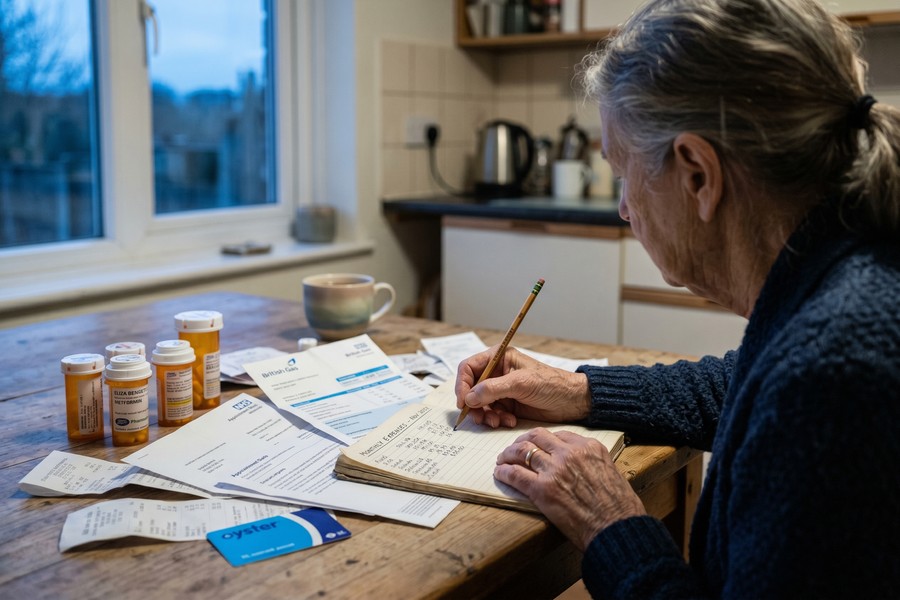

Step 4: How Do I Know If I Can Actually Afford a New Loan on My Fixed Income?

Before submitting any application, run a fixed-income affordability test. This is not optional. It is the step that separates a manageable loan from one that crowds out grocery money three months in. The goal is to confirm, with real numbers, that a new monthly payment fits within your income without touching funds earmarked for essential expenses.

The Pre-Application Checklist

Start by listing every source of monthly income and its gross amount: Social Security (use the gross figure, before Medicare deductions), pension distributions, 401(k) or IRA withdrawals, annuity payments, dividends, rental income, and any part-time earnings. Add those together to get your total gross monthly income. Next, list every current monthly debt obligation: mortgage or rent, minimum credit card payments, car loans, student loans, medical payment plans, and any other recurring debt. Divide total monthly debt obligations by total gross monthly income. That is your current DTI.

A Realistic Example

A borrower receiving $1,800 per month in Social Security and $600 per month in pension income has a gross monthly income of $2,400. If current debt obligations total $500 per month (a rent-equivalent or credit card minimum), the current DTI is about 21%, comfortable. A $250 per month loan payment would push DTI to roughly 31%, still within the 36% caution zone but leaving almost no buffer. A $400 per month loan payment would push DTI to 38%, which most lenders will flag as elevated risk. Running this calculation before applying tells you the maximum monthly payment you can support and, working backward using any standard loan calculator, the maximum loan amount at a given term and rate.

Setting Your Hard Ceiling

The affordability test should also account for real expenses that do not show up in DTI calculations: prescriptions, medical copays, transportation, and food. Set a maximum monthly payment that leaves at least $200 to $300 in monthly breathing room after all expenses, not just debt obligations. If no loan payment fits within that constraint, borrowing is the wrong tool for the current problem, and the next section on non-debt alternatives becomes the more relevant read.

The NCOA’s BenefitsCheckUp tool, available at ncoa.org, is a free resource that helps older adults identify every benefit program they qualify for before deciding whether a loan is actually necessary. Many seniors discover, after using it, that their monthly budget gap is largely closable through unclaimed benefits rather than new debt. According to the National Council on Aging, an estimated $30 billion in benefits goes unclaimed annually by older adults who qualify but are not enrolled.

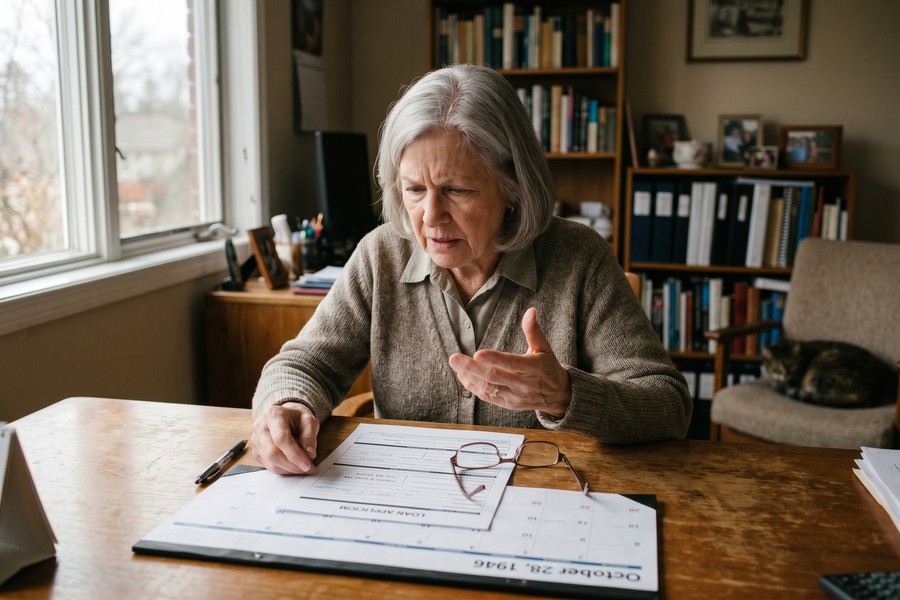

Step 5: How Do I Apply for a Digital Loan Online as a Senior Step by Step?

The digital application process is more straightforward than many seniors expect, but the order of operations matters. Doing it wrong, specifically submitting hard-pull applications before comparing offers, can damage your credit score without improving your chances of approval.

How to Do This

Follow these steps in sequence:

- Gather your documents before you touch any application. You will need: your SSA benefits verification letter (print it at ssa.gov or request it by phone), the most recent statements for any pension or retirement account distributions, three months of bank statements showing consistent deposits, your most recent federal tax return, and documentation for any additional income sources you plan to assert.

- Pull your free credit report. Visit AnnualCreditReport.com, the only federally authorized source, and review all three bureau reports for errors before applying. Disputing errors in advance takes two to three weeks but can meaningfully improve your score.

- Use soft-inquiry prequalification tools first. Most reputable online lenders and marketplaces offer prequalification that uses a soft credit pull, which does not affect your score. Platforms like Credible and Upgrade allow you to see estimated rates and terms without committing. Use this step across two or three lenders simultaneously to compare APRs and origination fees side by side. Our overview of how DTI affects your digital lending application covers what lenders are looking for behind those prequalification screens.

- Submit a full application only with your chosen lender. The hard-pull credit inquiry happens at this stage. Submitting multiple hard-pull applications within a short window (typically 14 to 45 days, depending on the scoring model) may be treated as a single inquiry for rate-shopping purposes, but the safest approach is to identify your preferred offer through prequalification first.

- Read the Truth-in-Lending disclosure before accepting. The TILA disclosure shows the annual percentage rate (APR), total loan cost, and monthly payment in standardized format. Confirm the rate is fixed (not variable), that there is no prepayment penalty, and that the monthly payment matches your affordability calculation. Sign only after reviewing this document.

What to Watch Out For

Some digital lenders bury origination fees of 1% to 9% of the loan amount, which are deducted from the disbursement. A $10,000 loan with a 6% origination fee delivers only $9,400 but requires repayment of the full $10,000 plus interest. Always check the disbursed amount against the loan amount in the Truth-in-Lending disclosure. Also confirm that loan funding goes directly to your bank account, not to a third-party contractor or vendor, which is a common structure in predatory home-repair loan scams.

If you are uncomfortable navigating digital forms alone, a HUD-certified housing counselor or a nonprofit credit counselor affiliated with the National Foundation for Credit Counseling (NFCC) can sit with you through the application process at no charge. This is not just for mortgage issues; these counselors are trained in the full range of consumer lending products.

Step 6: How Do I Spot Scam Lenders Targeting Seniors Online?

Financial exploitation of older adults is not a fringe problem. It costs an estimated $27 billion annually according to the FDIC, and digital lending has created new delivery channels for old scams. The goal of this section is not to create fear around online borrowing. It is to give you specific, concrete signals that distinguish a legitimate lender from a predatory one.

Red Flags That Identify Predatory Lenders

Any of the following should stop the application immediately:

- Upfront fees before funding. Legitimate lenders deduct fees from the loan disbursement or collect them at closing. No legitimate lender requires a wire transfer or gift card payment before releasing funds. Full stop.

- “Guaranteed approval” language. The CFPB identifies guaranteed approval claims as a regulatory red flag. Every legitimate lender evaluates creditworthiness before approving. A lender promising approval regardless of income or credit history is not a lender.

- Requests for direct bank account access to “disburse funds.” Legitimate lenders use ACH transfers initiated by the lender to a verified account. Any request to share online banking login credentials is a fraud vector.

- No verifiable state license. Every consumer lender operating in a given state must be licensed by that state’s financial regulator. You can verify licensing through the Nationwide Multistate Licensing System (NMLS) consumer access portal at nmlsconsumeraccess.org.

The Home-Repair Loan Scam Specifically

One predatory structure targets seniors with home equity more than any other. A contractor offers easy digital financing for a roof repair, HVAC replacement, or other urgent project. The financing is arranged through a third-party lender whose terms, adjustable rates, balloon payments, prepayment penalties, are buried in a long digital contract signed on a tablet at the door. By the time the contract terms become clear, the contractor has been paid and the senior holds a loan they did not fully understand. The protection is simple: never sign financing documents presented by a contractor without a 24-hour review period, and never accept financing from a lender you did not independently research before the contractor’s visit.

How to Report Suspected Fraud

If you encounter or have already been victimized by a predatory lender, report to all of the following: the CFPB complaint portal at consumerfinance.gov, the Federal Trade Commission at reportfraud.ftc.gov, your state attorney general’s consumer protection division, and the Eldercare Locator at 1-800-677-1116 for a referral to Adult Protective Services.

A default judgment on an unsecured personal loan can result in a lien against your home, even though Social Security income itself is generally protected from garnishment by private creditors. The “my Social Security is protected” assumption is only partially true for homeowners. Defaulting on any loan where you have home equity carries real risk of losing that equity through a court judgment.

Step 7: Should I Try Non-Debt Alternatives Before Taking Out a Digital Loan?

For retirees whose DTI is already at or above 36% before a new loan, digital borrowing is not the right first move. The honest answer is that non-repayable government benefits and nonprofit resources should come first, because they permanently reduce monthly expenses without adding a payment obligation.

Benefit Programs That Close Budget Gaps Without Creating Debt

The programs below are underutilized despite covering real costs that drive seniors toward loans:

- SNAP (Supplemental Nutrition Assistance Program): Food assistance for income-eligible seniors; many retirees qualify but are not enrolled because they assume the benefit is for people with no income at all.

- LIHEAP (Low Income Home Energy Assistance Program): Covers heating and cooling costs, addressing one of the most variable and budget-threatening expense categories for seniors on fixed income.

- Medicare Savings Programs: Four separate programs that pay some or all Medicare premiums, deductibles, and copayments for income-qualifying enrollees, potentially saving hundreds of dollars per month.

- Property Tax Relief Programs: Most states offer property tax exemptions, deferrals, or freezes for senior homeowners above a certain age or below a certain income threshold. These programs vary by state and county but can represent significant annual savings.

The NCOA’s BenefitsCheckUp tool screens for over 2,500 federal, state, and local programs based on a brief intake questionnaire. Given that $30 billion in benefits goes unclaimed annually, the probability that a fixed-income senior who has never used this tool qualifies for at least one unclaimed program is high.

Nonprofit Credit Counseling as a Free First Step

A counselor affiliated with the National Foundation for Credit Counseling (NFCC) or a HUD-certified housing counseling agency will review your full income and expense picture at no cost, negotiate with existing creditors on your behalf if needed, and model whether a specific loan amount is genuinely affordable before you apply. This service is particularly valuable for seniors who are not sure whether their budget problem is a short-term cash-flow issue or a structural mismatch that a loan cannot fix.

Cash Advance Apps: Appropriate Use and Misuse

A small number of cash advance apps, including Cleo and Dave, accept Social Security income and do not run hard credit checks or evaluate DTI. These tools provide advances of $20 to $500 against an upcoming deposit, typically with a small subscription fee rather than interest. Their appropriate use is narrow: covering a gap of a few days between a benefit deposit and an essential expense when no other option exists. Their misuse is equally common: treating a small recurring advance as a supplement to income creates a cycle of dependency that erodes the benefit deposit every month before it arrives. If you are using a cash advance app more than once every two or three months, the underlying budget problem needs a different solution than a digital loan of any kind. For a fuller look at how fintech platforms handle irregular income scenarios, our guide on digital lending for borrowers navigating income gaps covers comparable dynamics.

Frequently Asked Questions

Can I get a personal loan if my only income is Social Security?

Yes, Social Security income alone can qualify you for a personal loan. The CFPB confirms that lenders cannot legally disregard Social Security income during underwriting. The practical barrier is whether your monthly benefit, after existing debt obligations, leaves enough room for an additional payment. Lenders will still evaluate your DTI ratio, and a DTI above 43% will disqualify most applicants regardless of income source.

What credit score do I need to get approved for an online loan as a retiree?

Most online personal loan lenders target borrowers with credit scores of 580 or above, though rates improve significantly at 670 and above. Federal credit unions are generally more flexible and may approve borrowers with scores in the 560 to 580 range, especially for smaller loan amounts. A low credit score combined with limited income is a harder problem: focus on getting your DTI down and disputing any credit report errors before applying.

Will applying for a digital loan hurt my credit score?

Using soft-inquiry prequalification tools, available at most major online lenders and marketplaces, does not affect your credit score. The hard credit pull that does affect your score only happens when you submit a formal application to a specific lender. If you submit multiple formal applications within a 14 to 45 day window, most scoring models (including FICO 9) treat those as a single inquiry for rate-shopping purposes, minimizing the impact.

How do I prove my income to an online lender when I don’t have a pay stub?

Request a benefits verification letter directly from the Social Security Administration. It is available at no cost through the SSA’s online portal or by calling 1-800-772-1213. This letter serves the same function as a pay stub. Supplement it with three months of bank statements showing consistent SSA deposit amounts, plus any 1099-R forms for pension or retirement account distributions. The key is documenting every income source separately; lenders count what you prove, not what you describe.

Are there digital loans specifically designed for seniors on fixed income?

No category of loan product is formally designated “for seniors,” but federal credit unions, CDFI (Community Development Financial Institution) lenders, and some state-chartered credit unions structure their underwriting in ways that are systematically friendlier to fixed-income applicants: lower minimum income requirements, relationship-based decisions, and rate caps. HECM reverse mortgages, while not personal loans, are the only FHA-insured product specifically restricted to borrowers aged 62 and older and structured to eliminate monthly payment requirements.

Can a creditor garnish my Social Security if I default on a digital loan?

Private creditors generally cannot garnish Social Security benefits directly under federal law. However, this protection is more limited than it sounds for homeowners. A creditor who obtains a court judgment can place a lien on your home, which means the debt could be collected when the home is sold or refinanced. For fixed-income seniors with home equity, a loan default carries real risk beyond credit score damage, a nuance that many guides omit entirely.

What documents do I need to apply for a loan online as a senior?

You will need: a government-issued ID, your Social Security benefits verification letter showing gross benefit amount, three months of bank statements showing regular deposits, your most recent federal tax return (Form 1040), and documentation for any additional income sources such as 1099-R forms for pensions or annuity payment statements. Having all documents in digital form (PDF or clear photo) before starting the application prevents delays and reduces the chance of timeouts on lender platforms.

Should I take out a personal loan to cover a medical bill if I’m on Medicare?

Before borrowing for a medical bill, contact the hospital or provider’s billing department directly and ask about financial assistance programs, charity care, or an extended payment plan at 0% interest. Most nonprofit hospitals are required by law to offer financial assistance programs. A 0% payment plan eliminates the need for a loan entirely. If the bill is already with a collections agency, negotiating a reduced settlement is often possible, and that negotiation does not require taking on new debt. A nonprofit credit counselor can help structure this conversation at no cost to you.

What’s the difference between a HELOC and a home equity loan for a senior on fixed income?

A home equity loan provides a lump sum at a fixed interest rate with a predictable monthly payment, generally safer for fixed-income borrowers because the payment does not change. A HELOC is a revolving line of credit with a variable rate that can rise, and payments increase as the rate rises. For seniors on fixed income, the payment predictability of a fixed-rate home equity loan is almost always preferable to the variable structure of a HELOC, even if the initial HELOC rate is slightly lower. Our analysis of installment loans versus revolving credit lines for home repairs covers this trade-off in detail.

How do I report a predatory lender that targeted me online?

File a complaint with the CFPB at consumerfinance.gov (under “Submit a complaint”), with the FTC at reportfraud.ftc.gov, and with your state attorney general’s consumer protection division. If you believe you were targeted because of your age, also contact the Eldercare Locator at 1-800-677-1116, which connects callers to Adult Protective Services and local legal aid organizations that handle elder financial exploitation cases. Acting quickly matters: some predatory lenders move funds offshore rapidly after fraud reports begin.

Sources

- Consumer Financial Protection Bureau, Can a lender consider my age or income source when deciding to give me a loan?

- National Credit Union Administration, Equal Credit Opportunity Act Nondiscrimination Requirements

- National Council on Aging, BenefitsCheckUp and Benefits Access for Older Adults

- CFPB Office for Older Americans, Age-Friendly Banking Initiative

- CNBC, Credit card debt among retirees jumps significantly (EBRI data, 2024)

- The Kaplan Group, The State of American Debt 2025: 36% Debt Growth Among Seniors

- The Senior Citizens League, Social Security Benefits Have Lost 20% of Buying Power Since 2010

- Pew Research Center, Internet Use and Smartphone Ownership: Digital Divides in the U.S. (2025)

- LendingTree, Personal Loan Statistics (TransUnion data, Q4 2025)

- National Council on Aging, New Online Tool Helps Older Adults Manage Their Finances