Fact-checked by the CapitalLendingNews editorial team

The Verdict

AI loan matching platforms are worth using for most borrowers who want to compare real, personalized APRs without triggering multiple hard inquiries. They offer the clearest advantage when your FICO score is below 680 or you want offers from more than 10 lenders in one session. They are less decisive for borrowers with top-tier credit who already have strong bank relationships or complex income situations that algorithms struggle to read.

The single factor that determines whether an AI loan matching platform actually saves you money is whether it surfaces genuinely differentiated offers or just re-ranks the same three lenders every other site shows. That distinction matters more than the platform’s interface, the speed of its approval, or how slick its dashboard looks. According to The Business Research Company, the global AI-in-lending market reached $11.63 billion in 2025 and is projected to hit $14.71 billion in 2026, a 26.5% compound annual growth rate that reflects just how fast these tools are being built and deployed.

For borrowers, the timing is relevant because competition among platforms is sharpening lender incentives to offer better rates through these channels. The question is not whether the technology is real. It is whether the specific platform you are looking at will actually find you a deal worth taking.

| Factor | Reasons to Use AI Loan Matching Platforms | Reasons to Skip or Be Cautious |

|---|---|---|

| Lender breadth | Some platforms compare 90+ lenders in seconds, a scale no manual shopper can match | Many platforms have undisclosed referral agreements limiting which lenders appear |

| Credit inquiry impact | Most use soft pulls for pre-qualification, protecting your credit score during rate shopping | Accepting an offer still triggers a hard inquiry; multiple acceptances compound damage |

| Rate personalization | AI uses alternative data beyond FICO, often surfacing lower APRs for thin-file borrowers | Borrowers with complex income (self-employed, gig, seasonal) may get mismatch results |

| Speed | Pre-qualification in minutes versus days of bank paperwork and callbacks | Speed can pressure borrowers into accepting the first decent offer without due diligence |

| Data privacy | Established platforms operate under CFPB and FCRA data-handling rules | Sharing income, bank, and payroll data creates long-term data retention risk |

| Access for lower-credit borrowers | Platforms like RadCred now approve FICO scores below 600 using income-based models | Interest rates on approvals for sub-600 borrowers can still be 25%+ APR |

| Fee transparency | Good platforms display origination fees alongside APR for genuine comparisons | Some platforms earn referral commissions that are not always disclosed upfront |

| Loan complexity | Works well for standard personal loans, auto refinancing, and student loan comparison | Jumbo mortgages, business loans, and bridge financing rarely surface accurate matches |

Key Takeaways

- Your credit score is below 720 and you want to see whether alternative-data lenders like Upstart price your loan lower than your bank would

- You plan to compare at least 5 lenders and want to avoid triggering more than 1-2 hard inquiries during rate shopping

- The platform clearly distinguishes between soft-pull pre-qualification and the hard inquiry that follows acceptance

- Your loan amount falls between $2,000 and $50,000, the range where AI matching has the densest lender coverage

- You have reviewed the platform’s privacy policy and understand what financial data it retains after your session

- The platform displays origination fees and total loan cost alongside the APR, not just the headline rate

- You are not self-employed with irregular income, a situation where algorithmic matching often returns inaccurate pre-qualification amounts

What AI Loan Matching Platforms Actually Do in 2026

These platforms are not just upgraded comparison websites. A traditional rate aggregator collects your zip code and credit range, then shows you a static list. An AI matching platform ingests your full borrower profile, including income verification, employment history, bank cash-flow patterns, and sometimes payroll data, then queries lender APIs in real time to return personalized APRs that are specific to you, not to a credit tier bucket. The Consumer Financial Protection Bureau (CFPB) has noted that this shift toward alternative data can both expand credit access and introduce new risks of inconsistent treatment across borrower groups.

The practical difference shows up in the rate itself. A borrower with a 650 FICO Score and three years of stable direct-deposit history will get a different offer than a borrower with the same score and erratic income patterns. Traditional comparison sites cannot distinguish between these two people at all. Platforms built on machine learning models trained on large lending datasets, as Upstart describes its approach, can. That is what makes the technology useful rather than cosmetic.

What they do not do is negotiate on your behalf or guarantee that every lender in their network is offering its most competitive rate. The platform’s revenue model shapes what you see. If a lender pays a higher referral commission, some systems will surface that lender more prominently. This dynamic is not unique to AI platforms, but the algorithmic presentation makes it less visible than a clearly labeled sponsored result on a traditional site. Understanding this is essential before you treat any ranked list as objective. For borrowers managing their debt-to-income ratio (DTI) carefully, knowing how the platform weights its results matters: read about how debt-to-income ratio affects digital lending applications before you submit your first data point.

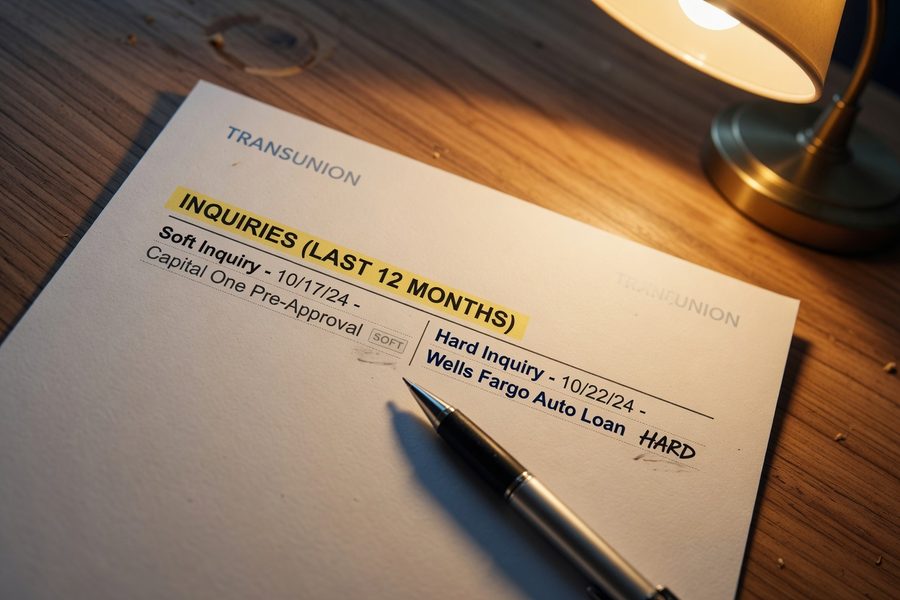

Soft Pulls, Hard Inquiries, and What Actually Happens to Your Credit Score

Most AI matching platforms use soft inquiries for pre-qualification, which means shopping five or six of them in a single week will not move your credit score. Only one hard inquiry follows: when you formally accept an offer and the lender pulls your full credit file. That structure is a genuine improvement over the old process of applying to three separate banks and absorbing three hard pulls.

The nuance most articles miss is that the protection ends the moment you accept. If you accept two offers to compare final terms, you have triggered two hard inquiries. FICO’s inquiry scoring rules allow rate-shopping windows of 14 to 45 days depending on the scoring model, during which multiple hard inquiries for the same loan type count as one. But that window applies to mortgage and auto loan inquiries more cleanly than it does to personal loans, where lender coding varies. The safe approach: complete your pre-qualification comparisons across platforms, choose one offer, and submit only that single formal application.

One concrete illustration of what this saves: a borrower comparing five personal loan offers the old way, applying directly to each lender, might see five hard inquiries drop their score by 15 to 25 points temporarily. Using a soft-pull platform first, then applying to one lender, limits the damage to 3 to 5 points. For a borrower right near the threshold between a good and fair credit tier, that difference can mean an annual percentage rate (APR) that is 1 to 2 percentage points lower on the accepted loan. Experian’s credit education guides offer a clear breakdown of how inquiry counts interact with overall score tiers for anyone who wants to see the numbers in detail.

Who Benefits Most, and Where the Algorithms Fall Short

Thin-file and lower-credit borrowers gain the most from AI matching platforms. That is the clearest, most defensible finding from how these tools have performed so far. RadCred’s March 2026 expansion explicitly targets borrowers with FICO scores below 600, using income-based approval models and offering same-day funding across all 50 states. For a borrower who would be declined outright at a traditional bank like Chase or Wells Fargo, even an approval at 24% APR is a meaningful alternative to a payday loan or credit card cash advance.

Borrowers with standard W-2 income in the 620 to 720 FICO Score range also tend to benefit, because AI models trained on large datasets can identify creditworthy patterns that FICO alone misses. A working paper examining machine learning in credit decisions from the National Bureau of Economic Research found that alternative-data models approved more applicants with comparable or lower default rates compared to traditional scoring approaches. Lenders like SoFi have built their own versions of this logic, weighting employment history and free cash flow alongside the standard FICO Score when evaluating personal loan applicants.

Self-employed borrowers, gig workers, and seasonal earners often find AI matching less reliable. The platforms read income signals well when deposits are regular and payroll-coded. Irregular deposits from multiple clients, 1099 income, or seasonal cash patterns can cause the algorithm to underestimate creditworthiness or return offers from lenders who will later decline after manual review. The Federal Reserve’s Report on the Economic Well-Being of U.S. Households consistently shows that gig and self-employed workers face structurally higher rates of credit denial, a problem that AI matching has not yet fully solved. If this describes your income, read how gig workers can approach digital lending during income gaps before assuming a pre-qualification result is firm.

High-loan-amount borrowers face a different limitation. Most platforms have the densest lender coverage between $2,000 and $50,000. Above that range, and especially for jumbo mortgage or large business loan needs, the number of participating lenders drops sharply and the AI’s matching advantage shrinks accordingly. The FDIC’s Small Business Lending Survey confirms that larger and more complex credit requests continue to rely on relationship-based underwriting rather than algorithmic matching.

Data Privacy, Platform Fees, and Costs You May Not See

Sharing your income data, bank statements, and employment history with an AI platform creates a data footprint that extends beyond your loan decision. The CFPB requires that platforms handling consumer credit data comply with the Fair Credit Reporting Act (FCRA), which governs how long data can be retained and who can access it. But compliance with FCRA does not mean the platform deletes your information after your session ends. Most retain it for marketing, model training, or partner sharing under terms buried in the privacy policy. The Federal Trade Commission (FTC) also enforces Gramm-Leach-Bliley Act requirements on financial data sharing, which gives borrowers some rights to opt out of certain third-party disclosures, though few bother to exercise them.

The platform’s business model is usually lender commissions, not borrower fees. That sounds borrower-friendly until you realize it means lenders who pay higher referral rates may get better placement in your results. A lender offering you 14.5% APR but paying the platform a 3% referral fee may appear above a lender offering 13.8% APR with a 1% fee. The displayed APR is accurate; the ranking is not neutral. Checking two or three platforms rather than trusting one is the practical hedge against this. The long-term implications of what happens to your data after a loan closes are worth understanding before you share anything: the details at what lenders do with your data after a digital loan closes are relevant here.

On fees: origination charges on personal loans range from 1% to 8% of the loan amount, and how a platform displays them varies. Some show a true APR that folds in the origination fee, as the CFPB’s APR disclosure rules are designed to require. Others show an interest rate with the fee listed separately in a footnote. On a $20,000 personal loan, the difference between a 3% origination fee ($600) and a 6% fee ($1,200) can exceed the interest savings from a 0.5-point rate difference over a three-year term. Always compare the total cost of the loan, not just the rate. Lenders like LendingClub and SoFi are generally more transparent about folding origination costs into their stated APR than some newer marketplace entrants.

Who Should and Who Should Not

Good candidates

These borrowers are likely to find AI matching platforms genuinely useful rather than just convenient.

- Borrowers with FICO scores between 580 and 720 who want to see whether alternative-data lenders price their loan lower than a traditional bank would

- Anyone shopping for a personal loan between $5,000 and $40,000 who wants to compare 10 or more lenders without multiple hard inquiries

- Borrowers with steady W-2 employment and consistent direct-deposit history, the income profile algorithms read most accurately

- First-time borrowers unfamiliar with how lenders weight different credit factors, who benefit from pre-qualification guidance; avoid the common digital lending mistakes first-time borrowers make before submitting

- Borrowers who want to refinance an existing personal loan and need a fast rate landscape before deciding whether the numbers work; the math on whether a rate difference actually saves money is covered in detail at when digital loan refinancing actually saves money

Who should skip it

Some borrower profiles will get limited or misleading value from AI matching platforms in their current form.

- Self-employed borrowers with variable monthly income, whose cash-flow patterns often cause algorithm-based pre-qualifications to be inaccurate or inconsistent

- Borrowers seeking loans above $100,000, where participating lender counts are thin and manual underwriting dominates

- Borrowers with FICO scores above 780 and existing bank relationships with institutions like Chase or Bank of America, who are unlikely to find meaningfully better rates on a platform than through a direct application to their primary lender

- Anyone in a rush who may accept the first decent offer without reviewing the origination fee, prepayment penalties, or total loan cost

Frequently Asked Questions

Do AI loan matching platforms hurt your credit score when you check rates?

Pre-qualification on most AI matching platforms uses soft inquiries, which do not affect your credit score. A hard inquiry only occurs when you formally accept an offer and the lender pulls your full credit file. If you accept multiple offers to compare final terms, each one triggers a separate hard inquiry. The three major credit bureaus, Experian, Equifax, and TransUnion, all treat hard inquiries the same way regardless of whether they originate through a platform or a direct lender application.

Are the APRs shown on AI loan platforms the actual rates you’ll get?

Pre-qualified APRs are estimates, not guarantees. The final rate is confirmed only after the lender completes a hard pull and verifies your income, employment, and identity. For most borrowers with accurately entered data, the pre-qualified rate and the funded rate are close, but they are not always identical, particularly if your income documentation shows something different from what the platform estimated.

Can you get approved through an AI matching platform if your credit score is below 600?

Yes, several platforms including RadCred now specifically target sub-600 borrowers using income-based approval models. Approval is more likely than at a traditional bank, but the APRs on these loans typically range from 20% to 35%. Comparing total loan cost against alternatives like credit union personal loans or secured lending products is worth doing before accepting.

How do AI loan matching platforms make money if they don’t charge borrowers fees?

Most earn referral commissions from lenders when a borrower accepts an offer through the platform. The commission structure can influence which lenders appear prominently in your results, even when displayed APRs are accurate. Using more than one platform and cross-checking a top offer against a direct lender application is the most reliable way to confirm you are seeing a competitive rate. The CFPB’s general guidance on comparing financial offers applies here: always look at the full cost, not just the headline number a platform surfaces first.

Sources

- The Business Research Company, Artificial Intelligence in Lending Global Market Report 2025-2026

- Stanford HAI, 2025 AI Index Report

- National Bureau of Economic Research, Machine Learning and Credit Decisions

- Upstart, About Our AI Lending Model

- Consumer Financial Protection Bureau (CFPB), Report on Alternative Data in Credit Decisions

- Consumer Financial Protection Bureau (CFPB), Fair Credit Reporting Act (FCRA) Compliance Resources

- Consumer Financial Protection Bureau (CFPB), Difference Between Interest Rate and APR

- Federal Reserve, Report on the Economic Well-Being of U.S. Households

- FDIC, Small Business Lending Survey

- Federal Trade Commission (FTC), Gramm-Leach-Bliley Act Financial Privacy Rule

- myFICO, How Credit Inquiries Affect Your FICO Score

- Experian, What Is a Good Credit Score?

- Federal Reserve, Consumer Credit Statistical Release (G.19)

- Consumer Financial Protection Bureau (CFPB), Consumer Credit Trends: Personal Loans

- Equifax, Understanding Credit Score Ranges