Fact-checked by the CapitalLendingNews editorial team

Quick Answer

Lenders price loans primarily on credit scores, debt-to-income ratio, and payment history, not savings balances. FICO Scores assign zero weight to cash reserves, so a borrower with $75,000 in savings but a 640 credit score can still be quoted 2–5 percentage points above prime on an unsecured personal loan compared to someone with $5,000 saved and a 760 score.

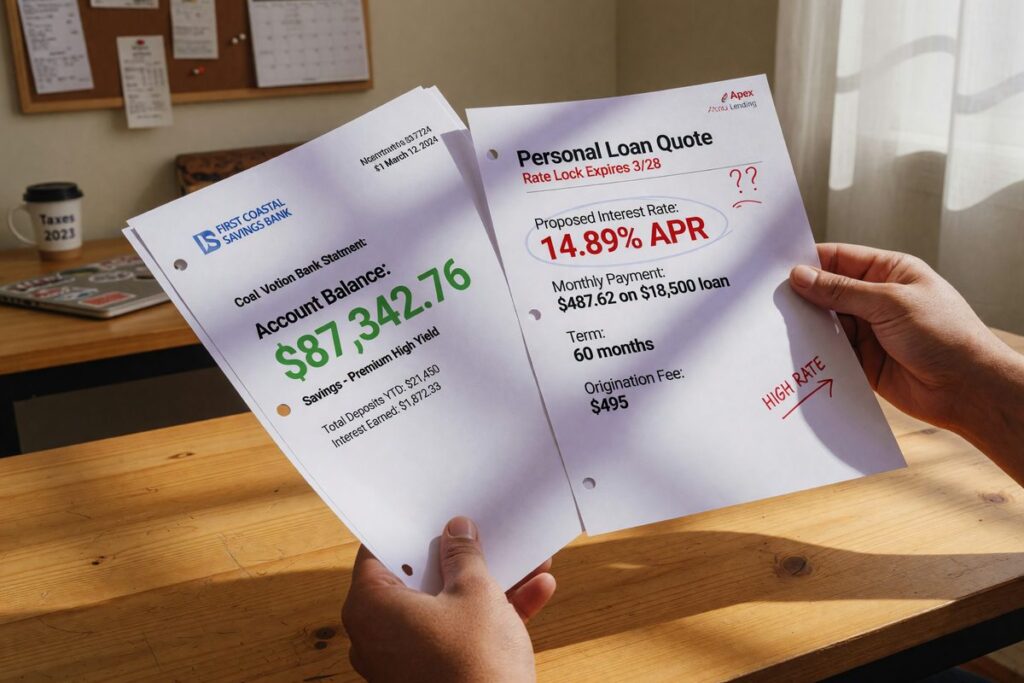

The high savings, high interest rate paradox catches borrowers off guard every day. A saver with $80,000 in a high-yield account applies for a $25,000 personal loan and gets quoted 14.9%, while a colleague with minimal reserves but a clean credit history gets 9.5%. The gap feels wrong, but it follows a precise logic. FICO confirms explicitly that its scoring models do not consider the amount of cash you hold, meaning your bank balance carries no direct weight in the formula that drives most lending decisions.

That gap has real costs, hundreds or thousands of dollars over a loan’s life. This guide explains why automated underwriting treats savings the way it does, which borrower profiles are most exposed, and what targeted steps actually move the rate quote in your favor.

Key Takeaways

- FICO Scores assign zero weight to savings or cash reserves; the “amounts owed” category measures utilization and debt levels, not account balances (FICO).

- Borrowers with credit scores in the 620–680 range are routinely quoted 2–5 percentage points above prime on personal and auto loans, regardless of savings held.

- Banks fund unsecured loans while paying depositors roughly 4–5% on high-yield savings accounts (June 2026 averages), then charge 8–12%+ on the same capital, a spread that rewards credit risk pricing, not asset holding.

- A joint interagency statement from the Federal Reserve, CFPB, FDIC, NCUA, and OCC acknowledges that bank account cash flow and savings can improve creditworthiness assessments, but only when lenders opt into alternative data models.

- The CFPB notes that while credit score is an important factor, lenders also weigh savings, total assets, and income, but in practice, these secondary factors rarely override a below-average credit score for rate-setting purposes (CFPB).

In This Guide

- The Counterintuitive Reality: High Savings, High Borrowing Costs

- How Lenders Actually Price Risk

- Why Credit Scores Outweigh Savings in Every Rate Quote

- Common Scenarios Where Strong Savers Still Face Premium Rates

- What Lenders Gain by Quoting Higher Rates to Savers

- Practical Steps to Improve Your Rate Even With High Savings

The Counterintuitive Reality: High Savings, High Borrowing Costs

Most borrowers assume liquidity signals safety. More cash on hand means you can cover payments if income drops, so the rate should fall. Lenders think in a different frame entirely.

Consider two applicants, each requesting a $30,000 personal loan. The first holds $90,000 across savings and brokerage accounts but carries a 648 credit score, opened three new accounts in the past year, and has a debt-to-income ratio of 38%. The second has $4,000 in checking, a 755 credit score, a clean payment history going back seven years, and a DTI of 18%. Almost every major lender will quote the first borrower a meaningfully higher rate, often by 4 percentage points or more, despite the obvious difference in liquid assets.

This outcome is not accidental. It is the direct result of how automated underwriting systems are built. They score the probability that a borrower will miss payments, and that probability is calculated almost entirely from credit behavior, not from balance sheet strength. The high savings, high interest rate outcome is, from a lender’s algorithmic perspective, entirely rational.

Fannie Mae’s Desktop Underwriter (DU) and Freddie Mac’s Loan Product Advisor (LPA), the two dominant automated underwriting engines for conforming mortgages, do use asset reserves as a compensating factor, but only after credit score and DTI thresholds are met. For personal loans and auto loans, most lenders use proprietary scorecards where reserves play an even smaller role or none at all.

How Lenders Actually Price Risk

Three factors dominate rate pricing at nearly every traditional lender: credit score, debt-to-income ratio, and income stability. Savings enters the equation late, and often only as a tiebreaker at the margins.

The Role of Automated Underwriting

For conforming mortgages, Fannie Mae’s Desktop Underwriter and Freddie Mac’s Loan Product Advisor run thousands of data points, but the output still pivots on credit score bands. Reserves above a certain threshold, typically two to six months of housing payments, can unlock marginal pricing benefits, but a score below 680 will override any reserve cushion when it comes to the rate tier assigned. For unsecured personal loans and auto lending, proprietary bank scorecards are even more rigid. Most assign savings balance a weight close to zero in rate-setting algorithms, though they may use it to approve borderline applications.

Debt-to-Income Ratio and Income Type

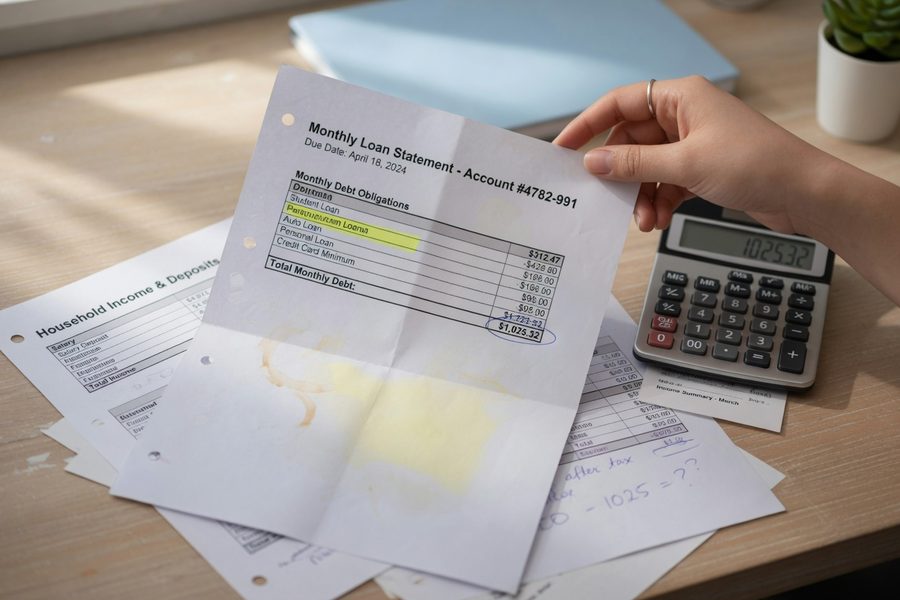

A high DTI penalizes borrowers directly in rate pricing, not just approval decisions. Lenders calculate DTI using gross monthly income divided by recurring monthly debt payments. A borrower with $120,000 saved but $3,200 in monthly debt obligations against $6,500 gross income sits at roughly 49% DTI, a number that triggers higher rates or outright declines at most banks, regardless of the savings figure. Income stability matters too. The CFPB notes that lenders weigh total assets and savings alongside credit scores, but in practice that weighing skews heavily toward score and income documentation, especially for self-employed applicants. That dynamic is covered in more detail in this analysis of self-employed mortgage rates when carry-forward losses affect qualification.

Why Credit Scores Outweigh Savings in Every Rate Quote

FICO is direct on this point: its scoring models simply do not consider how much cash you have. The “amounts owed” category, which accounts for roughly 30% of a FICO Score, measures credit utilization, number of accounts with balances, and installment loan balances relative to original amounts. It does not measure bank balances or investment holdings.

What FICO and VantageScore Actually Measure

Both FICO and VantageScore models are built on data reported to the three major credit bureaus: Equifax, Experian, and TransUnion. Savings accounts, money market accounts, and brokerage balances are not reported to any of those bureaus. They exist outside the data universe these models draw from. FICO states explicitly that “the amount of money you save doesn’t affect your FICO Scores.” That is not a technicality, it reflects a structural decision about what predicts payment behavior.

Payment history drives roughly 35% of a FICO Score. A single 30-day late payment from two years ago can cost 60–80 points, easily pushing a borrower from the 720 tier into the 640 tier. That shift can mean a rate difference of 3 to 5 percentage points on a personal loan, an outcome no savings balance can offset once the automated quote is generated. Understanding the full math behind those pricing bands is worth reviewing; this breakdown of interest rate tiers by credit score band shows exactly what each 20-point jump saves over a loan’s life.

Payment history accounts for approximately 35% of a FICO Score, while savings balances account for 0%. A single missed payment can move a borrower into a rate tier that costs thousands more over a loan’s term, no savings balance corrects that algorithmically.

The Alternative Data Exception

A joint interagency statement issued by the Federal Reserve, CFPB, FDIC, NCUA, and OCC confirmed that alternative data, including bank account cash flow and savings patterns, can be used in credit underwriting to potentially improve assessments of creditworthiness. Some fintech lenders have adopted this approach. The caveat is significant: most traditional banks and credit unions have not integrated these models at the rate-setting level. If your lender relies on a standard FICO pull and a proprietary scorecard, your savings data likely never enters the rate calculation at all. Newer platforms using alternative signals in their underwriting are the exception, not the rule in 2026.

Common Scenarios Where Strong Savers Still Face Premium Rates

Four specific borrower profiles show up repeatedly in above-average rate quotes despite substantial savings.

Thin credit files are common among high earners who pay cash for most purchases or have avoided debt for years. A 45-year-old with $150,000 saved but only two open trade lines will generate a limited credit score, sometimes below 680, because there is not enough scoring history to establish a higher tier. Recent credit inquiries compound the problem, five hard pulls in twelve months signal credit-seeking behavior that scoring models penalize regardless of what the savings account shows. High revolving utilization is another frequent mismatch: some savers keep large card balances for reward points or convenience while holding cash separately. A 72% utilization rate on a $20,000 credit line reads as financial stress to an algorithm even when $60,000 sits in a HYSA. Finally, irregular or self-employed income paired with strong savings creates documentation friction. Lenders may accept the savings as reserves but still price the loan higher due to income verification complexity, a pattern examined in detail in this guide to how debt-to-income ratio affects digital lending decisions.

| Borrower Profile | Savings Balance | Credit Score | Typical Rate Premium vs. Prime |

|---|---|---|---|

| Thin file, high saver | $100,000+ | 640–660 | +4 to +5 percentage points |

| High utilization, cash-rich | $50,000–$80,000 | 620–650 | +3 to +5 percentage points |

| Self-employed, strong reserves | $75,000–$150,000 | 660–690 | +2 to +4 percentage points |

| Recent inquiries, solid savings | $40,000–$70,000 | 670–700 | +1.5 to +3 percentage points |

| Strong credit, moderate saver | $5,000–$20,000 | 740–780 | 0 (at or below prime) |

What Lenders Gain by Quoting Higher Rates to Savers

Rate pricing is not arbitrary, it reflects a structural incentive built into how banks fund their lending operations.

, competitive high-yield savings accounts pay depositors roughly 4–5% APY. Banks take those deposits and lend them out on unsecured personal loans at 8–12% or higher, capturing a spread of 3 to 8 percentage points. That spread is how lending profitability works. A bank has no algorithmic reason to lower your rate because you happen to hold deposits with them or a competitor, your savings reduce the bank’s funding need in aggregate, but they do not reduce the bank’s assessed probability that you personally will default. Risk segmentation under frameworks like Basel III requires banks to hold regulatory capital against loan portfolios based on default probability, not on borrower wealth. A borrower with a 640 score costs the bank more in regulatory capital terms than a borrower with a 760 score, regardless of how much cash either holds.

Large recent deposits can sometimes trigger additional scrutiny rather than rate relief. Mortgage underwriters and some personal loan lenders require source-of-funds verification for substantial deposits made within 60–90 days of application. A $50,000 transfer showing up just before application may require documentation of origin, adding friction without improving your rate.

Practical Steps to Improve Your Rate Even With High Savings

The most direct path to a lower rate is fixing the factors lenders actually score, not highlighting the ones they ignore.

Credit Optimization Before You Apply

Paying down revolving balances to below 30% utilization before applying can move a score 20–50 points in 30–60 days. That single action can shift a borrower from one rate tier to the next. Disputing errors on Equifax, Experian, or TransUnion reports is worth doing before any application, inaccuracies affecting score are more common than most borrowers expect. Avoid opening new accounts or triggering hard inquiries in the three months before applying. The practical guidance in this overview of common digital lending mistakes first-time borrowers make covers several of these pre-application missteps in detail.

Shopping Lenders and Disclosing Assets Strategically

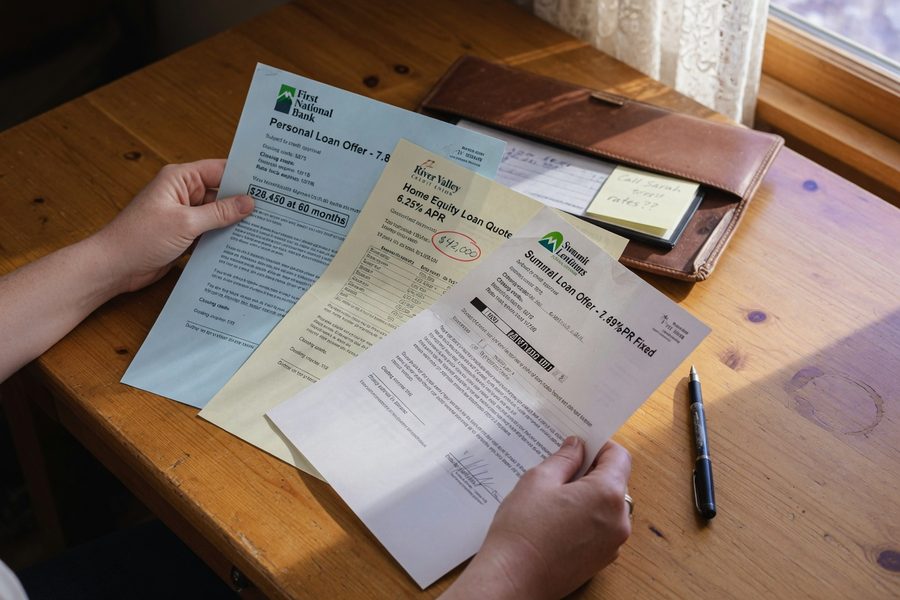

Rate shopping across at least three to five lenders within a 14–45 day window is scored as a single inquiry by FICO’s models, so there is no credit cost to comparing offers. Some lenders, particularly credit unions and certain online lenders that use alternative underwriting, will factor verified savings and cash flow into their pricing. Asking explicitly whether a lender uses asset-based underwriting or alternative data takes one phone call. Adding a co-borrower with a stronger credit profile is one of the most reliable ways to access a lower tier; the mechanics of how that interaction affects pricing are laid out in this guide to co-borrower credit score mismatches on joint loans.

One honest caveat: if your score sits below 640 and your DTI exceeds 40%, even perfect credit optimization may not bridge the full rate gap. In that scenario, waiting 6–12 months while building credit history and reducing debt balances will produce a more durable outcome than any application-timing tactic.

If you hold substantial savings, ask lenders whether they accept asset depletion income, a method where verified assets are divided over a loan term to create an imputed monthly income figure. This approach, more common in mortgage lending, can improve your income profile with some lenders even if your W-2 income is modest or irregular.

Related reading: debt management plan.

Frequently Asked Questions

Does having a lot of savings in the bank lower your interest rate?

Not automatically. Standard FICO and VantageScore models assign no weight to savings balances, so holding large cash reserves does not directly lower your quoted rate at most lenders. Some lenders that use alternative data or manual underwriting may factor in verified assets, but this is the exception rather than the standard practice at traditional banks and credit unions.

Why do lenders care more about credit scores than savings?

Credit scores are built from data that directly predicts payment behavior, on-time history, utilization patterns, account age, and past delinquencies. A borrower’s past behavior with debt is a stronger statistical predictor of future defaults than their current cash position. Savings do not appear in credit bureau files, so they cannot influence a score-driven rate decision.

Can a high savings balance help you get approved for a loan even with a low credit score?

Yes, in some cases. Verified savings and investment assets can serve as compensating factors in mortgage underwriting, particularly through Fannie Mae’s Desktop Underwriter or with lenders using manual review. For personal loans and auto loans, the effect is less consistent, some lenders use savings as a tiebreaker for borderline applications, but approval does not guarantee a better rate.

Does keeping savings at the same bank where you borrow improve your rate?

Rarely in any meaningful way. Relationship pricing, rate discounts for existing deposit customers, exists at some institutions, typically offering 0.25 to 0.50 percentage point reductions. That benefit is modest compared to the rate gap caused by a below-average credit score, and it should not be the primary reason to concentrate deposits at a single institution.

What is the fastest way to lower a loan rate when you have high savings but a mediocre score?

Reducing revolving credit utilization below 30% is usually the fastest lever, it can improve a FICO Score within 30 days of a balance update. After that, shopping multiple lenders within a short window costs nothing in credit terms and often reveals a spread of 2–4 percentage points between the highest and lowest quotes for the same borrower profile.

Do fintech lenders treat savings differently than traditional banks?

Some do. Certain fintech lenders have adopted bank account cash flow and savings pattern analysis as part of their underwriting, consistent with the framework outlined in the interagency guidance on alternative data. Borrowers with strong savings histories but limited credit files may find meaningfully better pricing at these platforms than at a traditional bank running a pure FICO-based model.

Can a large recent deposit hurt my loan application?

It can create friction. Mortgage lenders and some personal loan platforms require source-of-funds verification for large deposits made within 60–90 days of application. A substantial transfer that cannot be documented, a gift, business distribution, or asset sale, may delay approval or trigger additional scrutiny, even though the deposit itself improves your apparent cash position.

Sources

- FICO, FAQs About FICO Scores

- Consumer Financial Protection Bureau, Does My Credit Score Affect My Mortgage Rate?

- National Credit Union Administration, Interagency Statement on the Use of Alternative Data in Credit Underwriting

- Board of Governors of the Federal Reserve System, Selected Interest Rates (H.15 Release)

- myFICO, What’s in Your Credit Score?