Fact-checked by the CapitalLendingNews editorial team

The Verdict

Public employee loan rates are worth pursuing if you can document full-time employment with a qualifying government or nonprofit employer. Teachers and public workers who verify membership and stack autopay discounts can realistically access rates 0.5–1.25% below national averages on personal and auto loans. Skip the search if you work part-time or hold a contract role, since most programs require continuous full-time status to qualify.

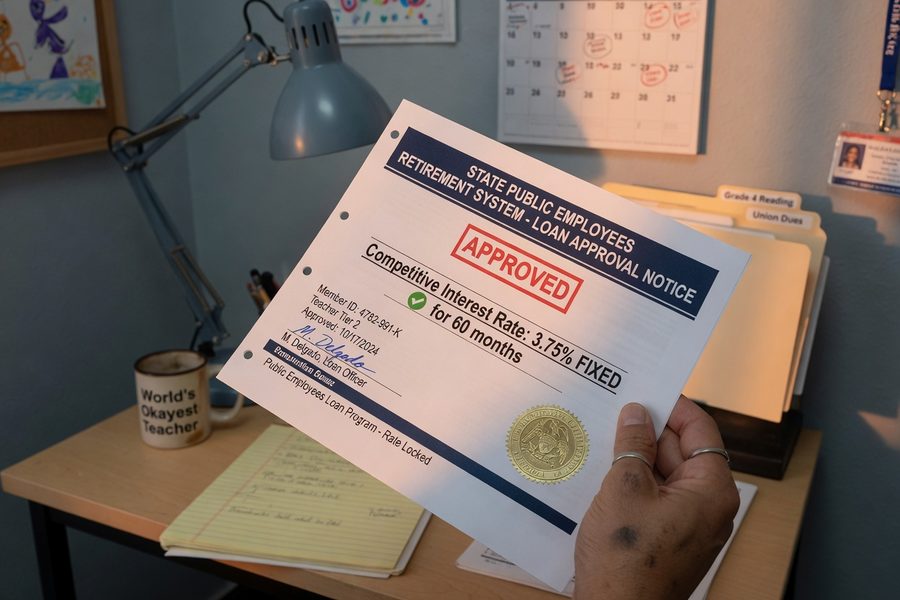

A fifth-grade teacher in Ohio paying 7.9% APR on a personal loan may have no idea her school district’s credit union affiliation can get her to 6.7% without a single phone call to a traditional bank. That gap is real, and it is what makes understanding public employee loan rates one of the most overlooked money moves available to government workers. According to the U.S. Department of Education’s 2026 announcement, federal Direct Loan borrowers enrolled in autopay now receive a full 1% interest rate reduction effective July 1, 2026 through June 30, 2028, a program-level benefit that operates entirely separately from any private lender discount.

This matters in mid-2026 because rising borrowing costs have made every fraction of a point consequential, and most lenders simply do not advertise the programs that serve public servants. The borrowers who find them tend to do so by accident.

| Factor | Reasons to Pursue Public Employee Rates | Reasons to Pause or Skip |

|---|---|---|

| Rate advantage | Credit unions tied to state associations offer APRs 0.5–1.25% below national averages | Advantage disappears if your credit score is below 680, since standard pricing may override member discounts |

| Autopay stacking | Federal Direct Loan autopay now saves 1% through June 2028, stackable with IDR plan benefits | Private lender autopay discounts are separate and rarely as large; some cap at 0.25% |

| Loan types covered | Mortgages, auto loans, and personal loans all have targeted programs through qualifying institutions | Not all loan types are eligible at every institution; mortgage benefits often require a separate application |

| Employment verification | Proof of full-time public employment is straightforward for most district or agency employees | Substitute teachers, seasonal workers, and contractors frequently cannot meet continuous full-time requirements |

| PSLF interaction | Public Service Loan Forgiveness is a parallel benefit; 1.2 million borrowers already approved | PSLF provides forgiveness after 120 payments, not upfront rate cuts; conflating the two leads to bad decisions |

| Union membership | Some unions negotiate additional auto and personal loan discounts on top of credit union rates | Union-specific deals may require six or more months of active membership before they activate |

Key Takeaways

- Your employer qualifies if it is a federal, state, or local government agency or a 501(c)(3) nonprofit; school districts at every level count.

- Your new rate should be at least 0.5 percentage points below your current rate to justify the paperwork and any balance-transfer fees involved.

- You are enrolled in autopay on a federal Direct Loan, which as of July 1, 2026 delivers a full 1% reduction, not the previous 0.25%.

- You hold verified membership in a credit union affiliated with a state teacher or public employee association, giving you access to member-only rate sheets.

- Your employment is continuous and full-time; part-time status or a recent job change within the last 90 days can disqualify you from most programs.

- You have checked whether your union negotiates an additional discount on top of credit union member rates, a combination that can exceed 1.5% in total savings.

- Your credit score sits at 680 or above, since below that threshold lenders typically apply standard risk-based pricing regardless of employer status.

What Actually Separates Public Employee Loan Rates From Standard Offers

Two structural advantages drive the pricing gap: lower default risk and subsidized membership. Public sector workers have more stable employment histories than the general borrower population, and that predictability gets priced in at institutions built to serve them. Lenders affiliated with state teacher associations or government employee unions can afford to charge less partly because they know their member base is not going anywhere.

Credit unions serving public employees such as those affiliated with the National Education Association or state-level counterparts routinely post APRs 0.5–1.25% below national averages on auto and personal loans once membership is verified. That range is not theoretical. It shows up on rate sheets that are never advertised to the general public, accessed only after a borrower submits employment documentation. Many of these institutions also offer relationship rate reductions, meaning an existing checking or savings account at the same credit union shaves another 0.25% off the stated member rate.

It is worth being clear on what these programs are not. Public Service Loan Forgiveness, administered by Federal Student Aid under the U.S. Department of Education, delivers forgiveness of remaining balances after 120 qualifying monthly payments, not a lower interest rate upfront., the Brookings Institution reports that 1.2 million borrowers have received PSLF approval, with $90.6 billion in balances forgiven. That is a forgiveness mechanism, and conflating it with rate reduction programs causes real confusion when borrowers are shopping for the lowest rate today.

Which Loan Types Carry the Deepest Discounts

Student loans see the most structured benefit. Auto loans come second. Mortgages offer targeted programs but require more documentation than most borrowers expect.

On the student loan side, the U.S. Department of Education’s July 2026 autopay reduction now delivers a full 1% rate cut for Direct Loan borrowers who enroll in automatic payment, effective through June 30, 2028. A borrower carrying a $40,000 Direct Loan balance at 6.54% would pay approximately $448 per month under a standard 10-year repayment plan. At 5.54% (after the 1% autopay reduction), that payment drops to roughly $432 per month, saving about $192 annually and nearly $1,920 over 10 years with no change in loan term. That is real money for a straight-forward enrollment step.

Auto loans through public employee credit unions often carry rates 0.75–1.0% below what a conventional bank or online lender quotes for the same credit profile. Personal loans show similar spreads. Mortgages are where the structure gets more complex. Some state housing finance agencies, including those in Texas, California, and New York, offer below-market first mortgage rates specifically for teachers and first responders, but these require applications through approved lenders rather than simply presenting an employment badge. If you are weighing a home purchase, understanding how each 20-point jump in your credit score affects mortgage pricing is worth doing before you apply anywhere, since employer status stacks on top of, not instead of, your credit tier.

Credit Unions and Institutions Built for Public Servants

PenFed Credit Union (Pentagon Federal Credit Union), once limited to military and government workers, now opens membership more broadly but retains preferred rates for verified government employees. State-specific institutions are often sharper on pricing. The Texas Employees Credit Union, the Florida State Employees’ Credit Union, and the SchoolsFirst Federal Credit Union in California each publish member-only rate schedules that run meaningfully below national averages for auto and personal loans. Membership typically requires proof of current employment with an eligible employer.

State teacher associations frequently maintain formal relationships with specific credit unions, in some cases negotiating rate floors that no individual borrower could access by walking in off the street. The National Education Association Member Benefits program connects teachers to financial products at rates negotiated at scale. Some state affiliates of the American Federation of Teachers have similar arrangements. The gap between what these programs offer and what a traditional bank quotes is not always dramatic on a single product, but stacking a union-negotiated auto loan rate with an autopay discount and a relationship account credit can push total savings past 1.5% in annual percentage rate.

One angle almost no mainstream article covers: substitute teachers and contract public workers. Most programs require “full-time continuous employment,” which technically excludes many substitutes. However, several credit unions tied to state education associations define full-time as averaging a certain number of hours per week over the prior 12 months, not necessarily a permanent hire classification. If you are a long-term substitute or work under a rolling contract, it is worth asking the specific institution how they define eligibility rather than self-disqualifying before you apply.

Stacking Discounts and Navigating Verification

Three layers of rate reduction can work simultaneously, and most borrowers only use one. The federal autopay reduction covers Direct Loans. Credit union membership discounts apply to most loan types at participating institutions. Union-negotiated rate floors apply specifically to members of certain affiliated unions. Getting all three requires coordinating three separate enrollment steps, none of which a lender will walk you through without prompting.

Employment verification typically requires a current pay stub, a letter from human resources confirming full-time status, and in some cases the employer’s tax identification number to confirm qualifying nonprofit or government classification. Some institutions also accept a state-issued employee ID badge alongside a pay stub. The process rarely takes more than a week, but timing matters. Applying during an active job change or within 60 days of a position reclassification can trigger additional documentation requests. If your employment situation is in flux, waiting until your status stabilizes almost always produces a cleaner approval.

One tradeoff worth naming directly: these programs reward stability but penalize transitions. A teacher who left a district mid-year to move to a charter school may find that the new employer’s nonprofit classification has not yet been verified by the institution’s eligibility database. Some databases update quarterly. That lag can delay access to member rates by 90 days or more even when the borrower is technically eligible. Checking your employer’s status before submitting an application saves time and avoids a hard credit inquiry on an application that would have been denied on administrative grounds.

For borrowers comparing these programs against what fintech lenders offer, the picture is nuanced. Alternative signals that digital lenders weigh in 2026 sometimes work in a public employee’s favor, since stable payroll data and consistent income patterns read well in algorithmic underwriting. But fintech platforms rarely target public sector workers specifically, and their rates are set by credit profile, not employer type. A government worker with a strong credit score may get a competitive quote from a fintech lender, but they will not get a rate that reflects public sector employment as a specific advantage.

Who Should and Who Should Not

Good candidates

These borrowers stand to save meaningfully with minimal effort.

- A full-time public school teacher with an active NEA or state affiliate membership who has not yet checked whether their district’s associated credit union offers member rates on auto or personal loans.

- A federal government employee with a Direct Loan balance who has not enrolled in autopay and is therefore leaving a full 1% annual rate reduction on the table starting July 2026.

- A state or local government worker whose municipality is affiliated with a public employee credit union and who currently holds their auto loan at a traditional bank at a rate above 7%.

- A firefighter, police officer, or first responder in a state with a housing finance agency first-time homebuyer program targeting public servants, whose mortgage application would benefit from a qualifying employer designation.

Who should skip it

These profiles rarely see enough benefit to justify the effort.

- A part-time or seasonal public employee who cannot document continuous full-time status, since nearly every program gates eligibility on that requirement.

- A borrower with a credit score below 660, where standard risk-based pricing will dominate regardless of employer status, often producing the same rate any member would receive anyway.

- Someone who changed public sector employers within the last 60 days and whose new employer is not yet verified in the credit union’s eligibility database, making the application timing poor.

- A borrower whose existing loan is already within 0.5 percentage points of the best available public employee rate, since switching costs including potential prepayment penalties erode most of the projected savings. Understanding when a rate drop actually saves money on a refinance helps run that math before committing.

Frequently Asked Questions

Do public employee loan rates require a specific credit score to access?

Most programs still apply risk-based pricing on top of employer status. A credit score below 680 typically activates standard pricing tiers that offset or eliminate the employer discount. Borrowers above 720 see the full benefit; those between 680 and 720 usually receive a partial reduction. Reviewing how credit score bands affect the interest rate you receive is useful preparation before applying to any public employee program.

Is PSLF the same as getting a lower interest rate as a public employee?

No. Public Service Loan Forgiveness cancels remaining federal student loan balances after 120 qualifying payments made under an income-driven repayment plan; it does not reduce the interest rate on those loans. Rate reductions for public employees come from separate programs: the federal autopay discount (now 1% through June 2028) and credit union membership rates. These operate independently and serve different financial goals.

Can a substitute teacher qualify for public employee loan programs?

Sometimes. Full-time status is the standard threshold, but several credit unions affiliated with state education associations define it by average weekly hours over the prior year rather than hire classification. A long-term substitute averaging 35 hours per week for 12 consecutive months may qualify at some institutions. Call the specific credit union and ask how they define “full-time” before assuming the answer is no.

How does the 2026 federal autopay discount work and who is eligible?

The U.S. Department of Education expanded the autopay interest rate reduction to a full 1% for federal Direct Loan borrowers effective July 1, 2026 through June 30, 2028. Eligibility requires active enrollment in automatic debit payments through your federal loan servicer. This applies regardless of whether your employer qualifies for PSLF, meaning private sector workers with Direct Loans also benefit.

Can I stack my union membership discount with a credit union rate?

Yes, in many cases. Unions affiliated with state credit unions sometimes negotiate rate floors that sit below the credit union’s standard member APR. Stacking that union-negotiated floor with an autopay discount and a relationship account reduction can produce total savings exceeding 1.5 percentage points compared to a conventional bank quote for the same loan amount and term. Ask both the union’s benefits coordinator and the credit union’s loan officer what combinations are permitted before assuming they cannot be combined.

Are fintech lenders a realistic alternative to public employee credit unions?

Fintech lenders can match or beat credit union rates for public employees with strong credit profiles, but they do not price employment type as a distinct advantage. A government worker at 750 FICO may get a competitive fintech offer on its own merits, but it will not reflect public sector status. Credit unions built for public servants are still the more reliable source of employer-specific rate advantages, particularly on auto and personal loans below $30,000.