Fact-checked by the CapitalLendingNews editorial team

The Verdict

Overtime and bonus income can help you qualify for a larger mortgage, but most lenders require a 2-year documented history before counting it toward your qualifying income. It typically affects your loan size and debt-to-income ratio more than your interest rate itself. Skip relying on it if your overtime has dropped more than 20% year-over-year or started within the last 12 months.

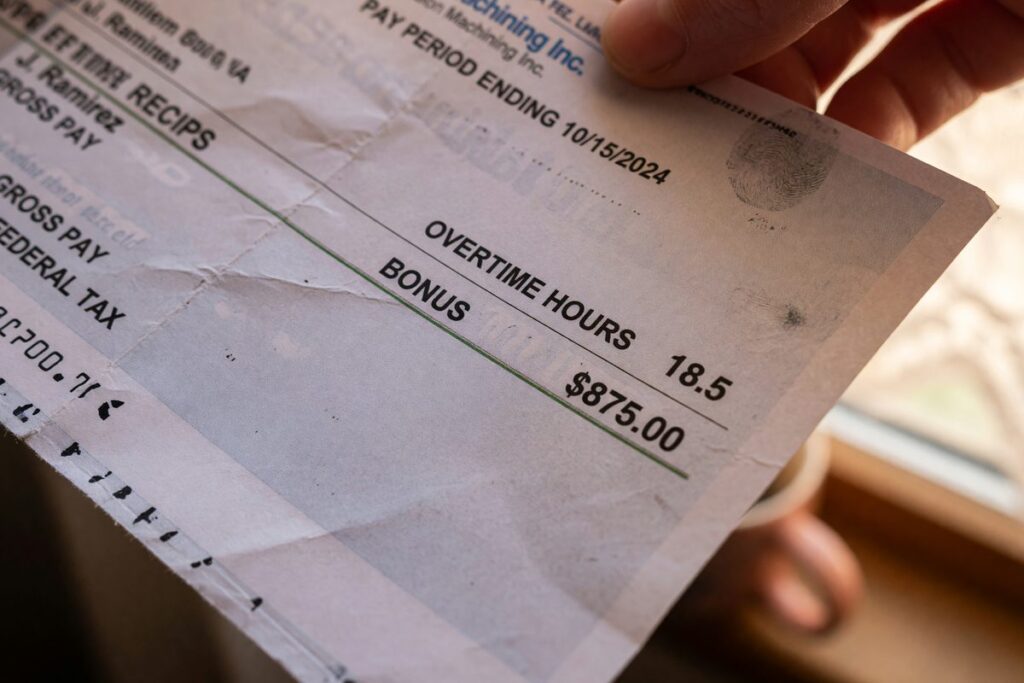

A nurse earning $72,000 in base salary plus $18,000 in overtime has a very different mortgage file than her pay stub suggests at first glance. Whether that $18,000 gets counted at all depends on rules set by Fannie Mae, Freddie Mac, the FHA, and the VA, and the treatment directly shapes your qualifying loan amount, your debt-to-income ratio (DTI), and, indirectly, your overtime income mortgage rate. The Consumer Financial Protection Bureau (CFPB) sets the baseline standard through Appendix Q to Regulation Z: overtime and bonus pay must have been received for at least two years, and documentation must show it is likely to continue before a lender can use it in qualifying calculations.

As of mid-2026, mortgage rates remain sensitive to borrower risk profiles, and an underwriter’s decision to include or exclude variable income can shift a debt-to-income ratio by several percentage points. That shift can move a borrower from a standard rate tier into a higher-risk pricing bracket, or push them out of approval entirely.

| Factor | Reasons to Count Overtime / Bonus Income | Reasons Not to Rely on It |

|---|---|---|

| History length | 2-year consistent record meets Fannie Mae, FHA, and VA standards | Anything under 12 months is almost universally excluded |

| Income trend | Stable or increasing overtime strengthens your DTI calculation | A 20%+ year-over-year decline triggers FHA’s current-year-only rule |

| Loan amount impact | Averaged overtime can add meaningful borrowing power; $18,000/year adds $1,500/month to qualifying income | It cannot offset a weak base salary below program minimums |

| Employer documentation | A written employer letter confirming continuation satisfies most lender overlays | VA loans often exclude overtime entirely if the employer won’t confirm future availability |

| Rate impact | Counting overtime can lower your DTI, which may qualify you for better pricing tiers | Higher DTI from excluded income can push you into a risk-adjusted rate add-on |

| Source of overtime | Overtime from a primary employer is most credible and easiest to document | Seasonal or second-job overtime faces heavier scrutiny and frequent exclusion |

Key Takeaways

- Your overtime or bonus history spans at least 24 months with the same employer or in the same field

- Your year-over-year overtime earnings have not dropped more than 20% from the prior year

- You can provide W-2s for the past two years plus a current paystub showing year-to-date overtime figures

- Your employer is willing to confirm in writing that overtime is expected to continue

- Counting the averaged overtime brings your debt-to-income ratio below 43%, the common threshold for conventional loan approval

- Your overtime comes from your primary employer rather than a second job or a seasonal arrangement that began within the last year

- Even without the full two years, you have at least 12 months of overtime documented and strong compensating factors such as a FICO Score above 720

Why Lenders View Overtime and Bonus Pay as Riskier Than Base Salary

Variable pay can disappear. That is the core concern underwriters carry into every file that includes overtime or bonus income. Base salary is contractual; overtime and bonuses depend on employer discretion, scheduling, and economic conditions that neither the borrower nor the lender controls.

That risk shows up directly in how lenders calculate your debt-to-income ratio. If an underwriter excludes your overtime, your qualifying income drops to base salary alone, your DTI rises, and you either qualify for a smaller loan or get priced into a higher rate tier. According to the CFPB’s guidance on DTI, most conventional programs treat 43% as a meaningful ceiling for qualified mortgage status. At a 45% DTI, many conventional lenders apply a loan-level pricing adjustment (LLPA) that adds to your rate. At 50% DTI, several conventional programs stop approving altogether. For borrowers whose base salary alone puts them near those thresholds, the treatment of overtime becomes the deciding variable in what rate they are offered, not just whether they can close.

Overtime from a second job or a seasonal arrangement gets even harder scrutiny. Lenders look at whether the overtime is tied to your primary employer, where continuation is at least plausible, or to a separate, unrelated position where hours could be cut without any notice to you. That distinction matters more than many borrowers realize when they are building their application. It is also worth reading about why strong savings balances alone don’t always produce better rate quotes; the dynamics of how lenders tier risk are often counterintuitive.

The 2-Year Rule: When It Applies and When Lenders Bend It

Two years of documented overtime is the standard, but it is not always the floor. Fannie Mae’s Selling Guide B3-3.3-02 states that while a minimum two-year history is recommended for bonus, commission, overtime, and tip income, a shorter period of at least 12 months is acceptable when positive offsetting factors reasonably compensate for the reduced documentation. Those factors typically include a high FICO Score, significant reserves, a low base-salary DTI, or long tenure with the employer.

Freddie Mac’s Section 5303.1 takes a similar position, requiring at least 12 months of income history to determine stable monthly income for fluctuating earnings including overtime and tips. Freddie’s guidelines add a specific focus on trends: if income has been declining after a peak year, underwriters are directed to use the lower stabilized figure or exclude it entirely rather than average in the high year.

FHA follows the two-year preference but adds its own wrinkle. If overtime income has declined by more than 20% from one year to the next, FHA requires lenders to use only the current-year income, not the two-year average, when calculating qualifying income. This is the rule most applicants do not know about until an underwriter flags it. For a borrower whose overtime peaked two years ago and has since tapered, that single rule can meaningfully shrink the income figure the lender uses. The full framework appears in the FHA Single Family Housing Policy Handbook 4000.1, published by the U.S. Department of Housing and Urban Development (HUD).

How Lenders Actually Calculate Your Overtime Income

The math is more forgiving than it sounds, if your numbers are consistent. The standard approach: add your total overtime earnings across 24 months, divide by 24, and add that monthly figure to your base salary for DTI purposes. A borrower who earned $14,000 in overtime in year one and $18,000 in year two has a $32,000 two-year total, or roughly $1,333 per month of qualifying overtime income.

Year-to-date paystubs complicate this when the application comes midyear. If you have 18 months of documented history and the YTD figure is on pace with prior years, many lenders will annualize the YTD amount and average it with the prior full year. If the YTD is trending lower, underwriters may use only the YTD annualized figure, or, under declining-trend reasoning, apply an even more conservative number. Lenders such as Chase and Wells Fargo typically layer their own overlays on top of agency minimums, so the effective threshold at a given institution can be stricter than what Fannie Mae or Freddie Mac technically permit.

Bonus income follows the same formula. The key difference is that lenders often treat a single large annual bonus more skeptically than steady weekly or biweekly overtime, because a bonus can be eliminated with a policy change while overtime tends to reflect structural scheduling. Borrowers who rely on a year-end bonus for a significant share of their income face a stricter documentation path, and should expect questions about whether the bonus is discretionary or tied to a defined performance metric. This is structurally similar to challenges faced by self-employed borrowers dealing with non-standard income patterns, where the averaging calculation can obscure a genuine income picture.

FHA vs. Conventional vs. VA: The Treatment Differences That Actually Matter

The program type changes the outcome significantly, and borrowers shopping rates across loan types should understand the differences before assuming their overtime will be counted the same way by every lender.

Conventional Loans (Fannie Mae and Freddie Mac)

Both agencies allow a 12-month history with compensating factors, and both emphasize trend analysis. Fannie Mae’s guidance is explicit that a declining earnings trend should lead the underwriter to use a lower, stabilized income figure rather than the full average. Fannie also specifies documentation requirements: either a completed Form 1005 (Verification of Employment) or two years of W-2s plus a current paystub, alongside a verbal verification of employment. Freddie Mac’s approach is nearly parallel, with Section 5303.1 adding emphasis on employer confirmation of the likelihood that the income continues. Lenders like Rocket Mortgage and SoFi that sell loans into the secondary market must conform to these agency standards, which limits how much latitude their underwriters can exercise.

FHA Loans

The FHA’s most distinctive rule is the 20% decline trigger. If your overtime in the most recent year was more than 20% below the prior year, the lender must use only the current-year figure, regardless of what the two-year average would produce. That is a concrete, mechanical rule, not underwriter discretion. FHA also allows a one-year history under specific circumstances, making it somewhat more flexible for newer overtime earners than some lender summaries suggest, but the declining-income rule is a hard constraint that eliminates the benefit of averaging. The Federal Housing Administration, which operates under HUD, backs these loans precisely because they are designed for borrowers with thinner profiles, but the income rules reflect that the agency is still managing default risk on a large portfolio.

VA Loans

VA guidelines take the most conservative approach to variable income by requiring explicit employer confirmation that overtime is expected to continue. If an employer is unwilling or unable to provide that confirmation, which happens frequently in shift-based industries, the income is excluded from qualifying calculations entirely. The VA Home Loan Guaranty program’s lender guidelines direct underwriters to assess whether the overtime is genuinely part of the borrower’s regular earnings pattern or the result of temporary conditions such as staff shortages. This is the program where overtime income disappears from the file most often, and borrowers applying for VA loans should discuss employer documentation well before submitting an application. If you are also comparing loan types for a first purchase, the analysis in our piece on fixed vs. adjustable rate mortgages for starter homes covers how program choice intersects with rate structure.

Who Should and Who Should Not

Good candidates

Borrowers who have steady, documented overtime from a primary employer and can show two years of consistent earnings are in the strongest position to have that income count in full.

- A police officer or firefighter with mandatory overtime shifts for at least 24 months, who can document each year with W-2s and a department letter confirming continued scheduling

- A manufacturing employee whose overtime has been stable or increasing for two years and whose employer will complete a verification of employment form

- A borrower with a FICO Score above 720 and less than 12 months of overtime, applying for a conventional loan where compensating factors allow a 12-month exception under Fannie Mae guidelines

- A nurse or healthcare worker in a unionized system where overtime is contractually scheduled and the employer can confirm its continuation in writing

Who should skip it

Certain income situations make it more trouble than it is worth to try to include overtime in the qualifying file.

- A borrower whose overtime earnings dropped more than 20% last year; FHA’s current-year rule will reduce the qualifying figure, and conventional lenders will likely apply the same conservative logic

- A gig worker or seasonal employee whose overtime comes from a second employer with no written commitment to continued hours

- A VA borrower whose employer HR department will not issue a written confirmation that overtime is expected to continue

- Anyone who started earning overtime fewer than 12 months ago, regardless of how large the income is; virtually no program will count it

Frequently Asked Questions

Does overtime income affect my mortgage interest rate directly?

Not directly, but the connection is real. Overtime income affects your debt-to-income ratio, and your DTI directly influences whether you qualify for standard pricing or trigger a loan-level pricing adjustment (LLPA). A higher DTI caused by excluded overtime can push you into a higher rate tier with conventional lenders, so the indirect effect on your rate is meaningful. The CFPB explains how DTI feeds into mortgage qualification and why lenders treat it as a primary risk signal alongside your FICO Score and loan-to-value ratio (LTV).

What if my overtime started 14 months ago, will lenders count it?

Possibly, under conventional guidelines. Fannie Mae allows a minimum of 12 months of history when positive compensating factors are present, such as a strong credit score or low base-salary DTI. Freddie Mac’s Section 5303.1 similarly accepts 12 months for fluctuating income. FHA and VA programs are less consistent on this point, and individual lender overlays at institutions like Bank of America or U.S. Bank may require the full two years regardless.

How do lenders verify that overtime will continue?

Most lenders require a verbal or written verification of employment, and many ask the employer to confirm that the overtime is expected to continue. VA loans have the strictest documentation requirement on continuation. A signed employer letter is the most reliable way to satisfy this requirement across all programs, though not all employers will provide one. The Federal Reserve’s interest rate environment also matters here indirectly: when rates are elevated, lenders tighten overlays, and documentation standards that were loosely enforced in a low-rate market tend to be applied more strictly.

Is bonus income treated the same as overtime for mortgage qualification?

The same two-year history rule and averaging method apply to both, but bonus income often gets more scrutiny because it can be discretionary. Lenders will ask whether the bonus is tied to a defined performance metric or is entirely at the employer’s discretion. Discretionary bonuses are more likely to be discounted or excluded, particularly if they are inconsistent year to year. The income calculation process is the same, but the underwriter’s willingness to credit it fully can differ. Experian notes in its mortgage qualification guidance that lenders assess not just income level but income stability, and a bonus that varies by 40% annually raises questions that steady overtime does not.

Sources

- Consumer Financial Protection Bureau, Appendix Q to Regulation Z: Standards for Determining Monthly Debt and Income

- Fannie Mae Selling Guide, B3-3.3-02: Bonus, Commission, Overtime, and Tip Income

- Freddie Mac Single-Family Seller/Servicer Guide, Section 5303.1: Fluctuating Employment Earnings

- U.S. Department of Housing and Urban Development, FHA Single Family Housing Policy Handbook 4000.1

- U.S. Department of Veterans Affairs, VA Home Loan Guaranty: Lender and Veteran Guidelines

- Consumer Financial Protection Bureau, What Is a Debt-to-Income Ratio?

- Federal Reserve, Selected Interest Rates (H.15 Statistical Release)