Fact-checked by the CapitalLendingNews editorial team

The Verdict

Automated fintech debt repayment is worth it if you have stable monthly income, at least $5,000 in unsecured debt, and a history of missed or late payments. It is not worth it if your income is irregular, your debt involves creditor negotiations, or app fees eat more than what you save in interest, which happens faster than most borrowers expect.

The single factor that swings this decision is income stability. Automated fintech debt repayment works by pulling fixed amounts from your linked bank accounts on a schedule, and that schedule has no tolerance for a month where your paycheck came in late or your freelance client stiffed you. According to the CFPB’s 2024 rule on digital payment app oversight, popular apps collectively process over 13 billion consumer payment transactions annually, which speaks to how mainstream these tools have become. Volume alone does not mean every setup suits every borrower.

This matters right now because the fintech debt category has matured enough that you can delegate nearly your entire repayment strategy to an algorithm. The question is whether that delegation actually helps your balance sheet or just your peace of mind.

| Factor | Reasons to Use Automated Repayment | Reasons Not to Use Automated Repayment |

|---|---|---|

| Late Fees | Eliminates missed payments; average late fee on credit cards runs $30–$41 per incident | Autopay only prevents your own forgetfulness; does not negotiate creditor terms |

| Interest Savings | Round-up and extra-payment features can shave months off a payoff timeline | Savings projections assume balances stay static; most borrowers keep spending |

| Consistency | Removes decision fatigue; payments happen regardless of impulse spending | False sense of control; automation does not prevent new debt accumulation |

| Cost | Some apps claim users save 10x the subscription fee in reduced interest charges | Subscription fees of $6–$20/month erode savings on small balances under $3,000 |

| Data Security | Reputable apps use bank-grade encryption and read-only account access via aggregators | Third-party data aggregators like Plaid create exposure points; app shutdowns strand linked accounts |

| Flexibility | Most apps let you pause or adjust allocations without penalty | Variable income borrowers risk overdraft fees when automation pulls on a low-balance day |

| Creditor Relations | Consistent payment history improves credit score reporting over time | Cannot negotiate reduced rates or hardship plans the way nonprofit DMPs can |

| Financial Skills | Frees mental bandwidth for higher-level money decisions | Full delegation erodes personal awareness of interest rates, due dates, and balances |

Key Takeaways

- Your monthly take-home pay is consistent within a 10% variance from month to month

- Your total unsecured debt balance is at least $5,000, making interest savings meaningful relative to app fees

- You have missed at least one payment in the past 12 months due to forgetfulness, not cash flow

- Your debts are held at institutions compatible with the app’s bank connectivity (confirm before signing up)

- You have a $500+ buffer in your checking account at all times to absorb automated pulls without overdrafting

- You are comfortable granting read or write access to a third-party aggregator like Plaid or Finicity for account linking

- Your debt does not require active creditor negotiation, no collections accounts, no settlements in progress

What Does “Automated Fintech Debt Repayment” Actually Mean in 2026?

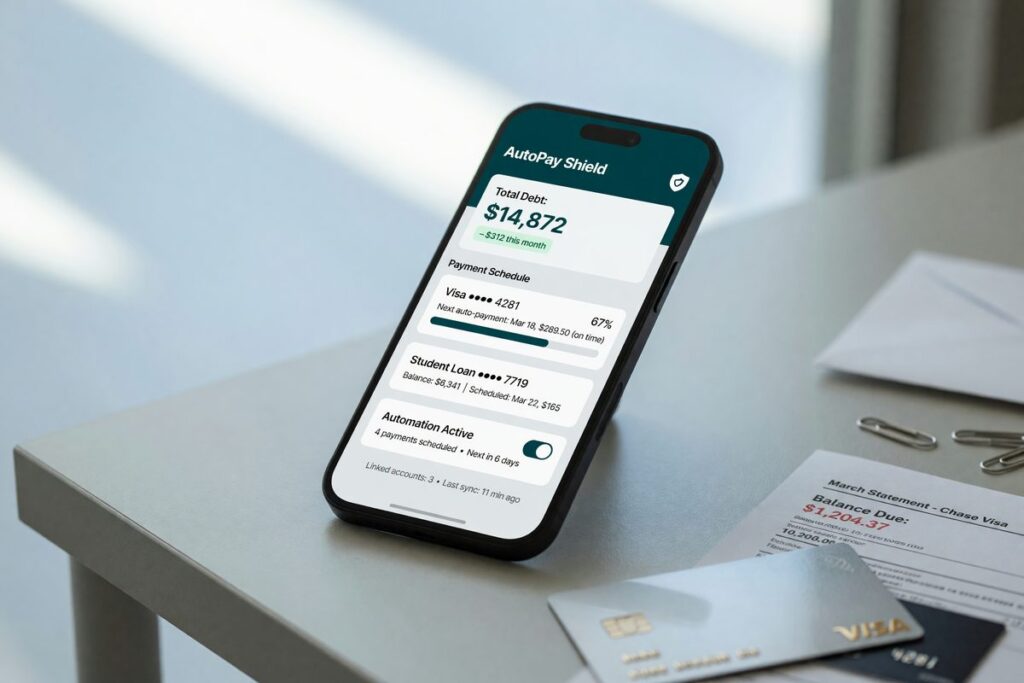

Not all automation is equal. Simple autopay, scheduling a fixed minimum payment through your bank, is very different from an AI-driven debt repayment app that reads your cash flow, identifies surplus, and allocates extra payments toward your highest-interest balance each week.

Apps like Ditch and tools built on Method Financial‘s infrastructure sit in the second, more sophisticated category. They link to your checking account via data aggregators such as Plaid or Finicity, read your incoming deposits and spending patterns, and then execute payments beyond minimums when your balance supports it. Some layer in round-up features: every debit card purchase gets rounded to the nearest dollar, and the difference flows toward debt. The result is a dynamic repayment engine rather than a static calendar reminder.

That sophistication is the value proposition and the risk simultaneously. The smarter the algorithm, the more account access it requires, and the more that can go wrong if the company changes its terms, gets acquired, or shuts down. We will cover that in detail below.

There is also a behavioral limitation worth naming early: automation handles the mechanics of payment, but it does nothing to slow new debt accumulation. Borrowers who continue spending at the same rate while running an automated repayment app often find their net balance barely moves. The tool removes one failure mode while leaving the more consequential one untouched.

Income Stability Is the Factor That Actually Decides This

For salaried borrowers, automated repayment is nearly always an upgrade. For gig workers, freelancers, and seasonal earners, it can create new problems while trying to solve old ones.

The core issue is that debt repayment apps are built around predictability. Most schedule pulls based on projected balances after reviewing 30–90 days of deposit history. If your income drops sharply one month, a contract ends, a client is slow to pay, the app may still attempt a pull your account cannot absorb. That triggers an overdraft fee from your bank, often $25–$35, which negates any interest savings from the extra payment. Worse, some apps do not catch this scenario until after the transaction fails, meaning you get hit twice: once by the bank, once by the app’s failed-payment process.

If you earn irregular income, a hybrid approach combining fintech tools with a manual buffer strategy is far more practical than full automation. Set the app to handle only minimums automatically, and make extra payments manually when surplus is confirmed. You get consistency without the overdraft exposure.

The default-rate data on automatic repayment is instructive here. A 2025 CFPB report on Buy Now, Pay Later lending found that BNPL borrowers defaulted on just 2 percent of their BNPL loans between 2019 and 2022, compared to 10 percent of the credit cards they held, a gap the CFPB attributes in part to automatic repayment requirements built into BNPL products. The takeaway is real: structured automatic payment does reduce default risk. But BNPL products deduct fixed, predictable amounts tied to specific purchases, which is a much simpler pull than a dynamic algorithm deciding how much surplus to sweep each week. The behavioral benefit is genuine; the operational risk is different in kind.

Do the Fees Actually Get Eaten Up by the Savings?

Sometimes yes, sometimes no, and the balance threshold where it tips matters more than most app marketing admits.

Ditch states that most users save 10x their subscription fee in reduced interest charges. At a typical fee of $10/month, that implies $100/month in interest savings, or $1,200/year. On a $10,000 balance at an 18% APR, paying an extra $100/month toward principal reduces total interest paid by roughly $1,800 over the life of the loan and cuts the payoff period by about 14 months. The math holds, but only if the automation actually generates that extra $100 in monthly payments and your balance is large enough to produce that kind of interest differential.

Run the scenario in reverse: a borrower with a $2,500 balance at 18% APR paying an extra $30/month saves about $190 in interest total. A $10/month app fee over the 8-month accelerated payoff costs $80. Net benefit: $110. That is real money, but it is not 10x the fee, it is barely 1x. At balances under $3,000, the math deserves scrutiny before you sign up.

Compare this against nonprofit options. A Debt Management Plan (DMP) through an NFCC-member agency typically costs $25–$35/month but includes negotiated rate reductions that can drop a 24% credit card rate to 6–10%. No fintech app can replicate that, because the rate reduction requires a human negotiating directly with the creditor.

Security, Privacy, and What Happens If the App Shuts Down

This is the angle most debt repayment app reviews skip entirely, and it deserves direct treatment.

Every app in this category requires you to grant third-party access to your bank account data. That access flows through aggregators like Plaid, which act as intermediaries between the app and your financial institution. The connection is typically read-only for monitoring and write-access only for payment execution. Encryption standards at reputable aggregators are solid. But the chain of custody for your data is longer than most borrowers realize: your bank, the aggregator, the app itself, and potentially the app’s cloud hosting provider all touch your account credentials or tokenized equivalents.

The bigger risk that no competitor article currently addresses: what happens to your automated payment setup if the fintech company fails or gets acquired? In 2026, fintech consolidation is ongoing. When an app is acquired, its data-sharing agreements, fee structures, and even the algorithms driving your payment allocations can change overnight. Your linked accounts do not automatically disconnect. If you are not monitoring the app actively, you may continue to have automated pulls from a product you no longer recognize or trust.

The CFPB advises that consumers should understand how automatic payments work and monitor accounts closely, a reminder that automation requires more active oversight than it appears to, not less. Set a calendar reminder to review your linked apps quarterly. Know how to revoke access at the bank level, not just through the app itself.

For a fuller picture of how your financial data persists well beyond a single product, read about what happens to your data after a digital loan closes. The same dynamics apply here.

Who Should and Who Should Not

Good candidates

Automated fintech debt repayment delivers real value for borrowers whose main problem is behavioral, not structural.

- Salaried employees with predictable biweekly or monthly deposits and at least $5,000 in credit card or personal loan debt, the automation works as designed and the interest savings are meaningful

- Borrowers who have missed payments due to forgetfulness rather than genuine cash shortfall; automation removes that failure mode completely

- Anyone managing 3+ separate debt accounts who wants a single dashboard and coordinated payment strategy without spreadsheet management

- People who know they have a surplus each month but consistently spend it rather than applying it to debt; round-up and automated sweep features close that gap before the money can be redirected

Who should skip it

For these borrowers, the tool creates friction rather than removing it.

- Freelancers and gig workers with income that swings more than 20% month to month; overdraft risk is too high, and the app’s optimization will misread your capacity regularly

- Anyone with debts in active collections or in creditor settlement negotiations, the CFPB specifically warns against automated or third-party solutions that cannot negotiate directly with creditors, and automated payments can actually complicate settlement leverage

- Borrowers with balances under $2,000; the fee structure will likely exceed the interest savings over a short payoff timeline

- Anyone not comfortable with third-party bank account access or unwilling to monitor linked accounts regularly; the risk of undetected permission drift or unauthorized pulls is real if you disengage entirely

One additional caution for anyone considering these apps: the FTC’s debt relief guidance is clear that no automated product can substitute for direct creditor negotiation when accounts have already gone delinquent. If you are behind by 60 days or more, a fintech repayment app is the wrong starting point.

Frequently Asked Questions

Is it safe to give a fintech app access to my bank account for debt repayment?

For reputable apps using regulated aggregators like Plaid or Finicity, the technical risk is low but not zero. The more important safeguard is behavioral: review your linked accounts quarterly, know how to revoke access at the bank level, and check the app’s privacy policy for third-party data-sharing clauses before you connect anything.

What happens to my automated payments if the debt repayment app shuts down or gets bought?

Your automated pulls may continue under new ownership unless you manually revoke access. This is one of the most overlooked risks in the category. If you hear your app is being acquired, log in immediately, download your data, and disconnect your bank accounts through both the app and your bank’s linked-account settings. Do not wait for the transition to complete.

Can a fintech debt app lower my interest rate the way a debt management plan can?

No. Fintech apps cannot negotiate reduced interest rates with creditors. Only nonprofit Debt Management Plans through NFCC-member agencies have that relationship with major card issuers, and it regularly produces rate reductions from 20%+ down to 6–10%. If rate negotiation is your primary need, a DMP will outperform any automated app.

Will automating my debt payments improve my credit score?

Consistent on-time payments are the single largest factor in your FICO score, so yes, automation typically improves credit scores for borrowers who previously missed due dates. The impact depends on how your app routes payments: it should send them directly to the lender, not hold funds internally, to ensure timely reporting to Equifax, Experian, and TransUnion.

Are there free alternatives to paid debt repayment apps?

Several free alternatives exist. Your bank’s own autopay feature handles minimum or fixed-amount payments at no cost. Budgeting tools like YNAB or even a spreadsheet with manual biweekly transfers can replicate the debt avalanche or snowball strategies without subscription fees. For most borrowers with balances under $4,000, a free manual approach will net more savings than a paid automation app.

Sources

- Consumer Financial Protection Bureau, CFPB Finalizes Rule on Federal Oversight of Digital Payment Apps (2024)

- Consumer Financial Protection Bureau, Buy Now, Pay Later Report 2025

- Consumer Financial Protection Bureau, How Do Automatic Payments From a Bank Account Work?

- Consumer Financial Protection Bureau, What Should I Do If I Can’t Pay My Credit Card Bills?

- Federal Trade Commission, Debt Relief Services and the Telemarketing Sales Rule

- National Foundation for Credit Counseling, How Debt Management Plans Work