Fact-checked by the CapitalLendingNews editorial team

Quick Answer

No origination fee digital lenders can be a genuinely better deal, but only under specific conditions. To determine whether one saves you money, you need to compare full APRs across at least three lenders, calculate total repayment cost over your actual loan term, and audit documents for hidden fees. On a $20,000 loan, skipping a 5% origination fee saves $1,000 upfront, but a higher interest rate on a 5-year term can erase that savings entirely.

Choosing among no origination fee digital lenders sounds simple: skip the fee, pay less. In practice, the math is more complicated, and the “better deal” depends almost entirely on your loan amount, repayment term, and credit profile. According to Experian’s consumer guidance, personal loan origination fees typically range from 1% to 8% of the loan amount, meaning a borrower taking out $50,000 could pay $2,500 to $4,000 before receiving a dollar of their funds. That upfront hit is real. But a no-fee lender charging a meaningfully higher interest rate can cost you just as much, or more, over a multi-year term.

The digital lending market has expanded rapidly, with platforms like LightStream, SoFi, PenFed, and Discover now competing specifically on the no-fee angle. As of early 2026, the personal loan market is more crowded than ever, and fee-waiver marketing is one of the primary tools lenders use to attract prime borrowers. Understanding what is actually being traded away when an origination fee disappears is not just useful, it is the difference between picking the cheapest loan and picking the one that sounds cheapest.

This guide is written for borrowers who have already decided they need a personal loan and want to evaluate whether a no-fee digital platform is the right choice for their specific situation. By the end, you will know how to read the real cost of any loan offer, what credit profile this market assumes you have, and exactly when paying an origination fee is the smarter financial move.

Key Takeaways

- Personal loan origination fees typically range from 1% to 8% of the loan amount, according to Experian, on a $50,000 loan, that is up to $4,000 in upfront costs a no-fee lender eliminates.

- The average two-year personal loan rate at commercial banks was 12.32% as of Q4 2024, per Federal Reserve data cited by Experian, context for evaluating whether a no-fee lender’s rate is truly competitive.

- Credit unions averaged 10.64% APR on three-year personal loans in Q4 2025, according to NCUA data via NerdWallet, often with no origination fees, making them a frequently overlooked alternative to fintech platforms.

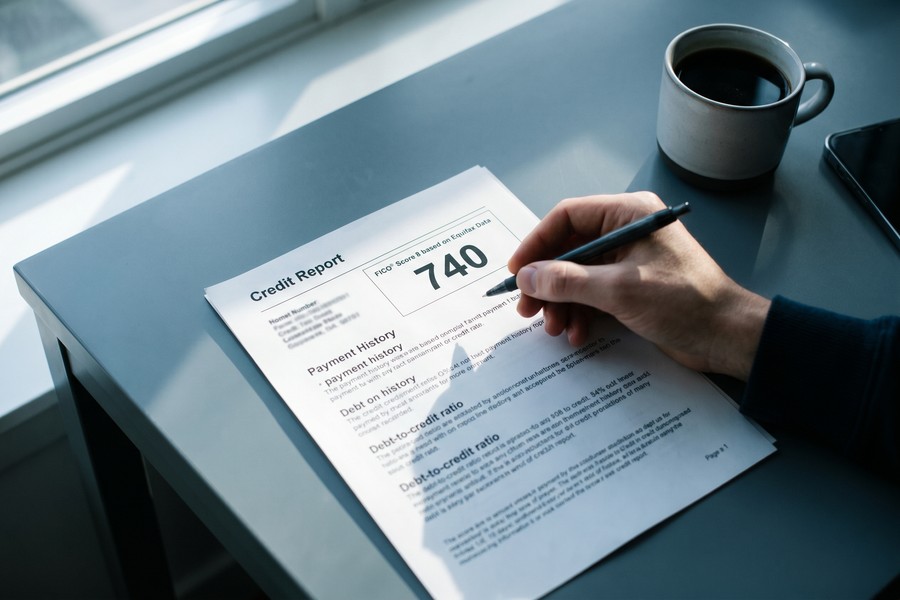

- Top no-fee digital lenders like LightStream require a FICO score of 740 or higher, and most require at least 670, meaning the majority of U.S. borrowers with fair or subprime credit cannot access this market at all.

- The Consumer Financial Protection Bureau advises that borrowers review all required disclosures carefully, because fees are sometimes listed under alternative names like “administrative fees” or “processing fees”, which are functionally identical to origination fees.

- On short loan terms of 12 to 24 months, avoiding a fee saves more in real dollars because interest has less time to accumulate and the fee represents a larger share of total cost; on terms of 5 to 7 years, a higher no-fee APR can erase or reverse those savings.

In This Guide

- What does an origination fee actually cost you on a personal loan?

- How do no-fee digital lenders make money if they waive the origination fee?

- What credit score do I need to qualify for a no-origination-fee loan?

- How do I compare a loan with a fee versus a loan without one?

- When is a no-origination-fee loan actually the better financial choice?

- What are the tradeoffs of AI-driven underwriting on no-fee digital platforms?

- How do I shop no-origination-fee digital lenders without getting fooled by hidden fees?

- Frequently Asked Questions

Step 1: What does an origination fee actually cost you on a personal loan?

An origination fee is a one-time charge, typically expressed as a percentage of the loan amount, that a lender collects for processing your application and funding your loan. Most borrowers understand this in theory. What catches them off guard is the mechanical reality: the fee is usually deducted from your loan proceeds before you ever see the money, but you still owe and pay interest on the full amount you requested.

How Origination Fees Work in Practice

Here is the concrete version. You apply for a $20,000 personal loan with a lender that charges a 5% origination fee. At funding, you receive $19,000. Your loan balance, however, is $20,000, and interest accrues on that full $20,000 from day one. That $1,000 gap between what lands in your account and what you owe is the hidden sting that most borrowers do not fully register until they run the numbers.

There is a second, less-discussed variant that no top-ranking article explains clearly: some lenders add the origination fee on top of the loan amount rather than deducting it from proceeds. In that structure, you request $20,000, receive $20,000, but your loan balance is $21,000. This is common in some buy-now-pay-later products and certain installment loan providers. The borrower gets the full funds but takes on a larger debt. Neither method is inherently better for the borrower, but they are structurally different, and confusing one for the other leads to badly miscalculated comparisons.

The average personal loan amount in the United States was $6,200 in Q4 2024, according to TransUnion data via Bankrate. At that loan size, a 5% origination fee costs $310, significant but not catastrophic. Scale that to a $50,000 home improvement loan, and the same fee rate costs $2,500 before your first payment. The larger the loan, the more a fee waiver is worth in concrete dollars.

What to Watch Out For

Origination fees also affect your effective APR. A loan advertised at 9% interest with a 5% origination fee does not carry a 9% APR, the fee pushes the true cost higher. The exact effective APR depends on the loan term, but on a 3-year loan, that 5% fee adds roughly 2 to 3 percentage points to your effective rate. Always ask for the APR disclosure, not just the interest rate, before making any comparison. The Federal Trade Commission enforces the Truth in Lending Act, which legally requires lenders to disclose APR, so any lender that cannot or will not give you an APR in writing before you sign is a lender worth walking away from.

Under the Truth in Lending Act and Regulation Z, every creditor is required to disclose the APR as a standardized cost measure. The National Credit Union Administration’s compliance guide confirms that APR folds in origination fees and other finance charges, making it the only apples-to-apples comparison tool available to borrowers.

Step 2: How do no-fee digital lenders make money if they waive the origination fee?

No-origination-fee digital lenders are not charities. When they waive an upfront fee, that revenue gap is recovered somewhere else, usually through a slightly higher interest rate, ancillary product sales, or both. Understanding the business model tells you where to look for the cost that replaced the fee.

Where the Revenue Goes Instead

The most common tradeoff is a higher baseline interest rate. A lender that charges a 6% origination fee might offer a loan at 8% interest. The same lender with no origination fee might price the same borrower at 9.5% or 10% interest. On a short-term loan, the fee-free version can still win on total cost. On a 5- or 7-year loan, that extra 1.5 percentage points of annual interest can accumulate beyond what the origination fee would have cost. This is the core math most borrowers skip.

Autopay discounts add a layer of opacity. Many digital lenders advertise a rate reduction of 0.25% to 0.50% for enrolling in automatic payments, but the baseline rate is set with that discount baked into the marketing. Borrowers who miss a payment or cancel autopay pay a higher rate than the advertised number, which is rarely the first thing lenders explain.

Cross-selling is the other major revenue mechanism. SoFi, for example, offers no-origination-fee personal loans but earns revenue from banking products, investment accounts, insurance, and student loan refinancing. The personal loan is partly a customer acquisition tool. Upstart and similar AI-driven platforms earn money through bank and credit union partnerships, they sell their underwriting technology rather than holding loans on their own books, which changes their incentive structure compared to a traditional lender. For a deeper look at how fintech platforms are using alternative data to expand their lending reach, see this analysis of how fintech lenders use payroll data to approve borrowers banks would reject.

What to Watch Out For

Fee laundering is real. Lenders sometimes relabel origination fees as “administrative fees,” “processing fees,” “financing fees,” or “documentation fees.” Functionally, these are identical, a percentage of the loan amount collected at or before funding. The FDIC’s consumer compliance examination manual confirms that any such charge must be accurately reflected in the APR calculation under Regulation Z. The practical check is straightforward: on a loan with genuinely zero fees, the APR will equal the stated interest rate. If the APR is higher than the stated interest rate, fees exist, regardless of what they are called.

Before signing any loan agreement marketed as “no origination fee,” verify that the APR equals the stated interest rate. If those two numbers differ, a fee is embedded in the loan, it is just not being labeled as an origination fee. This check takes 30 seconds and can save hundreds of dollars.

Step 3: What credit score do I need to qualify for a no-origination-fee loan?

The honest answer is that most no-origination-fee digital lenders require good to excellent credit, and the best-priced offers are reserved for borrowers near the top of the credit spectrum. This is not incidental, it is the business model. Fee waivers are used to attract low-risk borrowers who have many competing offers and enough creditworthiness to repay reliably.

The Credit Score Reality by Lender

LightStream, consistently cited as one of the most competitive no-fee lenders, prefers FICO scores of 740 or higher. Discover Personal Loans and PenFed Credit Union are somewhat more accessible, recommending scores of 670 or above. As Experian notes, it generally takes at least good credit, defined as a FICO score of 670 or higher, to qualify for a personal loan with no origination fee. Borrowers below that threshold typically cannot access this market at all.

This creates a structural inequality that most articles on this topic ignore. The borrowers who would benefit most from saving $500 to $2,500 in upfront fees are often the same borrowers who have fair credit (580 to 669 FICO) and fewer options. They are the ones most likely to face origination fees of 5% to 10% from lenders willing to approve them. The no-fee market is, in practice, designed for borrowers who already have the most negotiating leverage.

What Fair-Credit Borrowers Should Do Instead

If your credit score sits between 580 and 669, the no-fee conversation may be moot. Focus instead on total APR across lenders willing to approve you, and consider whether a fee-charging lender with a lower interest rate produces a better outcome than the alternative. Credit unions are worth checking seriously: the NCUA data shows an average three-year personal loan APR of 10.64% in Q4 2025, and many credit unions charge minimal or no origination fees even for members with near-prime credit. For borrowers with non-traditional income, the path to approval often runs through alternative underwriting, understanding how debt-to-income ratio affects digital lending applications can help you prepare a stronger application before you apply.

The average three-year personal loan APR at credit unions was 10.64% in Q4 2025, according to NCUA data cited by NerdWallet, often with no origination fees and more flexible credit requirements than competing fintech platforms.

Step 4: How do I compare a loan with a fee versus a loan without one?

APR is the only number that puts fee-charging and no-fee loans on equal footing. Comparing stated interest rates across lenders, some with fees, some without, is an apples-to-oranges exercise that reliably misleads borrowers.

A Side-by-Side Example With Real Numbers

Consider a $15,000 loan over three years. Lender A offers a 9% interest rate with a 5% origination fee. After the fee deduction, you receive $14,250, pay interest on $15,000, and your effective APR rises to approximately 11.7%. Lender B offers 11% interest with zero fees. Your APR is 11%. In this case, despite the lower stated interest rate, Lender A actually costs you more. On a 3-year term, the interest rate difference between these two options is smaller than the fee drag, so the no-fee lender wins.

Now extend the same scenario to a 5-year term. Lender A’s effective APR is still approximately 11.7%, while Lender B’s APR is 11%. Over 60 months instead of 36, an extra 0.7 percentage point applied to a $15,000 balance accumulates meaningfully. The no-fee lender still wins in this specific example, but the margin narrows. Change Lender B’s rate to 13% with no fees, and on a 5-year term, the fee-charging lender at 9% interest with a 5% fee actually produces a lower total repayment cost. The loan-term interaction is real, and the math shifts depending on the specific numbers involved.

This is why comparing total repayment cost in dollars, not monthly payment and not stated interest rate, is the correct method. Most loan calculators allow you to enter loan amount, interest rate, and term to get a total interest figure. Add the origination fee (if any) to that total to find the true all-in cost.

What to Watch Out For

Monthly payment comparisons are the most common trap. A 7-year loan at 11% with no fee will have a lower monthly payment than a 3-year loan at 9% with a 5% fee, but the total cost over 7 years will be dramatically higher. Lenders know that monthly payment is the number most borrowers anchor on, which is exactly why it is the wrong anchor. To understand how loan term length quietly drives total interest cost, the detailed breakdown at this guide to how loan term length controls how much interest you pay is worth reading before committing to any offer.

| Scenario | Loan A: 9% Rate + 5% Fee | Loan B: 11% Rate + No Fee | Loan C: 13% Rate + No Fee |

|---|---|---|---|

| Loan Amount | $15,000 | $15,000 | $15,000 |

| Origination Fee | $750 (5%) | $0 | $0 |

| Proceeds Received | $14,250 | $15,000 | $15,000 |

| 3-Year Total Cost | $17,389 | $17,563 | $18,523 |

| 5-Year Total Cost | $18,988 | $19,633 | $21,361 |

| Effective APR | ~11.7% | 11.0% | 13.0% |

| Better Deal at 3 Years? | No | Yes | No |

| Better Deal at 5 Years? | No | Yes | No |

The table above illustrates why a no-fee loan at a moderately higher rate (11%) still wins over a fee-bearing loan at 9% across both time horizons in this example, but a no-fee loan priced at 13% loses badly on a 5-year term. The rate differential matters as much as the fee presence or absence.

Use a loan amortization calculator to input the exact loan amount, rate, and term from each offer, then add any origination fee to the total interest figure. Compare these all-in dollar costs, not APRs alone. This single habit eliminates most of the confusion borrowers bring to the fee vs. no-fee question.

Step 5: When is a no-origination-fee loan actually the better financial choice?

A no-origination-fee loan is genuinely the better deal in specific, identifiable situations, and the worse deal in others. The distinction comes down to loan size, repayment term, and the rate differential between your competing offers.

Scenarios Where No-Fee Wins

Short loan terms favor fee elimination. On a 12- to 24-month loan, interest has limited time to accumulate, so the upfront fee represents a larger fraction of total borrowing cost. Avoiding a 5% fee on a $20,000 one-year loan saves $1,000 immediately, while a slightly higher interest rate over 12 months has little room to compound into an equivalent cost.

Large loan amounts amplify the advantage. On a $50,000 home improvement loan, a 5% origination fee costs $2,500 before you pay a dollar of interest. If a no-fee lender offers a rate only 0.5 to 1 percentage point higher, the fee savings easily exceed the extra interest over most loan terms. The break-even point shifts based on term length, but the fee savings are substantial and immediate.

Borrowers who are confident they will repay early benefit disproportionately from avoiding origination fees. If you plan to pay off a 5-year loan in 2 years, the interest portion of your total cost shrinks, but the origination fee you already paid does not. That fee becomes a higher share of your actual cost the earlier you pay off. Check first that the no-fee lender does not impose prepayment penalties, which would eliminate this advantage entirely.

Scenarios Where Paying a Fee Can Be the Smarter Move

Long repayment terms reverse the calculus. On a 6- or 7-year loan, a no-fee lender’s rate that is 2 percentage points higher than a fee-charging competitor’s rate will generate more additional interest than the fee cost. Run the numbers for your specific term before defaulting to the no-fee option.

SoFi offers an instructive real-world example of a false binary. The platform gives borrowers the option to voluntarily pay an origination fee in exchange for a lower interest rate. For borrowers who need the full repayment term, paying that optional fee and receiving a rate reduction can produce a lower total cost than the no-fee version of the same loan. This model makes clear that the fee-versus-no-fee framing is increasingly artificial: what actually matters is total repayment cost given your actual timeline.

Step 6: What are the tradeoffs of AI-driven underwriting on no-fee digital platforms?

Several leading no-fee digital lenders, including LightStream and SoFi, use automated, machine-learning-based underwriting that can process and approve an application in minutes. This efficiency is part of what makes the no-fee model financially viable for lenders, lower processing costs reduce the need to recoup expenses through upfront fees.

The Speed-and-Access Tradeoff

Automated underwriting delivers real benefits: fast decisions, consistent application of criteria, and in some cases better rates than a loan officer’s subjective assessment would produce. For borrowers with strong, clean credit files, algorithmic underwriting is generally favorable.

The tradeoff is transparency. When an algorithm declines your application, you often receive a limited, templated explanation. There is no loan officer to call, no committee to appeal to, and no way to provide context that the model did not capture from your credit file or income documentation. The Consumer Financial Protection Bureau has flagged fairness and transparency concerns with algorithmic underwriting in the fintech lending market, noting that borrowers have limited recourse when automated systems produce adverse outcomes. This is a real tradeoff consumers accept when they choose a streamlined digital platform.

On the other side of the market, AI-driven platforms that do charge origination fees have used algorithmic underwriting to expand access to near-prime borrowers who traditional credit scoring would reject. Upstart has published data claiming its model generates 41% more approvals and 33% lower rates than traditional credit-score-only models. For a borrower with a 620 FICO score who qualifies for an Upstart loan at 18% with a 5% origination fee but cannot qualify for a LightStream no-fee loan at all, the fee-bearing approval is obviously the better deal, because it is the only deal available. Approval has value, and that value can exceed the cost of the fee.

For gig workers, seasonal workers, and others with non-traditional income histories, this AI underwriting dimension matters acutely. The platforms most likely to approve these borrowers often charge origination fees. See how digital lending works for gig workers navigating income gaps for a detailed look at which platforms evaluate non-traditional income most favorably.

What to Watch Out For

Do not confuse “automated” with “unbiased.” Algorithmic models trained on historical lending data can encode the same structural inequalities present in that historical data. The CFPB’s ongoing scrutiny of AI-based credit decisions is not incidental, it reflects documented patterns of disparate outcomes across demographic groups that are not explained by creditworthiness alone. If a digital lender declines your application without a meaningful explanation, you have the right under the Equal Credit Opportunity Act to request specific reasons in writing.

Some fee-charging AI platforms like Upstart partner with banks and credit unions rather than lending their own capital. This means their underwriting technology is the product, not the loan itself. That model creates different incentives than a direct lender and can result in a wider range of rate and fee structures depending on which partner institution is actually funding your loan.

Step 7: How do I shop no-origination-fee digital lenders without getting fooled by hidden fees?

Effective comparison shopping for no-fee digital lenders requires a specific sequence of steps that most borrowers skip. The goal is to generate real, comparable offers before any hard inquiry hits your credit report, then audit each offer for fees that are not labeled as such.

How to Do This

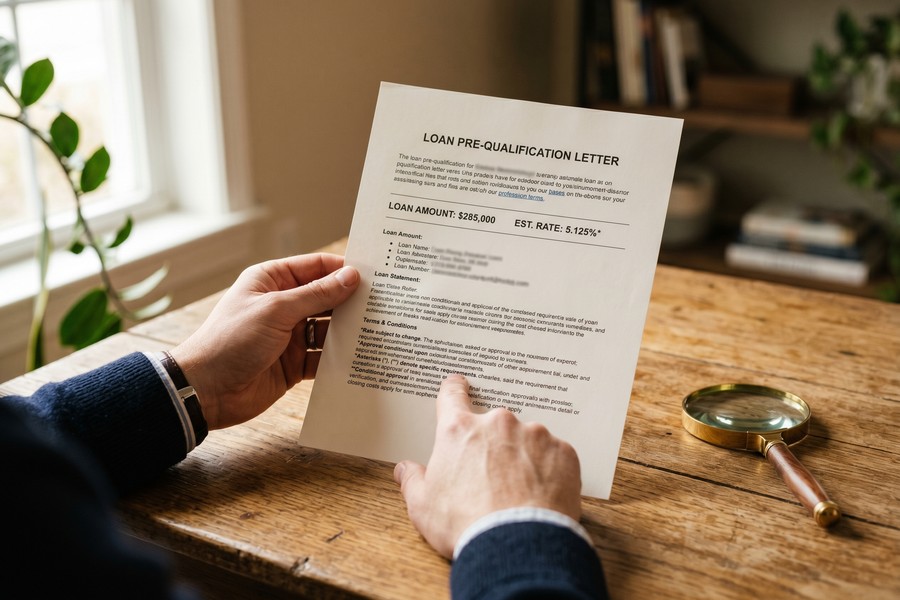

Start with soft-pull pre-qualification. Most major digital lenders, including SoFi, LightStream, Discover, PenFed, and LendingClub, allow you to check your estimated rate and terms without a hard credit inquiry. Pre-qualify with at least three lenders to generate a real comparison set. Use the same loan amount and term across all three so the quotes are directly comparable.

After collecting offers, compare total repayment cost in dollars, not monthly payment and not APR alone. Add any origination fee to the total interest charge from a loan calculator. The resulting number is your all-in borrowing cost for each option.

Then run the hidden-fee audit. Open the loan agreement or pre-qualification disclosure and search specifically for: “administrative fee,” “application fee,” “processing fee,” “financing fee,” and “documentation fee.” If any of these appear with a dollar amount or percentage, the loan is not truly fee-free. Confirm this by checking that the APR matches the stated interest rate exactly. Any gap between those two numbers indicates a fee is present, regardless of what it is called.

Check for prepayment penalties before signing. Some no-fee lenders compensate for the waived origination revenue by charging a penalty if you pay off the loan ahead of schedule. For borrowers planning to pay early, a prepayment penalty can eliminate every dollar of savings the no-fee structure offered. Treat the presence of a prepayment penalty as a disqualifying factor if early payoff is part of your plan.

If you are evaluating refinancing an existing loan, the same framework applies. The question of whether to refinance a personal loan with a no-fee lender versus staying with your current lender is covered in detail at this guide to fintech refinancing options, which addresses when the math favors a switch and when the costs of moving outweigh the savings.

What to Watch Out For

Pre-qualification rates are estimates, not guarantees. Your final approved rate may differ from the pre-qualification offer if your full credit file, income verification, or debt-to-income ratio reveals information the soft pull did not capture. Treat pre-qual numbers as directional comparisons, not binding commitments.

When you are ready to formally apply, limit hard inquiries by submitting all applications within a 14-day window. Credit scoring models from FICO and VantageScore treat multiple loan inquiries within a short window as a single inquiry for rate-shopping purposes, protecting your credit score while you compare final offers side by side.

Frequently Asked Questions

Is a no origination fee loan always cheaper than one with a fee?

No. A no-origination-fee loan is cheaper only when the lender’s interest rate does not exceed the fee-charging lender’s rate by enough to offset the fee savings over your loan term. On short-term loans (12 to 24 months), no-fee loans almost always win. On longer terms (5 to 7 years), a materially higher rate on the no-fee loan can cost more in total interest than the origination fee would have. The only reliable comparison is total repayment cost in dollars, calculated using the actual loan term you plan to use.

What credit score do I need to get a personal loan with no origination fee?

Most no-origination-fee digital lenders require at least a 670 FICO score, and top-tier lenders like LightStream prefer 740 or higher. As Experian explains, lenders waiving fees are targeting low-risk borrowers they are confident will repay, so the underwriting bar is higher. Borrowers with fair credit (580 to 669) will typically find that lenders willing to approve them do charge origination fees, making the no-fee comparison largely inaccessible.

How do I know if a lender is hiding fees under a different name?

The most reliable check is to compare the loan’s APR against its stated interest rate. If those numbers match exactly, the loan carries no fees. If the APR is higher than the interest rate, a fee exists, regardless of what it is called. The FDIC confirms that Regulation Z requires all finance charges to be accurately reflected in the APR. Common disguised fee names include “administrative fee,” “processing fee,” “financing fee,” and “documentation fee.”

Should I pay an optional origination fee to get a lower interest rate on my loan?

It depends on how long you plan to keep the loan. Paying an optional fee (as SoFi and a few other platforms offer) in exchange for a rate reduction makes financial sense only when the interest savings over your full loan term exceed the upfront fee cost. Run the math: multiply the rate reduction by your loan balance and term to estimate interest savings, then compare that to the fee dollar amount. If you plan to pay off early, the calculation changes, the shorter your actual payoff timeline, the less the rate reduction saves you.

Can I get a no-fee personal loan with a 600 credit score?

In most cases, no. The primary no-origination-fee digital lenders set minimum score requirements at 670 or higher. Borrowers with a 600 FICO score are more likely to qualify with platforms that use AI-expanded underwriting, such as Upstart or LendingClub, which may approve near-prime borrowers but typically charge origination fees of 5% to 10%. Credit unions with existing membership relationships sometimes offer more flexibility on fees, so checking a local or online credit union is worth doing before concluding a fee is unavoidable.

What is the best way to compare personal loan offers when some have fees and some don’t?

Pre-qualify with at least three lenders using the same loan amount and term, then calculate the total repayment cost (total interest plus any origination fee) for each offer. Do not compare monthly payments, which obscure term-length differences, and do not compare stated interest rates, which ignore fees. APR is the standardized metric, but total dollar cost over your actual repayment timeline is the most useful number for a direct comparison.

Do no-fee digital lenders approve loans as fast as fee-charging ones?

Generally yes. Leading no-fee digital lenders like LightStream and SoFi use automated underwriting that can produce decisions within minutes and fund loans within one to three business days. For same-day or next-day funding scenarios specifically, the key variables are the time of application submission and your bank’s processing speed, not whether a fee is involved. A detailed comparison of funding speed across platforms is available at this guide to same-day digital loans vs. next-day funding.

Are credit union personal loans a better option than no-fee digital lenders?

For many borrowers, yes. Credit unions averaged 10.64% APR on three-year personal loans in Q4 2025, per NCUA data, and many charge no origination fees. The limitation is membership eligibility and a less streamlined digital application experience. If you qualify for a credit union and your loan need is not urgent, comparing a credit union offer alongside fintech quotes is almost always worth doing.

What happens if I get declined by a no-fee digital lender, what are my alternatives?

A decline from a no-fee lender does not mean you cannot borrow. Fee-charging platforms with AI-driven underwriting, such as Upstart or LendingClub, have broader approval criteria and may qualify you even with a lower credit score or thin credit file. Credit unions and community banks are also worth approaching. Before reapplying anywhere, request the specific reason for the decline, you are legally entitled to this under the Equal Credit Opportunity Act, and address any correctable factors such as a high debt-to-income ratio before submitting another application. Understanding what drives your fintech loan limit and how lenders set it can help you identify what to improve before your next attempt.

Sources

- Consumer Financial Protection Bureau, Do Personal Installment Loans Have Fees?

- Federal Trade Commission, Truth in Lending Act

- National Credit Union Administration, Truth in Lending Act / Regulation Z Compliance Guide

- Experian, How to Get a Personal Loan With No Origination Fee

- Federal Deposit Insurance Corporation, Consumer Compliance Examination Manual: Truth in Lending Act

- Bankrate, Why Do Personal Loan Lenders Still Charge Origination Fees? (TransUnion Data)

- Experian, What’s a Good Interest Rate for a Personal Loan? (Federal Reserve Data)

- NerdWallet, Average Personal Loan Interest Rates (NCUA Data)