Reviewed by the CapitalLendingNews Editorial Team

Our Take

For caregivers managing irregular income and urgent care-related expenses, digital personal loans from fintech lenders are the strongest first option, faster approval, more flexible income verification, and funding within 1-2 business days beats what most traditional banks offer. This holds when your credit score sits above 620 and your debt-to-income ratio stays under 43%. The case for credit unions wins when you have time to apply, a stable pay history, and a credit score above 700; their rates consistently beat fintech platforms. For everyone else, digital is the practical answer.

Family caregivers are quietly carrying one of the most significant financial burdens in the U.S. economy. According to AARP’s 2024 research on financial supports for family caregivers, nearly 80% of family caregivers absorb out-of-pocket care costs averaging $7,200 per year, money that comes directly out of the same income pool used to pay rent, groceries, and existing debt. That math gets brutal fast when someone else’s health depends on your paycheck holding steady.

This article is for caregivers who need to borrow and want to know which path makes the most sense given their specific financial situation. What makes digital loans for caregivers work, or fail, comes down to how a lender reads your income story, and that story is rarely simple.

Key Takeaways

- Nearly 80% of family caregivers face average out-of-pocket costs of $7,200 annually, according to AARP (2024), directly reducing the income available to service new debt.

- 12% of caregivers have already taken out a loan or borrowed from family or friends to cover caregiving costs, per AARP’s caregiver financial impact data.

- Digital personal loan platforms typically fund in 1-2 business days, compared to 3-7 days at traditional banks, a critical difference when a care need is urgent and the expense cannot wait.

- Many fintech lenders now use bank-statement and cash-flow underwriting instead of W-2 employment verification, which directly benefits caregivers with reduced or variable work hours. This is a meaningful structural advantage, not marketing language.

- Caregivers managing two households should treat their debt-to-income (DTI) ratio as the make-or-break number: most digital lenders cap approval at 43-50% DTI, and care-related expenses can push many applicants past that threshold before they even apply.

The Hidden Financial Strain Caregiving Places on Your Income

Caregiving costs don’t announce themselves as a line item, they accumulate as a slow drain across medical supplies, home modifications, transportation, and reduced work hours. The $7,200 annual average from AARP breaks down to roughly $600 per month in added pressure on a household that is likely already stretched. For a caregiver earning $48,000 per year, that’s 15% of gross income disappearing into care costs before a single debt payment is made.

Here’s the thing: the financial strain isn’t only the money spent. It’s also the income not earned. Caregivers frequently reduce their own work hours to attend medical appointments, manage medications, or respond to health crises. That reduced income can show up in a lender’s underwriting model as volatility or inconsistency, which is exactly the kind of profile that gets rejected at a traditional bank, even when the borrower’s actual repayment capacity is sound.

The Expense Types That Hit Hardest

The categories that drive sudden, large borrowing needs among caregivers include home modifications (wheelchair ramps, walk-in showers, grab bars), assistive technology, emergency respite care, and uncovered medical equipment. These aren’t predictable budget items. They arrive abruptly, often triggered by a hospitalization or a change in care needs, and they rarely wait three to five business days for a bank to approve a loan.

What I see in practice: Caregivers often underestimate how quickly their debt-to-income ratio deteriorates once care costs start layering onto existing obligations. A reader managing a parent’s dementia care while carrying a car payment and student loan is frequently over 40% DTI before applying for a single new dollar of credit.

Why Traditional Banks Often Fail Caregivers at the Worst Moment

Traditional bank lending is built around a borrower profile that caregivers rarely fit: full-time W-2 employment, stable year-over-year income, no gaps in work history, and a debt-to-income ratio below 36%. That profile describes someone who isn’t managing another adult’s daily health needs.

Income verification is the first obstacle. Banks typically require two to three years of tax returns and recent pay stubs. A caregiver who reduced hours from full-time to part-time 18 months ago, or who shifted to self-employment or gig work to gain schedule flexibility, will show income that’s declining on paper, regardless of whether current cash flow is stable. That backward-looking model doesn’t serve people whose financial lives changed to accommodate care responsibilities.

Collateral and Timeline Problems

Traditional secured loans, including home equity lines of credit, require property ownership and a weeks-long appraisal and approval process. Many caregivers don’t own property, or they’ve already used equity to cover prior care costs. Unsecured bank personal loans require strong credit histories that thin files, common among caregivers who paused full-time work, can’t always support. The approval timeline alone, typically 3-7 business days after application, is too slow when a hospital discharge is happening Thursday and the home modification needs to be in place by Friday. As we’ve covered separately for gig workers facing income gaps, the borrowers banks are slowest to serve are often the ones with the most urgent and legitimate needs.

How Digital Loans Actually Address Caregiver-Specific Borrowing Needs

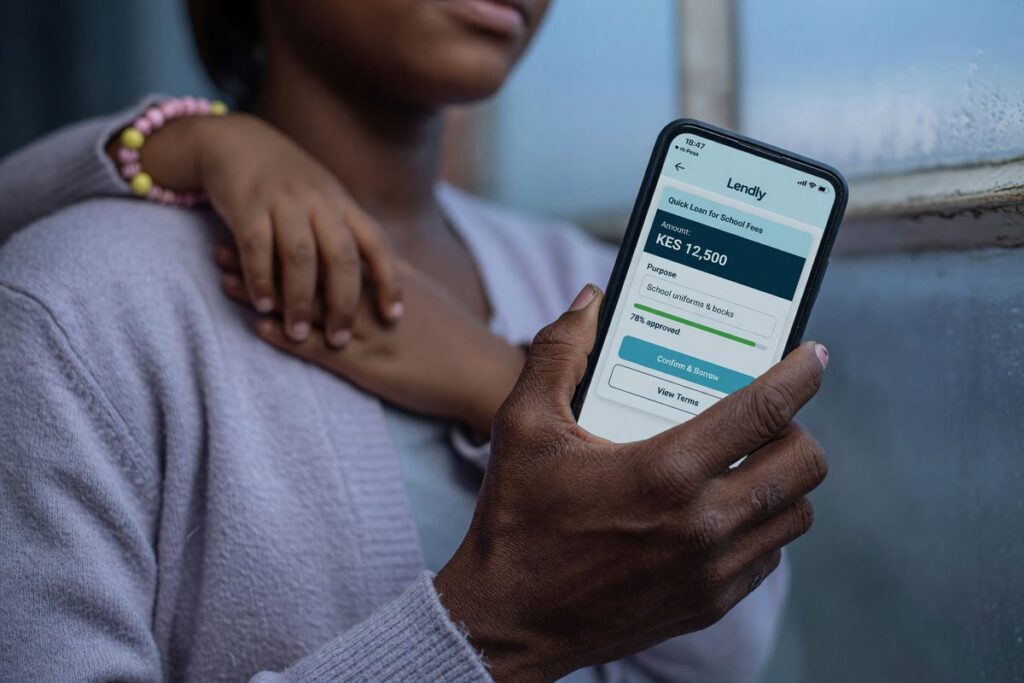

Fintech personal loan platforms solve the two most concrete problems caregivers face: speed and flexible income documentation. The funding timeline advantage is real, most major digital lenders including LightStream, Upstart, SoFi, and LendingClub fund approved borrowers within 1-2 business days. That timeline matches the sudden-expense reality of caregiving in a way that bank loan processing simply doesn’t.

The more structurally important advantage is alternative data underwriting. Several fintech platforms now use bank-statement analysis or open-banking cash-flow models rather than relying exclusively on W-2 verification. For a caregiver who left salaried employment to care for a parent but still earns consistent part-time or contract income, this approach reads the actual transaction history, recurring deposits, regular bill payment, low overdraft frequency, rather than penalizing a pay stub that reflects reduced hours. This is the same mechanism that allows fintech lenders to approve borrowers traditional banks routinely reject, and caregivers benefit from it directly.

Comparing Actual Loan Types by Caregiver Scenario

| Loan Type | Typical APR Range | Funding Timeline | Income Verification | Best For |

|---|---|---|---|---|

| Fintech Personal Loan | 9% – 36% | 1-2 business days | Bank statements or W-2 | Urgent needs, variable income |

| Credit Union Personal Loan | 8% – 18% | 3-7 business days | W-2, pay stubs required | Stable income, credit 700+ |

| Payday/Title Loan | 200% – 400%+ APR | Same day | Minimal | Avoid entirely |

| HELOC | 8.5% – 10.5% | 2-6 weeks | Full underwriting | Homeowners, non-urgent costs |

| Medical Credit Card (e.g., CareCredit) | 0% promo / 26.99% after | Instant (in-provider) | Standard credit pull | Medical-specific costs only |

Where this gets tricky: What we tell readers in this situation is to watch the promo-period trap on medical credit cards. A $4,000 charge at 0% APR sounds ideal until the promotional window closes and the deferred interest kicks in at 26.99%. For caregivers already managing tight cash flow, that back-loaded cost can be worse than a fintech loan at 18% from the start.

What to Actually Look for in a Digital Lending Platform

Rate transparency separates the serious platforms from the predatory ones. For caregivers, the four non-negotiable features are: APR disclosure before a hard credit pull, no prepayment penalty, no origination fee above 3%, and a minimum loan amount under $2,000.

That last point matters more than it sounds. Most care-related emergencies don’t require $20,000, they require $1,500 for a bathroom modification or $2,500 for a month of respite care. Platforms that only offer loans starting at $5,000 are not built for the actual scale of caregiver borrowing needs. Upstart and Avant both offer minimums around $1,000-$2,000, which fits better. Larger minimum platforms like SoFi (minimum $5,000) are better suited to consolidation or larger home modification projects.

An underrated feature: some fintech platforms now offer payment pause or hardship deferment programs. Given that caregiver financial stress tends to spike unpredictably, a hospitalization, a medication change, a care recipient entering hospice, the ability to pause payments for 30-90 days without penalty is a legitimate factor in choosing between two otherwise comparable offers. Ask directly before signing; this is rarely advertised prominently.

Understanding how debt-to-income ratio calculations work on digital lending platforms is especially important here, because how a lender counts your care-related obligations against your income determines whether you qualify at all.

Applying for a Digital Loan When Your Primary Role Is Caregiving

Documentation is the practical bottleneck. Gather 3-6 months of bank statements showing consistent deposits, from employment, gig work, Social Security, or state caregiver stipends where applicable. Some states administer Medicaid-funded programs (such as Consumer Directed Care or CDPAP) that pay family members a direct stipend; these deposits can count as qualifying income on bank-statement underwriting models, even though they aren’t W-2 employment.

Rate shopping without damaging your credit is possible through pre-qualification tools. Most major fintech platforms run a soft credit inquiry for pre-qualification, meaning you can compare offers from four or five lenders without triggering a single hard pull. Only submit a full application, which triggers a hard inquiry, for the offer you intend to accept. This matters more for caregivers because borrowers with non-traditional income profiles already face higher effective rates and can’t afford unnecessary credit score damage on top of that.

What clients often miss: State caregiver stipends and Medicaid consumer-directed wages are taxable income in most states, which means they show up on bank statements and can be documented for income verification purposes. Many caregivers don’t realize this income counts, and don’t present it during the application.

Repayment Realities When Your Income Supports Two Households

Here’s the thing: the loan approval is not the hard part. Repayment is. A caregiver earning $3,800 per month after taxes, supporting both their own household and supplementing a care recipient’s costs, has roughly $600/month in care costs already baked in before a loan payment is added. On a $5,000 loan at 18% APR over 36 months, the monthly payment is approximately $181. That number is manageable in isolation, but layered onto an existing budget with no margin, it becomes the expense that gets missed first when a care crisis absorbs cash in a given month.

The safest repayment strategy for caregivers is to size the loan to the minimum needed to resolve the immediate need, not the maximum offered. Lenders will often approve more than is necessary, and the temptation to borrow extra as a buffer is understandable, but a larger loan compounds both the monthly payment pressure and the total interest cost over the loan term. Borrowing $3,000 instead of $5,000 at the same rate saves roughly $720 in interest over three years and reduces monthly payment obligations during a period when financial flexibility matters most.

Where This Recommendation Falls Short

The recommendation toward digital personal loans carries real tradeoffs that caregivers need to price in honestly before applying.

The most significant drawback: fintech APRs for borrowers with credit scores below 650 can reach 30-36%. A caregiver who accumulated medical debt on behalf of a care recipient, which is common and not a reflection of financial mismanagement, may have a credit score that puts them in the higher-rate tier. At 35% APR, a $4,000 loan over 36 months costs over $2,700 in interest. That’s not meaningfully better than some credit union alternatives, and it’s considerably worse than the 18% example in the Our Take section. The recommendation holds for borrowers above 620; below that, the math changes and the credit union route, despite slower timelines, becomes worth pursuing, even if it means waiting a few extra days or finding a co-signer.

The catch on alternative data underwriting is that it doesn’t work uniformly across all platforms. Not every fintech lender uses bank-statement underwriting; some still rely heavily on credit scores and W-2 income. A caregiver who assumes all digital lenders are flexible may apply to a platform that rejects them for the same reasons a bank would. Vetting which specific platforms use cash-flow models before applying is necessary, it’s not an automatic feature of being digital.

There’s also a risk specific to caregivers who are already near their DTI ceiling. Adding any loan payment to a budget supporting two households can crowd out emergency savings contributions. If a borrower’s post-loan budget leaves zero margin for unexpected care costs, which, by definition, is what caregiving budgets frequently face, then the loan solves today’s problem while removing the buffer needed for the next one. In that scenario, non-debt options (state caregiver stipends, nonprofit grants, tax credits from the IRS for dependent care) should be exhausted first, even partially, before borrowing. Not for everyone, but for caregivers already at financial capacity: the right answer may be a smaller loan paired with non-debt relief, rather than digital borrowing alone.

How We Sourced This

This article draws primarily from AARP’s 2024 research on financial supports for family caregivers and AARP’s caregiver financial impact data for verified statistics on out-of-pocket costs and borrowing behavior. APR ranges and funding timelines in the comparison table reflect publicly disclosed terms from LightStream, Upstart, SoFi, Avant, and LendingClub as of June-July 2024, cross-referenced against the Consumer Financial Protection Bureau’s personal loan guidance. State caregiver stipend programs (including CDPAP) were verified through respective state Medicaid program documentation. DTI thresholds and credit score ranges reflect underwriting standards disclosed in each platform’s public-facing eligibility documentation. All statistics were verified and current.

Frequently Asked Questions

Can I use a digital personal loan to pay for caregiving expenses?

Yes. Most personal loans from digital lenders are unsecured and unrestricted, you can apply proceeds toward home modifications, medical equipment, respite care, transportation, or any other care-related cost. No lender will ask you to itemize what the funds are for on a standard personal loan application.

Do fintech lenders count caregiver stipends or Medicaid wages as qualifying income?

Several do, provided the income appears consistently in your bank statements. Platforms using bank-statement or cash-flow underwriting, including Upstart and some LendingClub products, can treat regular direct deposits from state caregiver programs as verifiable income. W-2-dependent platforms will not count stipend income. Confirm the underwriting approach with any lender before applying.

What credit score do I need to qualify for a digital personal loan as a caregiver?

Most fintech personal loan platforms require a minimum credit score of 580-620. Approval at that floor typically comes with APRs in the 28-36% range. For rates below 20%, a score above 680 is generally needed. Caregivers whose credit scores dropped due to medical debt, not payment negligence, should consider a co-signer to access better terms.

How does caregiving affect my debt-to-income ratio for loan applications?

Caregiving affects DTI in two ways: it reduces income if you’ve cut work hours, and it increases obligations if you carry any existing debt taken on for care costs. Lenders calculate DTI based on monthly debt payments divided by gross monthly income, they don’t subtract care expenses that aren’t formal debt obligations. This means your real financial pressure may be worse than your DTI number suggests, even if you qualify.

Are there digital loans specifically designed for family caregivers?

As of mid-2024, no major lending platform markets a loan product specifically for family caregivers. The practical solution is a standard unsecured personal loan from a fintech platform that uses alternative income verification, sized appropriately for care-related needs. Some credit unions affiliated with healthcare employers or caregiver organizations offer specialized programs worth checking locally.

Can the person I care for be a co-signer on my loan?

Technically yes, if they have income and a qualifying credit score. In practice, care recipients are often elderly, disabled, or managing their own fixed-income constraints that make co-signing inadvisable. A healthier option is enlisting another family member who shares responsibility for the care recipient’s wellbeing, especially if that person has stronger credit. Understand that mismatched credit scores between co-borrowers affect the interest rate you’ll be offered, sometimes significantly.

What happens if I can’t make a loan payment during a care crisis?

Contact the lender immediately, before missing the payment, not after. Most fintech platforms offer hardship deferment or forbearance programs that allow 1-3 payment pauses without penalty, but these are discretionary and must be requested proactively. Missing a payment without communication risks a credit score drop of 60-100 points and potential late fees; requesting a pause before the due date typically triggers neither consequence.