Fact-checked by the CapitalLendingNews editorial team

The Verdict

A fintech lender is usually the smarter choice for your first fix-and-flip if you have at least 5 completed flips on record and want speed above all else. If you are a true first-timer with no track record, a hard money lender is likely the better fit: more flexible underwriting, room to negotiate, and a human on the phone when the rehab goes sideways.

The single factor that swings the fintech vs hard money lender decision for first-time flippers is not the interest rate, it is experience. Fintech platforms such as Kiavi and New Silver run algorithmic underwriting that often requires a verifiable history of completed projects, while traditional hard money lenders like Easy Street Capital and BridgeWell Capital explicitly market programs for investors with no track record. The broader market is accelerating: according to the American Association of Private Lenders, the top 100 private lenders increased loan volumes by 25.3% in 2024, which means both lender types are competing hard for your business right now.

That competition gives first-timers more negotiating position than they realize, but only if they pick the right type of lender for their situation. Choosing wrong adds cost, friction, and risk to a deal that already has thin margins.

| Factor | Reasons to Choose Fintech | Reasons to Choose Hard Money |

|---|---|---|

| Speed to Close | 3–7 days via automated underwriting | 7–14 days, still faster than banks |

| Experience Requirement | Some platforms require 5+ prior flips | Many lenders accept zero prior flips |

| Rate Transparency | Instant online quotes, no negotiation needed | Rates negotiable, especially for stronger deals |

| Credit Impact | May pull personal credit (hard inquiry) | Often asset-based; softer on personal FICO |

| Flexibility on Extensions | Rule-based; extensions trigger automatic fees | Lender may negotiate extension terms personally |

| Rehab Draw Process | Online portal, faster inspections | Hands-on draw management with guidance |

| First-Timer Support | Self-service; limited mentorship | Some lenders offer dedicated advisor access |

| Entity Requirement | Often requires LLC formation upfront | Some lenders work with individual borrowers |

Key Takeaways

- Your new lender is the right fit if you can verify at least 2–3 comparable completed projects and need to close within 7 days.

- Hard money is likely smarter if this is your first or second flip and you have no established track record with a fintech platform.

- Your all-in rate (interest plus points) stays at or below 13% annualized, keeping margins viable on a typical $250,000–$400,000 fix-and-flip.

- Your loan-to-cost ratio does not exceed 90% of purchase price plus rehab budget, which is the standard ceiling for both lender types.

- You have a contingency fund covering at least 3 months of holding costs in case the renovation runs long.

- You have an LLC or legal entity ready, especially if applying to a fintech platform that will not lend to individuals.

- Your after-repair value (ARV) comps are within the last 90 days, since both lender types underwrite based on ARV and stale comps will kill your approval.

What Fintech and Hard Money Lenders Actually Are

Both lender types fund the same product: a short-term loan covering purchase price plus renovation costs, repaid when the property sells. The difference is in the engine behind the approval and the relationship that comes with it.

Fintech lenders like Kiavi, New Silver, and Groundfloor use automated underwriting models. You enter property data, pull ARV comps, and receive a rate quote within minutes. The appeal is speed and predictability, you know what you are getting before you sign. That automation comes with rigid qualification boxes. Kiavi, for example, has been reported to favor borrowers with a minimum of five verifiable prior flips, which filters out most true first-timers at the application stage.

Traditional hard money lenders operate differently. They are typically regional private lenders, family offices, or small funds that evaluate the deal and the borrower together. Business Purpose Lending, the broader category covering both types, represents roughly 8% of all U.S. home purchases according to Colonnade Advisors, a market large enough to support dozens of lenders in most metro areas. That scale means competition, and competition means some lenders actively court beginners to grow their book of business. Understanding how loan term length quietly controls your total interest cost is equally important here, since fix-and-flip loans are inherently short-term and every extra month on the clock is real money out of your pocket.

One caveat worth naming: neither lender type is a good fit if your renovation plan is largely guesswork. Both will require a detailed scope of work and contractor bids. Showing up without those documents, regardless of which type you approach, is the fastest way to get rejected or receive a punitively high rate.

Speed and Accessibility: Can You Actually Close in Time?

Fintech platforms close faster, typically 3–7 business days once the file is complete. Private lenders usually land in the 7–14 day range, which still beats the 30–45 day window a conventional bank like Chase or Wells Fargo requires. For competitive offers in markets where sellers want certainty, both options give you a credible proof-of-funds letter and a realistic close date.

The friction point for first-timers is qualification, not speed. Many fintech platforms require entity documentation (your LLC operating agreement), personal tax returns, and a completed project history before they will generate a formal term sheet. A first-timer who shows up with a great deal but no paper trail often stalls at the verification stage, and the clock is ticking on that purchase contract.

Asset-based underwriting is where private lenders have a real structural advantage for beginners. A borrower with a 620+ FICO Score, a reasonable down payment, and a believable renovation plan can often get approved in 48–72 hours. That approach is why lenders like Easy Street Capital position themselves specifically as first-timer friendly. For borrowers who need fast capital and have non-traditional income situations, the same logic that applies to digital lending for gig workers with income gaps holds here: asset-based underwriting is almost always more accessible than income-based underwriting.

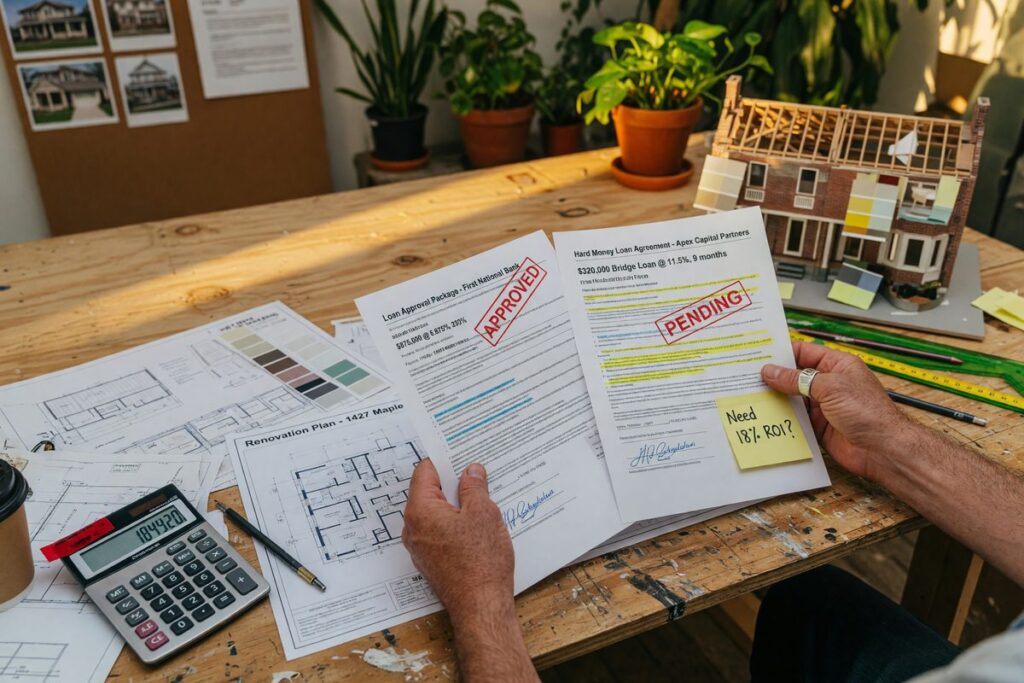

The Real Cost of Each Option on a $300,000 Flip

Rates run 8–13% annualized for both lender types, with 2–5 origination points paid upfront. The gap between the cheapest fintech quote and the most expensive hard money deal can be 3–4 percentage points, which sounds modest until you run the arithmetic on a real deal.

Consider a $300,000 fix-and-flip (purchase plus rehab) with a 6-month hold. At 10% interest and 2 origination points, your financing costs break down like this:

- Origination fee: $6,000 (2 points on $300,000)

- Interest for 6 months at 10%: $15,000

- Total financing cost: $21,000

Now run it at the upper end: 13% interest and 4 origination points:

- Origination fee: $12,000

- Interest for 6 months at 13%: $19,500

- Total financing cost: $31,500

That is a $10,500 difference on the same deal, before you factor in draw fees ($50–$200 per inspection), extension penalties (often 1–2 points for a 3-month extension), and any prepayment nuances. First-timers almost always take longer than planned. The National Association of Realtors’ Remodeling Impact Report notes that renovation timelines routinely run 20–30% over initial estimates, so extension exposure is a real cost, not a hypothetical one.

Fintech platforms often advertise lower starting rates, but those rates go to experienced investors with strong track records. A first-timer may receive a rate at the high end of the range from either lender type. The honest advantage of fintech is transparency, you see the numbers before committing. Private hard money lenders give you room to negotiate, which matters most when you bring a particularly clean deal or a large down payment. Knowing how debt-to-income ratio (DTI) affects digital lending applications can sharpen your positioning before you apply to either type.

Qualification Realities for First-Time Flippers

Asset-based underwriting is the fundamental advantage of hard money for beginners. Both lender types ultimately care about the deal, but fintech platforms layer on borrower-profile requirements that can knock out a first-timer before the property is even evaluated.

Fintech underwriting models are trained on historical borrower data. That means they weight prior flip experience heavily because, statistically, experienced investors default less. A true first-timer represents a data gap, and algorithms handle data gaps by either rejecting the application or pricing it punitively. Some platforms address this by requiring a co-borrower with experience, which can be a workable solution, but adds complexity for someone already navigating their first deal. The impact of a co-borrower’s credit profile on your loan rate is worth understanding before you add a partner to the application. Experian and the other major bureaus treat co-borrower inquiries as tied to both parties’ reports, so a partner with a troubled credit history can raise your effective APR even when your own file is clean.

Private lenders evaluate LTV and ARV first. A standard structure is 70–90% of purchase price plus 100% of verified rehab costs, capped at a maximum of 65–70% of ARV. What this means practically: if you bring a deal where the numbers work and you have a credible contractor lined up, many hard money lenders will fund it regardless of your personal flip history. Some will even treat the loan as a mentorship opportunity, walking you through the draw process and flagging budget overruns before they become defaults.

There is a personal finance angle that most articles skip. Fintech platforms pulling personal credit creates a hard inquiry on your FICO Score. Multiple applications to multiple fintech lenders in a short window, which many first-timers do while shopping rates, can suppress your score by 5–15 points per inquiry, complicating future conventional mortgage applications once the flip is done. Many traditional hard money lenders lend to the LLC entity with only a soft pull or no personal credit check at all, a meaningful advantage if you plan to apply for a CFPB-regulated conventional mortgage after the project closes.

What Happens When the Flip Goes Sideways

Default consequences are serious with both lender types: these are typically personal recourse loans secured by the property, meaning the lender can pursue you personally if the sale proceeds do not cover the balance. The difference is in what happens before default.

A fintech platform’s response to a problem is largely rule-based. Miss a draw inspection deadline, and the portal flags the loan. Need an extension beyond the automatic option? You will pay the posted extension fee, typically 1–2 points, with no exceptions negotiated. The digital self-service model that makes fintech fast on the front end makes it rigid when things get complicated. For landlords managing renovation financing across multiple properties, this inflexibility can be costly, as explored in the context of how landlords use fintech platforms to finance renovations without touching equity.

Private lenders operate on relationships, and relationships allow for conversations. A lender who knows you, visited the property, and has skin in the deal’s success is far more likely to grant a 30-day extension without penalty when a contractor walks off the job or a permit is delayed. This is not charity, it is rational. A completed and sold property recovers their capital; a foreclosure rarely does. That human flexibility is the strongest argument for choosing hard money on your first deal.

Bridge loan volumes surged 31% year-over-year in 2024 among Lightning Docs users, according to the American Association of Private Lenders, which signals that more investors are using these products, including beginners who have never managed a rehab default scenario. Knowing that your lender has both the experience and the willingness to work through problems with you is worth paying a slightly higher rate to access.

There is also a regulatory dimension that first-timers often overlook. Business-purpose loans sit outside most CFPB consumer-lending protections, and the Federal Reserve and FDIC do not directly supervise many private hard money shops. That means fewer disclosure requirements and fewer formal dispute-resolution channels than you would have with a bank loan. Vetting a lender’s reputation through the American Association of Private Lenders directory or checking their track record on Better Business Bureau matters more here than it would with a federally regulated institution.

Who Should and Who Should Not

Good candidates for fintech lenders

Experienced investors who prioritize speed and already have a deal pipeline will get the most out of fintech platforms.

- An investor with at least 5 verified completed flips who needs to close in under 7 days on a competitive offer

- A borrower who already has an LLC in place, clean financials, and strong ARV comps ready to upload

- Someone flipping in a high-volume market where the automated portal’s speed gives a genuine edge over other buyers

- An investor comfortable with self-service draw management who does not need lender guidance during the rehab

Who should skip fintech and go hard money

First-timers and anyone whose deal or profile falls outside a rigid algorithm’s approved range will fare better with a traditional private lender.

- A first-time flipper with zero or fewer than three prior deals, likely to face rejection or punitive pricing on fintech platforms

- A borrower with a complex income profile (self-employed, gig-based, or irregular W-2) who needs asset-based underwriting to qualify

- Anyone working on a deal in a secondary or rural market where automated ARV models are less accurate and human judgment matters more

- An investor who expects the renovation to run long and wants the ability to negotiate an extension without automatic penalty fees

- Someone who wants mentorship and draw guidance built into the lending relationship, not just capital

Frequently Asked Questions

Can a first-time flipper actually get approved by a fintech lender?

Some fintech platforms will approve first-timers, but most favor borrowers with verifiable experience. Kiavi, for instance, has been reported to weight prior completed flips heavily in its underwriting model. A first-timer with a strong deal and a large down payment has a better shot at approval through a traditional hard money lender that evaluates the property first.

What credit score do I need for a hard money fix-and-flip loan?

Many hard money lenders will work with borrowers at 620 FICO or above, and some go lower if the deal is strong and the down payment is substantial. Credit is a secondary factor in asset-based underwriting; the property’s ARV and your renovation plan carry more weight. Experian’s credit score guidance explains how lenders interpret FICO ranges if you need a baseline before applying.

Is a fintech lender faster than a hard money lender for fix-and-flip loans?

Generally yes. Fintech platforms can close in 3–7 business days compared to 7–14 days for most hard money lenders. If your file is incomplete or your profile triggers manual review, a fintech loan can stall just as long as any other. A well-organized application to a responsive hard money lender can close just as quickly.

What happens if my renovation runs over budget or over time?

Both lender types charge extension fees, typically 1–2 origination points for a 3-month extension. The difference is that hard money lenders may negotiate those terms or waive fees in good faith when a delay is outside your control; fintech platforms apply extension charges automatically through their portal with no exceptions. Budget a 3-month contingency holding cost before you sign with either lender.

Do fix-and-flip loans from either lender type show up on my personal credit report?

It depends on how the loan is structured and which lender you use. Fintech platforms often pull a hard inquiry on your personal credit during underwriting, which affects your FICO Score. Many traditional hard money lenders lend to the LLC entity and focus on asset-based underwriting with only a soft pull, a meaningful advantage if you plan to apply for a conventional mortgage after the flip is complete. The CFPB’s mortgage market data offers useful context on how hard inquiries factor into lender decisions at that stage.

Sources

- Colonnade Advisors, Business Purpose Lending Market Report, Fall 2024

- American Association of Private Lenders, Bridge and DSCR Activity Surges, 2025

- Consumer Financial Protection Bureau, Mortgage Market Activity and Trends

- National Association of Realtors, Remodeling Impact Report

- ATTOM Data Solutions, Home Flipping Report

- Experian, What Is a Good Credit Score?

- Federal Reserve, Financial Accounts of the United States (Z.1 Release)

- FDIC, Bank and Lending Regulatory Resources

- Better Business Bureau, Business Directory and Reviews

- American Association of Private Lenders, Lender Directory

- IRS, Limited Liability Company (LLC) Formation Guide

- Urban Institute, Who Are Private Mortgage Lenders?