Fact-checked by the CapitalLendingNews editorial team

Quick Answer

A HELOC interest rate floor is a contractual minimum rate that prevents your line of credit from falling below a set threshold, often 4% to 8%, no matter how far the Federal Reserve cuts rates. To protect yourself, ask every lender for the exact floor figure before signing, compare credit unions for floor-free options, and calculate the break-even on refinancing before switching lenders.

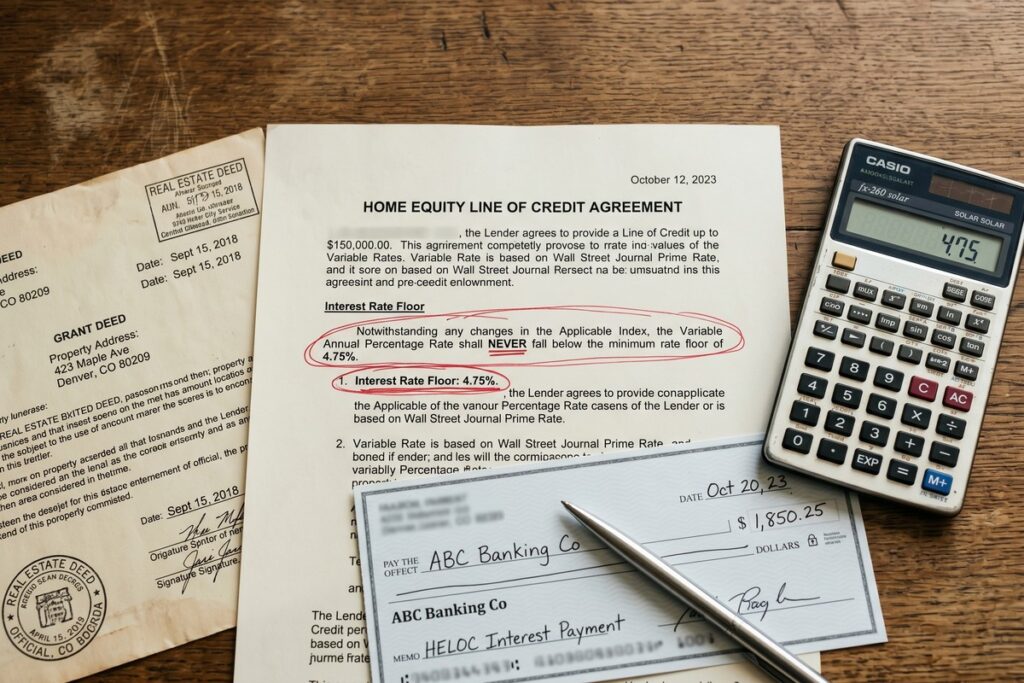

A HELOC interest rate floor is a clause buried in your loan agreement that sets a hard bottom on your rate, one the lender cannot go below regardless of what the Fed does. Borrowers who signed HELOCs at near-10% rates in 2023 and 2024 expected to ride cuts all the way down, but those with floor clauses hit a ceiling on their savings long before the formula rate reached its natural low. With total tappable U.S. home equity reaching a record $11.5 trillion entering Q2 2025, according to ICE Mortgage Technology, more households than ever are drawing on HELOCs and more are running into this exact problem.

The timing matters. First-quarter 2025 second-lien equity withdrawals rose 22% year-over-year to nearly $25 billion, the largest Q1 volume in 17 years, per the same ICE report. That surge happened precisely because falling rates made HELOCs look attractive again. What borrowers didn’t always know when they signed is that the floor clause insulates the lender from the very rate cuts making HELOCs appealing in the first place.

This guide is for anyone currently holding a HELOC, shopping for one, or trying to decide whether to refinance out of an existing line. By the end, you will know how floors work mechanically, where they hide in loan documents, what they cost you in real dollars, and how to find or negotiate your way into a floor-free product.

Key Takeaways

- A HELOC interest rate floor protects the lender, not the borrower. Unlike rate caps, floors receive no standardized disclosure requirement under the HELOC-specific provisions of Regulation Z, creating a documented information gap between what lenders know and what borrowers see at closing.

- Some lenders set floors as high as 7%–8%, according to HSH.com’s rate-term glossary, meaning a borrower with such a floor would receive zero benefit from Fed cuts even if the prime rate fell to 4%.

- The average outstanding HELOC balance is $32,904 per borrower as of Q4 2024, per Federal Reserve flow-of-funds data analyzed by HELN News, at a 0.75% rate gap caused by a floor, that balance generates roughly $247 in unnecessary interest annually.

- Early-termination fees on no-closing-cost HELOCs typically run $250 to $3,000, and new closing costs on a replacement HELOC can reach 2%–5% of the credit line, pushing the refinance break-even to four or five years.

- The rate spread between the best and worst HELOC offers for the same borrower profile has been documented at 1.5%–2.5%, translating to $1,500–$2,500 per year in unnecessary interest on a $100,000 draw, a real dollar value to shopping for a floor-free product.

- Not all lenders use floor rates. At least one credit union, First South Financial, explicitly advertises floor-free HELOCs, confirming that these products exist and are shoppable for borrowers willing to compare lenders.

In This Guide

- What a HELOC Interest Rate Floor Actually Is (And Why It’s Not the Same as a Rate Cap)

- How the Prime-Rate Formula Works, and Where the Floor Breaks the Chain

- Why Most Borrowers Never See the Floor Coming Before They Sign

- What Typical Floor Rates Look Like Across Lenders Right Now

- The Trapped Borrower Scenario: Why Refinancing Out Is Harder Than It Looks

- How to Find Your Floor Before You Sign (And What to Negotiate)

- Strategies for Borrowers Already Stuck in a High-Floor HELOC

- Frequently Asked Questions

Step 1: What a HELOC Interest Rate Floor Actually Is (And Why It’s Not the Same as a Rate Cap)

A HELOC interest rate floor is a contractual minimum below which your variable rate cannot fall, regardless of how far market rates drop. It is not a consumer protection, it protects the lender from earning too little on a low-rate environment. Understanding this asymmetry is the foundation of everything else in this guide.

How to Spot the Difference Between a Floor and a Cap

Rate caps and rate floors are both limits on how far a variable rate can move, but they serve opposite parties. A lifetime rate cap on a HELOC sets a maximum above which your rate cannot rise. The Consumer Financial Protection Bureau notes that variable-rate HELOCs must disclose the maximum possible rate upfront under Regulation Z. Lenders sometimes advertise caps as a borrower-friendly feature. Floors get no such fanfare, and no equivalent standardized disclosure is required by federal regulation.

In practice, a floor is usually expressed as a percentage in the rate-adjustment section of your HELOC agreement, something like “the minimum APR shall not fall below 4.00%”, written several pages into the document and not summarized on the term sheet handed to you at the start of the process. Most borrowers focus on the margin and the cap. The floor sits quietly until the rate environment makes it relevant.

What to Watch Out For

The floor only becomes visible when the formula rate (prime rate plus your margin) tries to drop below it. In a rising-rate environment, you’ll never notice it. In an aggressive cutting cycle, it becomes the thing that explains why your monthly payment stopped falling even after three or four Fed cuts in a row. Many borrowers blame their lender for slow updates to their rate when the real culprit is a clause they signed years earlier.

The TILA-RESPA Integrated Disclosure rules that require a standardized Loan Estimate and Closing Disclosure for most mortgages explicitly do not apply to HELOCs. HELOCs fall under the less consumer-protective HELOC-specific provisions of Regulation Z, which means you will not see a floor summarized in the same structured format you would expect from a purchase mortgage disclosure.

Step 2: How the Prime-Rate Formula Works, and Where the Floor Breaks the Chain

Most HELOCs are priced at the Wall Street Journal Prime Rate plus a lender margin. When the Federal Reserve cuts the federal funds rate, the prime rate drops by the same amount almost immediately, typically within one to two billing cycles. The floor breaks this transmission mechanism at a precise threshold.

How to Do This: Running the Math on Your Own HELOC

Work through this example to see the floor’s effect concretely. Suppose you have a HELOC priced at prime plus 0.25%, with a 4% floor. If the Fed cuts rates until prime reaches 3.75%, the formula produces 4.00% (3.75 + 0.25). That is exactly the floor. Now suppose the Fed cuts once more, pushing prime to 3.50%. The formula would produce 3.75%, but the floor keeps your rate at 4.00%. You receive zero benefit from that final cut.

Now add dollars to the picture. On a $75,000 outstanding balance, the difference between a 4.50% floor and a formula-derived rate of 3.75% is 0.75 percentage points. That gap costs roughly $562 per year in unnecessary interest, interest you pay solely because the floor clause exists. Over a three-year draw period, that is more than $1,600 paid to the lender with no corresponding benefit to you. The number scales directly with balance: a $150,000 draw would double the cost.

Understanding how loan term and rate interact over time is equally important here. A related read on this site covers how loan term length quietly controls how much interest you actually pay, which gives useful context for modeling HELOC draw and repayment period costs together.

What to Watch Out For

Borrowers who opened a HELOC at 9% or above and now see a rate of 7.5% often feel they are benefiting from Fed cuts. If their floor is 7%, however, they would be at 7% regardless of what the Fed does. The entire perceived “savings” from the cutting cycle is the formula rate converging toward the floor, not the floor itself delivering savings. Once the formula rate touches the floor, the borrower is fully insulated from any further cuts.

The average HELOC rate stood at 8.36%, per Bankrate’s survey of the 10 largest banks and thrifts in 10 large U.S. markets. That figure reflects a rate environment where borrowers with 7%–8% floors were already at or near the point where further Fed cuts would produce no savings at all.

Step 3: Why Most Borrowers Never See the Floor Coming Before They Sign

The disclosure problem is real, documented, and structural, not simply a matter of borrowers failing to read paperwork. The regulatory framework governing HELOCs creates a genuine information gap between what lenders know about the floor and what borrowers are required to be shown.

How to Do This: Where to Look in Your Loan Documents

When you apply for a HELOC, the lender must provide an early disclosure booklet (often the CFPB’s “What You Should Know About Home Equity Lines of Credit” publication or an equivalent) plus the actual HELOC agreement. The floor, if it exists, will appear in the rate-adjustment section of the agreement, typically labeled something like “Minimum Rate” or “Rate Floor”, and will be expressed as a numerical percentage. It is almost never on the first page of the term sheet, and it is rarely mentioned in the verbal summary a loan officer gives during the application process.

Lenders often lead with an introductory teaser rate, sometimes below 6% for the first six months, that obscures the floor’s relevance. The teaser rate expires before the formula rate would ever approach the floor, so borrowers focused on the promotional offer have no reason to think about what happens later. By the time the floor matters, the loan is already closed.

What to Watch Out For

Unlike rate caps, which lenders sometimes actively advertise as consumer protection features, floors receive no equivalent marketing treatment. They do not appear on most lender comparison websites, are rarely mentioned in financial press coverage of HELOC rates, and are not discussed proactively by loan officers because doing so would make the product look less competitive. The asymmetry is not random, it reflects a structural incentive to highlight what benefits borrowers and minimize what benefits the lender.

If a lender advertises a “no closing cost HELOC,” check the fine print carefully. These products frequently embed early-termination fees and floor clauses as the mechanism that compensates the lender for waiving upfront costs. A no-closing-cost loan with a 7% floor and a $500 termination fee can cost far more over a full cutting cycle than a loan with modest upfront costs and no floor.

Step 4: What Typical Floor Rates Look Like Across Lenders Right Now

Floor rates vary widely across lenders, and that variation creates a genuine shopping opportunity, but only for borrowers who know to ask. In the July 2025 rate environment, with the prime rate sitting in the 6.75%–7.50% range following the Fed’s three late-2024 and 2025 cuts, most borrowers are not yet trapped by their floors. The trap becomes material if the Fed resumes aggressive cutting toward a 3%–4% funds rate target.

How to Do This: Comparing Floor Rates Across Lender Types

National banks tend to set floors between 4% and 5%, reflecting their internal cost-of-funds models. Some large lenders set floors as high as 7%–8%, per HSH.com’s rate-term documentation, which would protect the lender entirely from any Fed cut scenario that leaves the prime rate above 6%. That is not a theoretical edge case, it is a documented practice across recognizable institutions.

Credit unions operate differently. As member-owned nonprofits, credit unions typically price HELOC margins 0.25%–0.50% lower than national banks for equivalent borrower profiles, and a meaningful subset offers floor-free structures. First South Financial, for example, explicitly advertises HELOCs with no floor rate, meaning the borrower’s rate tracks the prime formula all the way down without a contractual backstop. That makes the floor a genuine comparison variable, not a universal feature of HELOC products.

| Lender Type | Typical Floor Rate | Typical Margin Above Prime | Early-Termination Fee |

|---|---|---|---|

| National Bank (large) | 4.00%–8.00% | 0.25%–1.00% | $300–$750 |

| Regional Bank | 3.50%–6.00% | 0.25%–0.75% | $250–$500 |

| Credit Union | 0% (floor-free) to 4.00% | 0.00%–0.50% | $0–$250 |

| Online / Nonbank Lender | 4.00%–7.00% | 0.50%–1.25% | $500–$3,000 |

The rate spread between the best and worst offers for an identical borrower can reach 1.5%–2.5%, which translates to $1,500–$2,500 per year in unnecessary interest on a $100,000 draw. That gap is large enough to justify spending real time comparing at least three to five lenders, including at least one credit union, before signing any HELOC agreement.

This also connects to a broader dynamic covered in our guide to bridge loan rates versus HELOC costs for borrowers between properties, when you compare alternatives, the floor clause is one of the key variables that changes the true cost of a HELOC relative to a fixed-rate alternative.

Before you compare HELOC rates online, call or email at least two local credit unions and ask this exact question: “Does your HELOC product have a minimum interest rate floor, and if so, what is it?” Most comparison websites do not surface floor information. You have to ask directly, and credit unions are the lender type most likely to say “no floor.”

Step 5: The Trapped Borrower Scenario: Why Refinancing Out Is Harder Than It Looks

The most common response to discovering a punitive floor is “I’ll just refinance.” The math on that decision is often worse than borrowers expect, and the exit routes available can close without warning.

How to Do This: Calculating Your Real Refinancing Break-Even

Start with the annual cost of your floor. If your floor is 0.75% above where your formula rate would otherwise sit on a $100,000 balance, you are paying $750 per year in floor-related overage. Now calculate the exit costs. No-closing-cost HELOCs typically include clawback fees of $250–$750 if closed within two to three years, and some online lenders charge up to $3,000. A new HELOC brings closing costs of 2%–5% of the credit line amount, on a $100,000 line, that is $2,000–$5,000 in out-of-pocket costs before you save a dollar.

Divide total exit costs by annual floor overage to find your break-even. If total switching costs are $3,500 and you save $750 per year by escaping the floor, you break even in roughly 4.7 years. If you plan to pay off the balance or draw down the line within that period, staying put is the mathematically correct choice. Refinancing only makes financial sense when the remaining draw period exceeds the break-even horizon.

What to Watch Out For

There is a second exit route that can close entirely without borrower input. Lenders are permitted to reduce or freeze a HELOC’s available credit if home values drop significantly or if the borrower’s financial profile deteriorates. A borrower who planned to refinance into a better product may find the available equity insufficient to qualify for a new line at the moment they need it most, particularly in a falling-rate environment that also coincides with a housing market correction. The floor trap and the freeze risk are related: both tend to materialize under the same macroeconomic conditions.

There is also a version of this problem that is almost entirely absent from mainstream HELOC coverage: the repayment-period trap. When a HELOC’s draw period ends (typically after 10 years), the borrower can no longer pull funds from the line and must begin repaying on an amortizing schedule. The floor still applies to the variable rate on that amortizing balance, but the borrower now has far fewer restructuring options. They cannot tap the line to offset the cost, cannot easily roll it into a new HELOC without full qualification, and cannot lock a rate advance on a portion they have already drawn. Borrowers approaching the end of their draw period with a high floor face the most constrained version of this problem.

If your HELOC enters its repayment period while carrying a high floor, your options narrow sharply. You cannot draw new funds, so you cannot use the line to offset overage costs. A cash-out refinance of your first mortgage may be the only clean exit, but that resets your entire mortgage rate and term, a significant cost tradeoff if your first mortgage carries a low fixed rate from an earlier period.

Step 6: How to Find Your Floor Before You Sign (And What to Negotiate)

The most effective moment to deal with a floor is before you close, not after. Knowing exactly which questions to ask, and understanding what is and is not negotiable, puts you in control of the process rather than discovering terms after the fact.

How to Do This: The Specific Questions to Ask Every Lender

Before accepting any HELOC offer, ask each lender these questions in writing (email is sufficient and creates a record):

- Does this HELOC product have a minimum interest rate floor?

- If so, what is the exact floor percentage?

- Does the floor apply during the draw period, the repayment period, or both?

- Is the floor negotiable, or is it set by lender policy for this product?

- Is there an early-termination or early-closure fee, and if so, what is the exact amount and trigger period?

Most borrowers ask only about the margin and the lifetime cap. Those are important, but the floor and the termination fee are the two variables most likely to create long-term cost surprises, and they are the two least likely to be volunteered proactively.

What to Watch Out For

The margin is negotiable, especially if you have competing offers in hand. The floor typically is not. Floors are set by the lender’s loan program policy and rarely adjusted at the individual borrower level. Knowing this upfront shapes your strategy: if the floor is unacceptably high, the right move is to shop elsewhere, not to negotiate the same lender down. This is why getting competing quotes from at least one credit union matters. Credit unions are structurally more likely to offer floor-free products and lower margins, their nonprofit status reduces the cost-of-funds pressure that drives banks to set higher floors in the first place.

For context on how lenders more broadly set the parameters that determine your borrowing terms, our article on how lenders decide your loan limit and what you can do to raise it covers the pricing logic behind these decisions in more detail.

Request a copy of the full HELOC agreement, not just the term sheet or the early disclosure booklet, before the day of closing. Search the document for the words “minimum rate,” “floor,” and “minimum APR.” If you cannot locate any of those terms, ask the loan officer directly where the floor language appears. A lender who cannot answer that question is one worth scrutinizing more carefully.

Step 7: Strategies for Borrowers Already Stuck in a High-Floor HELOC

If you are already holding a HELOC with a floor that is limiting your rate savings, you have several options, each with honest tradeoffs. None of them are perfect, but each fits a different borrower situation.

How to Do This: Evaluating Your Three Real Options

Option 1: Refinance into a new HELOC. This makes sense when the annual floor overage significantly exceeds your total switching costs divided by your remaining time horizon. Use the break-even formula from Step 5. If you have six or more years of draw period remaining and your floor is costing you $800+ per year above where your rate should be, refinancing into a floor-free credit union product can generate real savings. Run the numbers honestly before acting.

Option 2: Use a fixed-rate advance. Many lenders allow borrowers to lock a portion of their HELOC balance at a fixed rate, sometimes called a fixed-rate sub-account or fixed-rate advance. This does not eliminate the floor on the variable portion of the balance, but it creates payment predictability and removes the variable-rate risk on the locked amount. It is a partial solution, not a complete one, and it works best for borrowers who expect rates to rise rather than fall further. If you are trying to escape a floor because you expect further Fed cuts, a fixed-rate lock runs counter to your goal.

Option 3: Stay put and optimize the balance. If your break-even on refinancing is four or more years and you expect to draw down or pay off the balance before then, staying in your current HELOC is the rational choice. Focus instead on paying down the principal more aggressively during periods when the formula rate is above the floor, the floor becomes irrelevant the moment the prime rate stabilizes at a level where your formula rate stays above it anyway.

What to Watch Out For

There is a psychological trap worth naming directly. Borrowers who opened HELOCs at 9% or above have watched their rates fall toward 7.5% and feel genuine relief. That feeling can mask the fact that a 7% floor means every rate reduction they have received was only the formula converging toward the floor, not the floor itself moving. Once the formula touches the floor, the perception of “benefiting from cuts” stops, but many borrowers do not notice the moment it happens. Checking your current rate against your stated floor once or twice a year is a simple habit that keeps you oriented.

A broader framework for thinking about rate timing decisions, including when to lock versus when to wait for additional cuts, is covered in detail in our guide on whether to lock your rate early or float it when the Fed signals a pause.

A HELOC is still one of the most cost-effective ways to borrow against home equity in a falling-rate environment, the problem is the floor clause specifically, not the HELOC structure itself. A fixed-rate home equity loan eliminates rate uncertainty entirely but typically prices 0.5%–1.0% higher than the equivalent HELOC margin. In a moderate cutting cycle of three to four quarter-point reductions, a floor-free HELOC will often outperform a fixed home equity loan on total interest paid.

Frequently Asked Questions

What exactly is a HELOC rate floor and how is it different from a rate cap?

A HELOC rate floor is a contractual minimum below which your interest rate cannot fall, regardless of how far market rates drop. It protects the lender. A rate cap is a contractual maximum above which your rate cannot rise, it protects the borrower. Federal regulations under Regulation Z require upfront disclosure of the maximum (cap) rate for variable-rate HELOCs, but no equivalent standardized disclosure requirement exists for floors, which is why borrowers are far more likely to know their cap than their floor at the time of signing.

How do I find out if my existing HELOC has a floor rate?

Pull your original HELOC agreement and search for the terms “minimum rate,” “minimum APR,” or “rate floor” in the rate-adjustment section. The floor will be stated as a specific percentage, for example, “the APR shall not fall below 4.00%.” If you cannot locate the language, call your lender’s customer service line and ask directly: “Does my HELOC have a minimum interest rate floor, and what is it?” You can also check your most recent account statement, though the floor may only appear in the original agreement, not on monthly billing documents.

Can I negotiate a lower floor rate on a HELOC before I sign?

In most cases, no. Floor rates are set by lender product policy and are rarely adjusted at the individual borrower level, even for well-qualified applicants. The margin above prime is negotiable, especially if you have competing offers from other lenders. If a specific lender’s floor is unacceptably high, the practical move is to take your business to a different lender, particularly a credit union, which is more likely to offer a floor-free product, rather than trying to negotiate the floor down with the original lender.

Do credit unions really offer HELOCs without a rate floor?

Yes. Some credit unions explicitly offer floor-free HELOC products where the rate is tied purely to prime plus the margin with no contractual minimum. First South Financial is one documented example that advertises this feature. Credit unions also tend to price HELOC margins 0.25%–0.50% lower than national banks for comparable borrower profiles. This makes the floor a genuine shopping variable: checking at least one credit union during your HELOC comparison process is a concrete way to lower your long-term borrowing cost.

How much does a HELOC floor actually cost me in real dollars?

The cost depends on the size of the gap between your floor and where your formula rate would otherwise sit. On a $75,000 balance with a floor 0.75 percentage points above the formula rate, the annual overage is approximately $562. On a $150,000 balance with the same gap, the annual cost doubles to roughly $1,125. The gap grows as the Fed cuts rates further, each additional quarter-point cut that would reduce your formula rate below the floor adds to the overage without changing what you actually pay.

Should I refinance out of my HELOC to escape a high floor?

Only if your break-even horizon is shorter than your remaining draw period. Total the switching costs: early-termination fees (typically $250–$3,000) plus new closing costs on the replacement HELOC (typically 2%–5% of the credit line). Divide total switching costs by your annual floor overage to find the break-even in years. If you expect to have the line open and the balance drawn for longer than that break-even, refinancing makes financial sense. If you plan to pay off the balance soon, staying put and directing extra cash toward principal is the better choice. For further context on how loan costs compound over time, our guide to how loan term length controls total interest paid provides useful framing.

What happens to my HELOC floor when my draw period ends and I enter repayment?

The floor remains in effect throughout the repayment period on the variable-rate balance. This is a distinct and often overlooked version of the problem because your options narrow significantly once the draw period ends: you can no longer pull new funds from the line, you cannot easily lock a rate advance on an already-closed draw period, and refinancing into a new HELOC requires full qualification and likely new closing costs. Borrowers approaching the end of their draw period with a high floor are in the most constrained position of any HELOC holder and should evaluate refinancing options before the draw period closes, not after.

Will the Fed cutting rates always lower my HELOC rate?

Not if your HELOC has a floor. Each Fed cut reduces the federal funds rate, which lowers the prime rate by the same amount almost immediately. Your HELOC rate will follow that decrease, but only down to your floor. Once the formula rate (prime plus margin) reaches the floor, no further cuts matter to your rate. In the July 2025 environment with prime in the 6.75%–7.50% range and typical floors at 4%–5%, most borrowers still have room for cuts to benefit them. That cushion disappears if the Fed resumes aggressive cutting toward a 3%–4% funds rate target over the next two to three years.

Is a fixed-rate home equity loan better than a HELOC with a floor?

It depends on how far rates are likely to fall and what floor the HELOC carries. A fixed-rate home equity loan eliminates rate uncertainty entirely but typically prices 0.5%–1.0% higher than the equivalent HELOC margin at the time of origination. In a moderate cutting cycle of three to four quarter-point reductions, a floor-free HELOC generally produces lower total interest. A HELOC with a floor set at or near current market rates offers little advantage over a fixed loan because the floor effectively functions as a pseudo-fixed rate anyway, without the certainty of knowing your rate upfront. For borrowers who want rate certainty and are comparing these two options, reviewing how fixed versus adjustable rate structures differ in practice can help clarify the tradeoffs.

Can my lender freeze my HELOC if home values drop, and how does that relate to my floor?

Yes. Under federal rules, lenders are permitted to reduce or freeze a HELOC’s available credit if the property value declines significantly or if the borrower’s financial situation deteriorates. This risk is most relevant to borrowers who were planning to refinance out of a high-floor HELOC: if values fall before they execute the refinance, the new lender may not extend sufficient credit to replace the existing line. The floor trap and the freeze risk share the same macroeconomic trigger, a falling-rate environment that also coincides with housing market weakness, making borrowers who hold high-floor HELOCs in overvalued markets doubly exposed.

Sources

- ICE Mortgage Technology, June 2025 Mortgage Monitor: Record Levels of Home Equity and Falling Rates Drive Highest HELOC Withdrawals Since 2008

- ICE Mortgage Technology, June 2025 Mortgage Monitor Full Report

- HELN News / Bankrate, Average HELOC Rate December 2024

- HELN News, Federal Reserve Flow-of-Funds Analysis: Average Outstanding HELOC Balance Q4 2024

- Consumer Financial Protection Bureau, What Is a Home Equity Line of Credit (HELOC)?

- Federal Reserve, Selected Interest Rates (H.15 Release): Prime Rate Historical Data