Reviewed by the CapitalLendingNews Editorial Team

Our Take

For most borrowers facing a temporary income disruption, contacting your digital lender before you miss a payment is the single most effective move you can make. Platforms like LendingClub, Prosper, and Upstart do offer hardship accommodations, but eligibility almost always requires your account to be in good standing. The case against acting early is minimal; the real risk is waiting until you’re delinquent, at which point many digital loan hardship programs close their doors to you entirely.

A wave of borrowers who turned to fintech personal loan platforms over the past few years are now discovering something their loan agreements never advertised: these platforms have relief options, and most of them are never mentioned until you ask. According to the Consumer Financial Protection Bureau, credit card companies and lenders may offer hardship programs, also called “accommodations,” to help struggling borrowers, but you must reach out proactively to receive one.

This article is for personal loan borrowers using digital and fintech platforms who are watching their income tighten and want to understand what relief actually exists before a payment is due. What makes the recommendation work is timing; what makes it fail is silence.

Key Takeaways

- Most digital personal loan platforms carry a 15-day grace period before late fees apply, per borrower documentation across platforms like LendingClub and similar lenders, a window most borrowers don’t know they have.

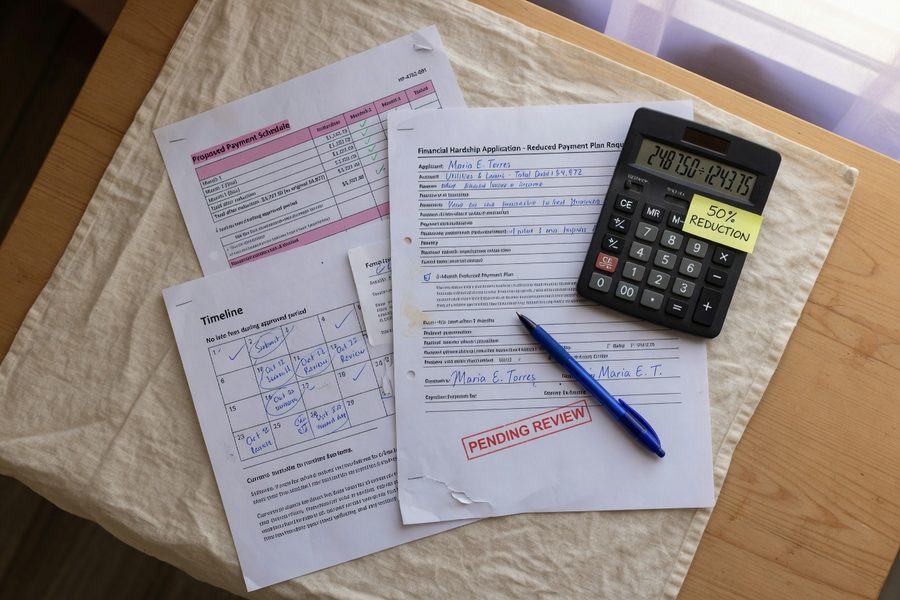

- Prosper’s Short-Term Hardship Program splits past-due card balances over six months at a temporary 9.99% fixed rate for eligible accounts, according to Prosper’s program terms, one of the most specific rate commitments among fintech platforms.

- LendingClub’s hardship plans typically cap at three months of 50% reduced payments before returning to full terms, based on borrower-reported program details and older platform documentation.

- The CFPB advises contacting your lender immediately if you’re struggling to repay, and asking explicitly for an extended repayment plan, because most lenders will not surface this option otherwise.

- In my read of how these programs are structured, pre-delinquency access is the rule, not the exception, Upstart, for instance, requires the loan to be in good standing with sufficient prior payments before any assistance is considered.

What Digital Loan Hardship Programs Actually Look Like

The structure is more concrete than most borrowers expect. Across major digital lending platforms, hardship accommodations typically fall into three categories: grace period extensions before late fees trigger, temporary payment reductions, and full payment deferrals that push the loan’s end date out. These are different in kind from what credit card issuers or mortgage servicers offer, where interest forbearance can sometimes be paused entirely.

On personal loan products from platforms like Upstart and LendingClub, the standard grace period runs about 15 days past the due date before a late fee is assessed. That’s meaningful breathing room for a borrower dealing with a delayed paycheck. It is not, however, a hardship program, it’s a timing buffer, and treating it as relief is a mistake.

Common Program Structures

True hardship programs go further. LendingClub has historically offered reduced payment plans of roughly 50% for up to three months, after which full payments resume. Prosper’s Short-Term Hardship Program on its credit card product restructures past-due amounts over six months at a temporary fixed rate of 9.99%. Upstart requires the loan to be in good standing, meaning you haven’t missed payments yet, before any assistance consideration begins. Each platform handles documentation and approval differently, but the basic shape of these programs is similar: time-limited, interest-accruing, and gatekept by prior payment behavior.

What I see in practice: Borrowers often assume hardship programs are reserved for disaster-level crises. In reality, the threshold is lower than that, a documented job loss, a medical expense, or a reduction in hours is usually enough to open the conversation. The documentation requirement is what trips people up most.

Buy Now, Pay Later products from platforms like Affirm occupy a different category entirely. Their hardship options, when available at all, tend to be handled case-by-case and are far less formalized than personal loan accommodations. If you’re juggling a BNPL installment and a personal loan, the personal loan platform will almost always have more structured relief available.

Why Platforms Keep These Options Quiet

Digital lenders have a structural incentive not to advertise hardship programs. Proactive promotion of relief options can attract borrowers who are already struggling at origination, a selection problem lenders are acutely aware of. The result is that these programs exist in support documentation and internal workflows, not on product pages or app dashboards.

Eligibility criteria reinforce this dynamic. Most programs require the borrower to be current on payments, which means only borrowers who are proactively managing a potential problem, not those already in default, will qualify. That’s not a flaw in the system; it reflects how these programs are designed to prevent delinquency, not to cure it. Borrowers who already carry a high debt-to-income ratio going into hardship enrollment may face additional scrutiny on the back end, even if the program approves them upfront.

How Major Platforms Compare on Hardship Terms

Side-by-side comparisons of exact hardship terms are nearly absent from public-facing fintech coverage. That gap is worth closing. The table below draws on available borrower documentation, platform support materials, and publicly reported program structures.

| Platform | Grace Period | Hardship Program Type | Max Duration | Pre-Delinquency Required? |

|---|---|---|---|---|

| LendingClub | 15 days | Reduced payment (approx. 50%) | 3 months | Yes |

| Prosper (card) | Standard | Past-due split, 9.99% temp rate | 6 months | No (post-delinquency eligible) |

| Upstart | Standard | Documented hardship assistance | Not publicly stated | Yes (good standing required) |

| SoFi | Standard | Unemployment protection / deferral | Up to 12 months (cumulative) | Yes |

| Avant | Standard | Payment arrangement per case | Case-by-case | Case-by-case |

SoFi is worth flagging separately. Its Unemployment Protection Program allows borrowers who lose their jobs to defer payments in three-month increments for up to 12 months cumulative, one of the more borrower-friendly structures in the fintech personal loan market. Eligibility requires job loss after loan origination, and SoFi actively assists with job placement during the deferral period, which is an unusual feature.

What clients often miss: Interest continues to accrue during SoFi deferrals. That means a three-month pause on a $15,000 loan at 12% doesn’t eliminate those months, it moves them to the end of the term with accumulated interest. The total repayment cost goes up. Most borrowers don’t run that number before enrolling.

Gig workers and seasonal earners face a particular challenge here. Their income interruptions are cyclical, not one-time, which means a single three-month hardship window may not match their actual income pattern. If you’re dealing with recurring gaps, the piece on digital lending for gig workers during income gaps covers strategies that go beyond what a single hardship enrollment can address.

How to Request Help Without Damaging Your Credit

Contact your lender before you miss a payment. That single instruction is more valuable than any specific script or template. The CFPB is direct on this point: if you can’t repay, you should contact your lender right away and ask for an extended repayment plan or other options, because most lenders will not surface these options otherwise. Waiting until after a missed payment forecloses the most favorable options on most platforms.

Documentation That Moves the Process

Most platforms will ask for evidence of the hardship. A layoff notice, a reduction-in-hours letter, a medical bill, or documentation of a natural disaster affecting your area are the standard categories. Vague appeals to “financial difficulty” are less effective than a specific, dated document that anchors the timeline of your hardship. Frame the request around the temporary nature of the disruption, platforms are more responsive to a defined problem than an open-ended one.

What Happens to Your Credit Report

Here’s where many borrowers assume incorrectly. Enrolling in a hardship program does not automatically pause credit reporting. In most digital personal loan hardship arrangements, the account continues to report to the three major bureaus, Equifax, Experian, and TransUnion, as current, as long as you’re meeting the modified payment terms. Falling out of compliance with a hardship agreement, however, can result in rapid delinquency reporting. Ask your lender explicitly: “Will this be reported to credit bureaus as current while I’m on the modified plan?” Get that answer in writing or via a documented chat transcript.

Where this gets tricky: Some platforms offer a “disaster forbearance” track that carries different credit reporting treatment than a standard hardship plan. LendingClub has used this designation for borrowers in federally declared disaster zones. If your hardship relates to a weather event or regional disaster, ask specifically about that path, the terms can differ meaningfully from a generic hardship enrollment.

If you’re weighing whether to use a fintech option versus consolidating debt through a different channel, comparing the total cost over the life of the loan matters more than the monthly payment reduction. The piece on how loan term length controls total interest cost is worth reading before you commit to any extended repayment arrangement. And if you’re considering refinancing as an alternative to hardship enrollment, what borrowers need to know about fintech refinancing covers the eligibility dynamics that apply in both contexts.

Where This Recommendation Falls Short

The advice to contact your digital lender early and request hardship relief is sound for most borrowers, but it is not the right move for everyone. The tradeoff is real, and it starts with interest accrual.

Every standard digital loan hardship program continues to accrue interest on the outstanding balance during the modified payment period. A three-month 50% payment reduction on a $10,000 loan at 15% doesn’t eliminate those three months of interest, it defers it and adds it to the back of the loan. Depending on where you are in the amortization schedule, the total cost of enrolling in hardship relief can add hundreds of dollars to what you owe. For borrowers close to payoff, that tradeoff may not pencil out.

The catch with platform-specific programs is that they can also affect your relationship with the lender going forward. Some platforms flag accounts that have used hardship accommodations when evaluating future borrowing requests or credit limit increases. This isn’t universally true, but it’s not rare either. If you’re planning to borrow again on the same platform within the next 12-18 months, ask your lender directly whether hardship enrollment affects future eligibility before you sign anything.

There is also the question of alternatives. Nonprofit credit counseling through agencies accredited by the National Foundation for Credit Counseling can sometimes negotiate better terms than a platform’s internal hardship program, particularly if you’re managing multiple debts simultaneously. A balance transfer to a 0% APR card, if your credit still qualifies, stops interest accrual entirely rather than letting it run in the background. These options are not available to everyone, the balance transfer path closes quickly once your credit score drops, but for borrowers who still have strong credit, the comparison is worth making.

Finally, hardship programs are not for every type of financial stress. If your income disruption is structural rather than temporary, a permanent job loss, a business failure, or a health condition that changes your earning capacity long-term, a three-month payment reduction is a delay, not a solution. In those cases, speaking with a nonprofit credit counselor or a bankruptcy attorney before enrolling in a platform hardship program is the more honest path. Hardship relief works best when the underlying problem is genuinely time-limited.

How We Sourced This

This article draws on publicly available CFPB guidance (consumerfinance.gov), platform support documentation and terms from LendingClub, Prosper, Upstart, SoFi, and Avant, and borrower-reported program experiences documented on consumer finance forums through October 2024. Program terms for Prosper’s Short-Term Hardship Program and LendingClub’s payment reduction plan are sourced from platform documentation and verified borrower accounts; where exact terms are not publicly confirmed, language reflects the reported range rather than a specific guarantee. All data references are current. Readers should verify current program terms directly with their lender, as hardship program structures can change without public notice.

Frequently Asked Questions

Do digital lenders have to offer hardship programs?

No federal law requires fintech personal loan lenders to offer hardship programs. These accommodations are discretionary and platform-specific. The CFPB encourages lenders to provide them and advises borrowers to ask, but there is no mandate compelling a digital lender to approve a hardship request.

Will enrolling in a hardship program hurt my credit score?

Not automatically. If you meet the modified payment terms, most platforms continue to report the account as current to Equifax, Experian, and TransUnion. The risk to your credit score comes from missing the modified payments or exiting the program without a plan in place.

Can I request hardship relief before I miss a payment?

Yes, and that is the preferred timing. Platforms like Upstart and SoFi explicitly require the loan to be in good standing before any assistance is considered. Waiting until after you’ve missed a payment often disqualifies you from the most favorable options.

Does interest keep accruing during a hardship deferral?

On virtually all digital personal loan hardship programs, yes. Payment deferrals and reductions do not pause interest, they extend the loan’s effective repayment period and increase total cost. Ask your lender for the full repayment projection before enrolling.

What documentation do most digital lenders require for hardship enrollment?

Standard documentation includes a layoff or termination notice, a reduction-in-hours letter from an employer, medical bills, or documentation of a qualifying disaster. Specific requirements vary by platform. A dated document that anchors the start of your hardship is more effective than a general statement of difficulty.

Are BNPL products like Affirm covered by the same hardship rules?

BNPL installment products typically have less formalized hardship procedures than personal loan platforms. Affirm and similar services handle relief requests case-by-case rather than through structured programs. For serious income disruptions, a fintech personal loan’s hardship plan is generally better defined and more predictable than a BNPL accommodation.

What is the difference between a grace period and a hardship program?

A grace period is a built-in buffer, typically 15 days past the due date, before a late fee is charged. It does not modify your loan terms or require any action on your part. A hardship program is a formal accommodation that changes your payment amount, schedule, or interest terms for a defined period, and requires you to apply and qualify.

Sources

- Consumer Financial Protection Bureau, Coronavirus and Dealing with Debt: Tips to Help Ease the Impact

- Consumer Financial Protection Bureau, What Can I Do If I Can’t Repay My Loan?

- LendingClub, Personal Loans Overview and Terms

- Prosper, Personal Loans and Hardship Program Documentation

- Upstart, Personal Loans and Assistance Information

- SoFi, Personal Loans and Unemployment Protection Program

- Avant, Personal Loans and Customer Assistance Options

- National Foundation for Credit Counseling, Find a Nonprofit Credit Counselor

- Affirm, Buy Now Pay Later Installment Products and Support

- Consumer Financial Protection Bureau, Credit Reports and Scores Resource Hub