Fact-checked by the CapitalLendingNews editorial team

The Verdict

Avoiding digital lending mistakes before you apply is worth the extra preparation time if you have a thin credit file or are applying for the first time. The single biggest threshold: if you have fewer than 5 years of credit history, pre-application errors cost you disproportionately more than they do seasoned borrowers. Skip the prep work and you risk automatic rejection, score damage, or a predatory lender.

The decision to apply for a digital loan feels fast by design, and that speed is where most first-time borrowers get into trouble. Digital lending mistakes rarely happen during the application itself. They happen in the ten minutes before, when a borrower opens three apps simultaneously, skips the rate check, or hands over bank-account access to an unverified lender. According to the Federal Reserve’s 2025 report on household economic well-being, roughly one-third of credit applicants in 2024 were denied or approved for less than they requested, a number that skews sharply toward first-time and thin-file borrowers.

That matters right now because the digital lending market has grown faster than borrower education around it. Fintech platforms, embedded lenders, and buy-now-pay-later apps have normalized speed, but they have also compressed the window where borrowers can catch their own errors. The mistakes are predictable. Most of them are preventable.

| Factor | Reasons to Prepare Before Applying | Reasons First-Timers Skip Preparation |

|---|---|---|

| Credit Report Accuracy | Errors can trigger automatic rejections in seconds with digital underwriting | Borrowers assume fintech platforms check fewer data points than banks |

| Hard Inquiry Impact | Clustering applications compounds score damage for thin-file borrowers | Speed of digital apps makes it tempting to apply to several at once |

| Lender Verification | Unregulated apps use fake approvals to harvest fees and personal data | Positive app store ratings feel like sufficient vetting |

| True Affordability | Origination fees and late charges add 3–8% to total loan cost beyond the stated rate | Instant approval amounts feel like a green light to borrow the maximum |

| Document Consistency | Mismatches in income data trigger automated fraud flags and delays | Digital platforms appear informal, so borrowers underestimate document precision needed |

| App Permissions | Broad data access consented to before download can enable third-party sharing or aggressive collections | Users click through permissions quickly to reach the loan offer |

Key Takeaways

- Pull your credit report from AnnualCreditReport.com and dispute any errors at least 30 days before applying.

- Use soft-pull prequalification tools on every platform before submitting a full application that triggers a hard inquiry.

- Limit formal applications to 1–2 platforms within a 14-day window so credit-scoring models treat them as rate shopping rather than separate inquiries.

- Verify any digital lender’s state license through the Consumer Financial Protection Bureau (CFPB) complaint database before sharing financial data.

- Calculate total loan cost including origination fees before accepting; a 5% origination fee on a $10,000 loan adds $500 upfront that the APR headline may not immediately convey.

- Review every app permission request before download; deny access to contacts, call logs, and location data unless the lender explains a clear underwriting purpose.

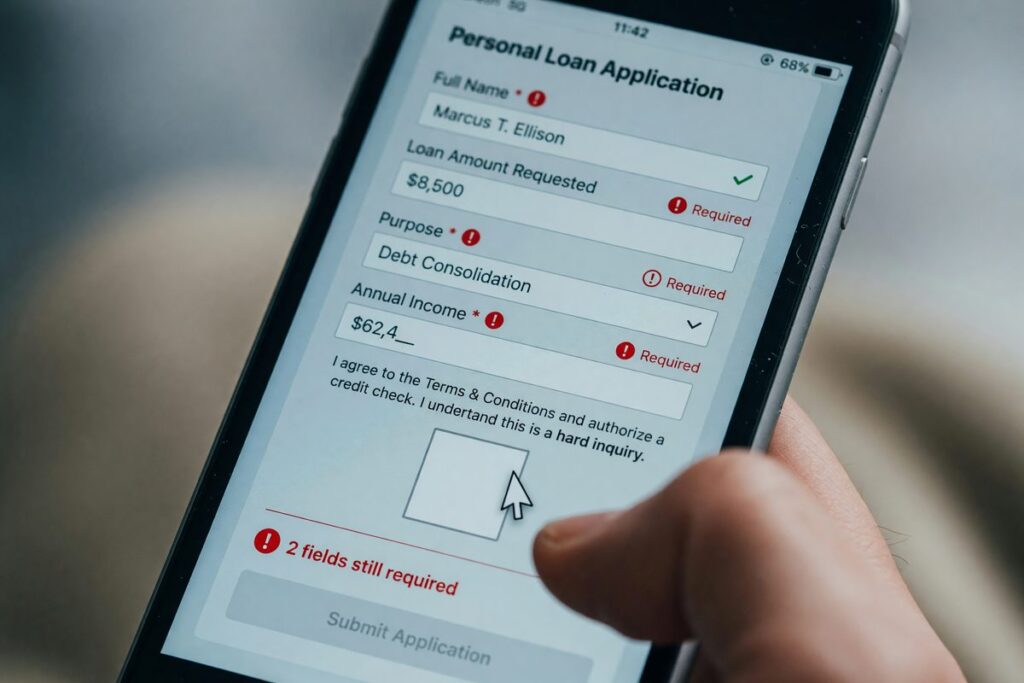

- Ensure that all income figures you enter match your bank transaction history exactly, since automated systems flag inconsistencies as fraud indicators.

Is Your Digital Credit Footprint Ready for Instant Underwriting?

Most digital lenders run an automated decision in under 60 seconds, and that decision leans heavily on whatever your credit file shows at that exact moment. A single outdated collection account or a name mismatch between your application and your credit report can trigger an automatic rejection before a human ever reviews it. For first-time borrowers, this is the highest-leverage place to focus before touching any application.

Traditional credit bureaus, Equifax, Experian, and TransUnion, still anchor most digital underwriting decisions, even on fintech platforms that advertise alternative data. Errors appear on roughly one in five consumer credit reports according to Federal Trade Commission research, and they do not correct themselves. Pull all three reports and look specifically for accounts that are not yours, balances already paid off but still showing open, and any public records that may have been misattributed. Dispute anything inaccurate in writing through the relevant bureau directly.

Alternative data adds another layer that most generic loan advice ignores entirely. Fintech platforms like Upstart, Petal, and Chime-affiliated lenders increasingly pull transaction history and payroll data to build a fuller picture of creditworthiness. Fintech lenders using payroll data can approve borrowers that traditional banks would reject, but only when that data is clean, current, and consistent. If your linked bank account shows irregular deposits that don’t match the income figure you typed in, the system flags it. The rejection is automated; the appeal is slow.

One genuine limitation worth naming: if your credit file is very thin, fewer than three open accounts, even a clean, error-free report may not give an automated system enough data to approve you at a competitive rate. Some fintech platforms will approve the loan but at an APR that costs more than a secured credit card would over the same period. Preparation reduces errors, but it cannot manufacture credit depth that does not yet exist.

Multiple Applications, One Week: The Inquiry Problem Digital Apps Make Worse

Three apps, three hard pulls, three points off your score each, and for a borrower with fewer than two years of credit history, that sequence can move you from an approval tier to a denial. Hard inquiries from digital lenders tend to post to credit bureaus faster than traditional bank inquiries, compressing the damage into a shorter window.

The standard rate-shopping exception under FICO and VantageScore models groups mortgage and auto loan inquiries within a 14-to-45-day window. Personal loan applications on digital platforms get the same treatment, but only if they happen within that window, and only if the borrower knows to use it. Most first-timers do not. They open one app Monday, get a rate they dislike, open another Wednesday, and a third Friday, treating each as a separate decision rather than a coordinated search.

The fix is straightforward. Use every platform’s prequalification or “check your rate” tool first. These use soft pulls, which do not affect your score at all. LendingClub, SoFi, and Prosper all offer soft-pull prequalification. Once you have narrowed your choices to two realistic options, submit formal applications on the same day. If you have non-traditional employment, understanding how debt-to-income ratio works on digital lending platforms will help you filter out lenders where you won’t qualify before the hard pull ever happens, which is exactly how thin-file borrowers should approach this market.

How to Verify a Digital Lender Before You Share Anything

Scam and unregulated lending apps represent a specific danger for first-time borrowers, and the risk is larger than most mainstream advice acknowledges. Over 40% of surveyed users in certain markets reported being targeted by fraud through digital lending apps, often involving fake approval screens designed to extract processing fees or harvest banking credentials before any loan is disbursed.

A polished app interface and a high star rating are not sufficient vetting. Fake apps cycle through app store listings quickly, sometimes cloning the branding of legitimate lenders like Marcus by Goldman Sachs or LightStream to appear credible. Google has taken enforcement actions against apps requesting excessive device permissions, contacts, call logs, or message access, that serve no underwriting purpose and create data-sharing risks extending well beyond the lender itself.

Before entering any personal or financial information, confirm that the lender holds a valid license in your state (searchable through your state’s financial regulatory agency or the CFPB’s database), that the lender’s website uses HTTPS and matches the name on the app store listing exactly, and that no active enforcement actions or warnings exist from the Consumer Financial Protection Bureau or the Federal Trade Commission. The CFPB’s public complaint database is searchable and free. A lender with dozens of unresolved complaints about hidden fees or aggressive collections is telling you something.

For borrowers in markets with tighter regulatory environments, the picture shifted noticeably after privacy rule tightening in 2025 and 2026. Post-regulation data from comparable markets showed approval rates dropping by 16 to 18 percentage points for younger and first-time applicants, even when default rates remained flat, meaning the restrictions cut legitimate borrowers, not just risky ones. That’s a structural disadvantage for first-timers that thorough pre-application research can partially offset.

Who Should and Who Should Not

Good candidates

First-time borrowers who spend time on preparation tend to get meaningfully better outcomes from digital lenders than those who rush in cold.

- A borrower with a credit score between 620 and 680 who has pulled their report, disputed one error, and used soft-pull prequalification may move from a 24% APR offer to a 17% offer through preparation alone.

- A gig worker or freelancer who has 12+ months of consistent bank transaction history and understands how digital lending for gig workers with income gaps works, alternative data underwriting favors consistency, not W-2s.

- A first-time borrower who needs a small loan ($1,000–$5,000), has verified the lender’s license, and is borrowing for a defined, short-term purpose with a clear repayment timeline.

- Someone who has calculated the total cost of the loan including origination fees and still finds the all-in APR lower than comparable credit card financing.

Who should skip it

Some borrowers are better served waiting until their financial picture strengthens, or using a different product entirely.

- A borrower who plans to apply to five or more platforms in a single week without using soft-pull prequalification first, the inquiry damage will likely cost more than the rate difference between lenders.

- Someone who found the lender through a social media ad and has not verified its licensing or CFPB record; the risk of encountering a fraudulent app is highest through unverified referral channels.

- A borrower whose debt-to-income ratio is already above 40%, digital lenders typically apply the same DTI constraints as banks, and a rejection now creates an inquiry without the benefit of funds.

- Anyone borrowing the maximum pre-approved amount without running the repayment numbers against their actual monthly budget, including any variable fees the platform may charge. Understanding how loan term length controls your total interest cost is essential before accepting any offer.

Frequently Asked Questions

What are the most common digital lending mistakes first-time borrowers make?

Applying to multiple platforms simultaneously without using soft-pull prequalification is the most damaging single mistake, particularly for thin-file borrowers. Close behind it: skipping lender verification, entering income figures that don’t match bank transaction data, and accepting the maximum approved amount without calculating total repayment cost including fees.

Do multiple digital loan applications hurt your credit score?

Each formal application that triggers a hard inquiry typically lowers your score by a few points temporarily. For borrowers with limited credit history, several applications within days of each other can compound that effect enough to push you into a lower approval tier. Rate-shopping within a 14-day window limits the damage, since scoring models may count those inquiries as one.

How do I tell if a digital lending app is legitimate?

Search the lender’s name in the CFPB’s public complaint database and confirm they hold a valid license in your state. Legitimate lenders do not require you to pay an upfront fee before disbursing a loan, and they will not request access to your contact list or call logs during the application process.

Can a fintech lender approve me without a traditional credit score?

Some fintech lenders use alternative data, bank transaction history, payroll records, or subscription payment patterns, to underwrite borrowers with thin or no credit files. Even these platforms typically pull a credit report as part of identity verification, and inconsistencies between your application data and the data they access will delay or deny approval automatically.

What does a 5% origination fee actually cost me on a digital loan?

On a $10,000 loan, a 5% origination fee equals $500 deducted upfront, so you receive $9,500 but repay the full $10,000 principal. Over a 3-year term at a 15% APR, that changes your effective cost meaningfully, which is why comparing APR across lenders, not just the stated interest rate, is the only accurate way to evaluate competing offers.

Should I avoid giving a lending app access to my bank account?

Read-only access for income verification through services like Plaid or Finicity is standard and generally safe with licensed lenders. What to refuse: any permission request for your contact list, call logs, location data outside of fraud prevention, or the ability to initiate withdrawals beyond your agreed repayment amount. Those permissions have no legitimate underwriting purpose and create real risk of data misuse.

Sources

- Federal Reserve, Report on the Economic Well-Being of U.S. Households in 2024: Banking and Credit

- Consumer Financial Protection Bureau, Consumer Complaint Database

- Federal Trade Commission, Consumers and Credit Reports

- AnnualCreditReport.com, Free Credit Report Access (Equifax, Experian, TransUnion)

- myFICO, Hard vs. Soft Credit Checks: What’s the Difference?

- Consumer Financial Protection Bureau, What Is a Debt-to-Income Ratio?

- Federal Trade Commission, Truth in Lending Act (Regulation Z) Overview

- Consumer Financial Protection Bureau, Credit Reports and Scores: Key Terms

- FDIC, Bank and Lender Regulatory Resources

- Experian, What Is Alternative Credit Data?

- Plaid, End-User Privacy Policy and Data Access Practices

- NerdWallet, Personal Loan Origination Fees Explained

- Consumer Financial Protection Bureau, CFPB Actions Against Illegal Digital Lending Practices