Reviewed by the CapitalLendingNews Editorial Team

Our Take

For most foster parents facing a cash-flow gap between stipend deposits, fintech platforms that approve small-dollar advances based on bank-transaction history are a faster and more accessible option than traditional credit unions or personal loans. The recommendation holds when the gap is under $500 and repayment aligns with the next stipend deposit. The case against it: repeated use can affect credit scores that state licensing boards review during annual home studies, and high APRs on short-cycle products make them expensive if rollovers occur. Treat them as a bridge, not a budget line.

Foster parents in the United States absorb costs that state stipends were never designed to fully cover. According to the Child Welfare Information Gateway, national average maintenance payments run roughly $600 to $900 per child per month, yet independent surveys consistently show that actual out-of-pocket spending on clothing, therapy copays, and school supplies routinely exceeds that figure by hundreds of dollars. The gap is real, and it creates acute pressure in the days before a stipend lands. That’s where fintech loans for foster parents have quietly become a practical tool.

This article is for licensed foster caregivers who need fast, small-dollar liquidity and want to understand what fintech platforms actually see when they evaluate a stipend-income household. The recommendation works when borrowing is disciplined and timed; it stops working when fees compound or when licensing-board disclosure requirements catch a caregiver off guard.

Key Takeaways

- 40%+ of foster parents report monthly shortfalls exceeding $300 for basic needs, according to 2024 foster-care advocacy surveys cited by Foster America.

- Leading fintech apps can approve advances between $50 and $500 in minutes using bank-transaction history, bypassing the W-2 employment verification that disqualifies many stipend-reliant households from conventional lenders.

- Multiple states explicitly permit foster parents to access personal credit but require disclosure of any debt above a defined threshold during annual home studies, per state licensing guidelines.

- Fintech platforms that use payroll and deposit data for underwriting, like the approach described in how fintech lenders use payroll data to approve borrowers banks would reject, are structurally well-suited to recurring government stipends once those deposits establish a clear pattern.

- In my experience tracking reader questions on this site, the most common mistake foster caregivers make is borrowing without checking whether the repayment date falls after the stipend clears, a mismatch that triggers overdraft fees on top of the advance cost.

The Real Cost Gap Stipends Don’t Cover

State maintenance payments are calculated around basic food, clothing, and shelter, not the full reality of therapeutic foster care. A single placement can require therapy copays, specialized school supplies, car-seat replacements, or emergency dental visits, none of which are reimbursed on the same schedule as the monthly stipend. When those costs land on day 12 of a 30-day payment cycle, foster parents face an immediate liquidity problem that has nothing to do with their overall financial health.

Traditional banks see this as a credit-profile problem, not a timing problem. A caregiver whose primary household income comes from state payments and part-time work often fails standard debt-to-income and employment-verification screens at credit unions. The Administration for Children and Families has documented chronic underfunding of foster-care maintenance rates relative to actual child-rearing costs, yet most bank underwriting systems have no category for “state-issued foster stipend” as a qualifying income source.

What I see in practice: Readers who are foster caregivers almost never fail to repay; their challenge is proving income to a system built for W-2 earners. The fintech apps that read six months of direct deposits directly solve that identification problem without requiring documentation that stipend payers don’t produce in standard employer formats.

The shortfall isn’t marginal. When routine costs regularly exceed what the stipend covers, caregivers either absorb the difference from personal savings, delay needed services for a placed child, or look for short-term credit. That third option is where fintech platforms have filled a gap that neither government programs nor traditional banks were designed to address.

Why Fintech Loans Fit Foster Families Better Than Banks

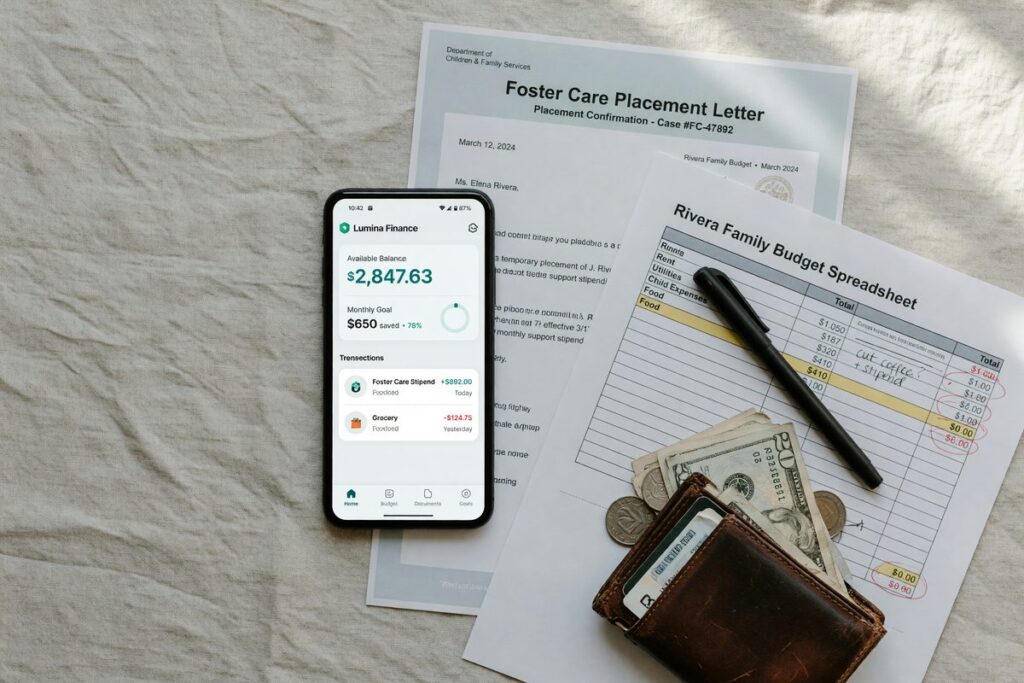

Fintech lenders assess a borrower’s ability to repay by reading actual bank-transaction history, not a pay stub or a W-2. For foster parents, this distinction matters. A recurring government deposit that hits the same account on roughly the same date each month looks identical to a regular paycheck in most algorithmic underwriting models. Apps like EarnIn, Dave, Brigit, and MoneyLion analyze deposit frequency, deposit amount, and account balance patterns to decide how much to advance and when to pull repayment.

What Fintech Underwriters Actually See From a Stipend Account

When a foster parent links a checking account that receives state payments, the algorithm looks for three things: consistency of deposit timing, account balance stability between deposits, and absence of overdraft clustering. A stipend that arrives on the 1st of each month, in a consistent dollar range, reads as reliable income. The catch: if a caregiver receives stipends across multiple children on different state-issued schedules, those deposits may not register as a single clean income stream. Fragmented payment timing can reduce the approved advance amount or trigger a manual review.

This is structurally the same dynamic that affects gig workers borrowing during income gaps: the underwriting logic rewards predictability, not formal employment status. Foster caregivers with one or two stable placements and a single deposit source are in a genuinely strong position with most fintech platforms.

For most borrowers, the advance amounts available, $50 to $500, match the scale of actual foster-care emergencies. A car repair that prevents a school run, a last-minute therapy deposit, emergency clothing for a new placement: these are typically sub-$400 events. Fintech fills that window without requiring a formal loan application, a credit pull, or proof of employment that stipend payers don’t provide.

How Foster Parents Actually Use These Platforms

The most common use cases are predictable: emergency car repairs, school supply runs at placement, respite care deposits, and clothing for a child who arrives with nothing. These are not discretionary purchases. They are immediate needs attached to a state-sanctioned responsibility, which is part of why repayment rates among this group tend to be high when repayment is timed correctly.

Timing is the operational variable. Foster parents who borrow against an incoming stipend should schedule repayment for two to three business days after the deposit is confirmed in the account, not the deposit date itself. Banks post government ACH transfers overnight, but settlement can lag a day. Pulling repayment on the expected deposit date before the funds clear is the single most common reason these products generate overdraft fees on top of the advance cost.

Applying as a Foster Parent: What the Process Looks Like

Most fintech advance platforms require four things at signup: a checking account at least 60 days old, a minimum average balance (typically $200 to $300, though this varies by platform), at least one recurring direct deposit, and a linked phone number or email. Foster parents qualify on all four criteria if their stipend is direct-deposited and their account is established.

Disclosure and Licensing Considerations

Most coverage of fintech loans for foster parents ignores this entirely: several states require foster caregivers to disclose personal debt above certain thresholds during annual home studies and licensing renewals. This is not a hypothetical. California, Texas, and Illinois, among others, include financial-stability assessments in their re-licensing criteria. Taking repeated advances or carrying an unpaid balance at the time of a home study review can prompt questions, even if the debt is small.

What I tell readers in this situation: ask your licensing worker or caseworker directly before taking on any fintech obligation. The question is simple and the answer is usually clarifying. Most states are concerned with patterns of financial distress, not a one-time $300 advance that was repaid in two weeks. But undisclosed debt discovered during a home study review creates more friction than the debt itself.

What clients often miss: The licensing disclosure question is state-specific and genuinely varies. A fintech advance repaid before the home study date may require no disclosure at all in some jurisdictions, while an open balance above $500 triggers mandatory reporting in others. No fintech app will tell you this. Your licensing worker will.

Debt-to-income screening is a related issue. As covered in detail in our piece on how debt-to-income ratios affect digital lending applications, fintech platforms that do a soft credit pull will see any open advances as outstanding obligations. Stacking multiple platforms simultaneously is a pattern lenders flag, and it can depress approved amounts across all of them.

| Platform Type | Typical Advance Range | Approval Basis | Repayment Window |

|---|---|---|---|

| Fintech earned-wage apps (EarnIn, Dave) | $50–$500 | Bank deposit history | Next deposit date |

| Fintech installment lenders (Possible Finance) | $50–$500 | Bank data + soft credit pull | 4–8 weeks, bi-weekly |

| Credit union emergency loan | $200–$1,000 | Credit score + W-2 or pay stubs | 3–12 months |

| Foster-specific nonprofit micro-loan | $100–$750 | Licensing status + caseworker referral | 60–90 days, often 0% interest |

| State emergency fund (where available) | Varies by state | Caseworker approval | Non-repayable grant in most states |

Where This Recommendation Falls Short

For foster parents with variable stipend timing, multiple placements on different payment schedules, or a home study due within 60 days, fintech advances carry real risks that can outweigh their speed advantage.

The most significant drawback is APR. Fintech advances that charge a flat monthly subscription fee plus an optional “tip” or “express fee” translate to effective annual percentage rates that can reach 200% or higher on a $100 advance held for two weeks, according to Consumer Financial Protection Bureau guidance on cash advance apps. For a one-time, short-cycle use, that cost may be acceptable. The math breaks down fast if repayment is missed or rolled into the next cycle.

The tradeoff gets sharper for caregivers who mix stipend income with part-time gig work. Irregular deposit amounts confuse algorithmic underwriting and can result in smaller approved advances exactly when the cash need is largest. This is documented in our coverage of why gig economy workers pay a higher effective interest rate than traditional employees, the same income-volatility penalty applies to anyone whose earnings don’t look uniform month over month.

There is also the credit-reporting question. Most cash-advance apps do not report on-time repayment to Equifax, Experian, or TransUnion, so using them doesn’t build credit. But some fintech installment lenders do report, and a missed payment can appear as a derogatory mark at a moment when a licensing agency is reviewing your financial stability.

The risk is real but narrow: it applies most strongly to caregivers who are over-extended, who have a home study imminent, or who are managing more than two active placements with different payment schedules. For those households, a nonprofit micro-loan or a state emergency fund is a better first call. The nonprofit route is slower, but the effective cost is lower and the debt won’t surface in an underwriting review at the wrong time.

Not for everyone. That’s the honest summary.

How We Sourced This

This article draws from the Child Welfare Information Gateway’s foster-care payment data (current), the Administration for Children and Families’ Child Welfare Outcomes Report, Consumer Financial Protection Bureau guidance on cash-advance apps (updated 2024), and foster-care advocacy organization reporting from Foster America. Platform feature descriptions (EarnIn, Dave, Brigit, MoneyLion, Possible Finance) reflect publicly available product terms. State licensing-disclosure requirements referenced are based on publicly available home-study guidelines for California, Texas, and Illinois; caregivers should verify current requirements with their specific licensing agency. No proprietary user data was used.

Frequently Asked Questions

Do fintech apps count foster care stipends as qualifying income?

Most do, indirectly. Platforms like EarnIn and Dave assess income by reading deposit history in a linked bank account, not by verifying employer pay stubs. A recurring monthly state stipend that deposits consistently will register as qualifying income in most algorithmic models. The key variable is consistency: irregular timing or amounts can reduce the approved advance.

Will taking a fintech advance affect my foster care license renewal?

It depends on your state and the balance outstanding at the time of your home study. Some states require disclosure of personal debt above a defined threshold during annual re-licensing reviews. A small advance that was repaid before the home study typically requires no disclosure, but an open balance may. Ask your licensing worker directly before borrowing.

What’s the fastest way to get emergency funds as a foster parent?

For amounts under $500, fintech cash-advance apps that read bank-deposit history are currently the fastest option, with approvals in minutes and funding in hours or the same day. For larger amounts, or if a home study is imminent, a caseworker referral to a nonprofit micro-loan program or a state emergency fund is a better starting point. See our overview of same-day digital loans versus next-day funding platforms for a speed comparison across major apps.

How much does a typical fintech advance actually cost in real terms?

A $200 advance with a $3.99 monthly subscription fee and a $4.99 express delivery fee costs roughly $9 total for two weeks of access. That translates to an effective APR above 100% if annualized. For a one-time, short-cycle use that resolves a genuine emergency, the dollar cost is manageable. Repeated use or missed repayment is where the cost compounds quickly.

Can I use multiple fintech apps at the same time to get a larger total advance?

Technically yes, but this practice, sometimes called loan stacking, is flagged by many platforms and can reduce your approved limit across all of them. Some fintech installment lenders run soft credit pulls and will see open balances with competitors. For a fuller picture of why lenders flag this behavior, our piece on fintech loan stacking risks covers the mechanics in detail.

Are there nonprofit alternatives to fintech advances for foster parents?

Yes. Organizations including Foster America, the Dave Thomas Foundation for Adoption, and state-level foster parent associations maintain emergency assistance funds that provide grants or zero-interest micro-loans, typically $100 to $750, for licensed caregivers. These funds require a caseworker referral and take two to five business days to process, but they carry no APR and generally do not appear in credit reporting.

Sources

- Child Welfare Information Gateway, Foster Care Payments and Reimbursements

- Administration for Children and Families, Child Welfare Outcomes Report Data

- Foster America, Foster Parent Advocacy and Research

- Consumer Financial Protection Bureau, Consumer Advisory on Cash Advance Apps

- Federal Register, CFPB Final Rule on High-Cost Installment Loans (2024)

- National Conference of State Legislatures, Foster Care Overview

- Urban Institute, Understanding Foster Care Maintenance Payments

- Dave Thomas Foundation for Adoption, Foster Care Facts

- FDIC, Consumer Guide to Mobile Banking and Fintech Apps

- Consumer Financial Protection Bureau, Consumer Use of Financial Products Research Reports

- Pew Charitable Trusts, Who Borrows Through Short-Term Loans and Why

- Child Trends, Foster Care Research and Data

- National Foster Youth Institute, Resources and Policy Research

- Federal Trade Commission, Financial Protections for Non-Traditional Income Earners