Fact-checked by the CapitalLendingNews editorial team

Quick Answer

Part-time income does not directly change the interest rate a lender quotes you. Rates are driven primarily by credit score, loan-to-value ratio, and market conditions. Where part-time earnings matter is indirectly: stable, documented part-time income lowers your debt-to-income (DTI) ratio, which can move you into a better rate tier, but only if the income meets verification standards, typically 12–24 months of uninterrupted history.

A borrower with a 720 credit score and a part-time retail job can expect the same base rate quote as a borrower with identical credit and no part-time work. The part-time income label itself does not trigger a rate penalty or a rate reward. What changes is the DTI calculation, and that is where the part-time income loan rate connection actually lives. According to CFPB regulations under the Equal Credit Opportunity Act, lenders are legally prohibited from discounting income simply because it comes from part-time employment.

With personal loan rates averaging well above 20% APR for borrowers with thin or high-DTI profiles, even a modest improvement in qualifying income can shift which rate tier you access. That shift is worth understanding before you apply.

Key Takeaways

- Part-time income does not directly affect your interest rate; it works through your DTI, with below-36% DTI qualifying for the best available pricing tiers, per CFPB Regulation B guidance.

- Crossing from a 43% DTI to a 36% DTI tier with verified part-time income can reduce a mortgage rate by 25–50 basis points, potentially saving tens of thousands of dollars over a 30-year term.

- Conventional loans typically require 12 months of uninterrupted part-time employment history; FHA loans effectively require 24 months before the income is treated as a reliable qualifier, according to HUD’s FHA Single Family Housing Policy Handbook.

- Borrowers with credit scores above 740 and down payments exceeding 20% are already in the best available pricing tier, so adding verified part-time income typically produces no further rate benefit.

- For personal loans and auto financing, APRs are governed primarily by credit score, not DTI thresholds, so part-time income usually affects qualifying loan amounts rather than the rate itself.

- Part-time income started fewer than 12 months before application is typically excluded from DTI calculations entirely, leaving your rate unchanged, per CFPB Regulation B interpretations.

Does Part-Time Income Directly Change Your Offered Interest Rate?

No, part-time income by itself does not move the rate a lender quotes. Lenders set interest rates using a risk-based pricing model built primarily around credit score, loan-to-value ratio, and current market benchmarks like the Prime Rate or SOFR. Your income source, part-time, full-time, self-employed, is not a standalone pricing variable in that model.

The indirect pathway runs through DTI. When a lender verifies your part-time earnings as stable and ongoing, those dollars count toward your total qualifying income. A higher qualifying income reduces your DTI, and a lower DTI can push you across a threshold into a better rate tier. Think of it as a two-step process: income verification first, DTI improvement second, and only then a potential rate benefit.

One honest concession worth flagging: if your credit score is already above 740 and your down payment exceeds 20%, adding verified part-time income may have negligible pricing benefit. You are already accessing the best available tier. The income still matters for loan amount qualification, but it will not squeeze another basis point off your quoted rate. This is the scenario most competitors fail to mention when writing about part-time income loan rate outcomes.

For borrowers in the middle of the credit spectrum, scores in the 660–719 range, verifiable part-time income can genuinely matter for pricing, because their rate tiers are wider and the DTI threshold between tiers is more consequential.

Key Takeaway: Part-time income does not directly set your rate, but it lowers DTI when verified, and a lower DTI can move you into a better rate tier. Borrowers with scores above 740 and 20%+ down payments often see no pricing benefit, per CFPB income evaluation guidance.

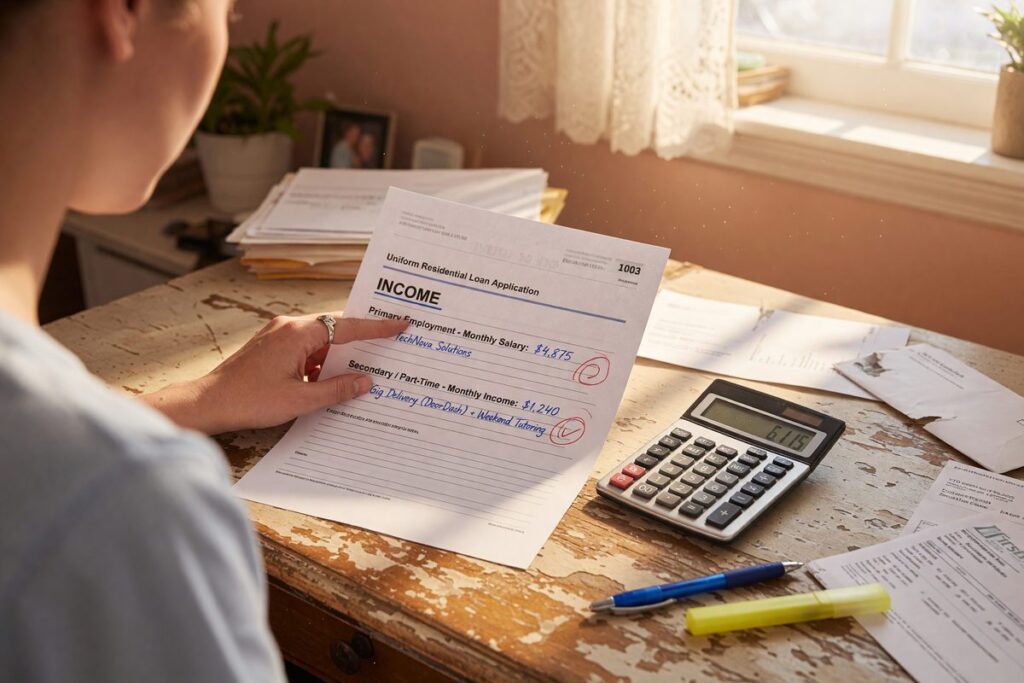

How Lenders Verify and Include Part-Time Income

Documentation requirements differ by loan type, and getting this wrong before you apply is a common and costly mistake. For conventional loans backed by Fannie Mae or Freddie Mac, lenders typically require a 12-month history of uninterrupted part-time employment. FHA loans are stricter: the CFPB’s Regulation Z commentary notes that part-time income received for less than two years may only be included if the lender documents it as likely to continue, meaning a two-year track record is effectively the safe harbor.

What Lenders Actually Ask For

Standard documentation includes recent pay stubs covering at least 30 days, W-2s for the prior two tax years, and a Verification of Employment (VOE) from the part-time employer confirming current status and expected continuation. When hours fluctuate week to week, underwriters typically average the income over 12 or 24 months using tax returns rather than annualizing a recent pay stub. That averaging method can hurt borrowers who ramped up hours recently and hurt them significantly.

Fixed part-time schedules, say, 20 guaranteed hours per week at a set hourly rate, are treated more favorably than variable-hour gig arrangements. Fintech lenders using payroll data are beginning to make exceptions for platform-based income, analyzing transaction consistency rather than employer letters, but traditional mortgage underwriting has not caught up to that model.

Automated Underwriting vs. Manual Review

Most applications run through Fannie Mae’s Desktop Underwriter (DU) or Freddie Mac’s Loan Product Advisor (LPA). These automated underwriting systems price risk on verified qualifying income only. Income that does not meet the documentation threshold is excluded from the DTI calculation, leaving the borrower’s rate unchanged from what it would have been without any part-time work listed. Manual underwriting can make exceptions, but manual files take longer and some lenders charge a slightly higher rate for the additional review risk.

Key Takeaway: Conventional loans may accept 12 months of part-time history; FHA loans effectively require 24 months. Variable-hour gig income is averaged over prior tax years by automated underwriting systems, which often produces a lower qualifying figure than a recent pay stub suggests. See how seasonal and irregular income affects loan qualification for a related breakdown.

The Real Link: DTI Ratio, Risk Pricing, and Rate Tiers

| DTI Range | Rate Tier Impact | Part-Time Income Needed |

|---|---|---|

| Below 36% | Best available tier, lowest risk pricing | Helps if income moves you under this threshold |

| 36%–43% | Standard approval, moderate pricing | Verified income can shift you into the tier above |

| 44%–49% | Compensating factors required, higher rate | Part-time income critical; must be fully documented |

| 50%+ | Decline or specialist lender required | Part-time income alone rarely sufficient |

A DTI at or below 36% is where mainstream lenders offer their most competitive pricing. Cross that line with verified part-time income and the rate improvement can be material. For a $300,000 mortgage, moving from a 43% DTI pricing tier to a 36% DTI tier might represent a rate difference of 25 to 50 basis points depending on the lender, translating to tens of thousands of dollars over a 30-year term. As loan term length quietly magnifies every rate difference, even a quarter-point matters over a long payoff period.

Lender overlays add another layer. Even when Fannie Mae’s DU approves a file, individual lenders apply their own overlays, internal rules that can restrict DTI ceilings or require higher reserves. A borrower whose verified part-time income drops DTI to 43% might be approved at lender A but face a higher-rate program at lender B with a 41% overlay cap. Shopping multiple lenders is not optional advice here; it is the mechanism through which part-time income borrowers find their actual best rate.

A creditor shall not discount or exclude from consideration the income of an applicant because the income is derived from part-time employment; a creditor may consider the amount and probable continuance of any income in evaluating an applicant’s creditworthiness.

Key Takeaway: Crossing the 36% DTI threshold with verified part-time income can reduce your mortgage rate by 25–50 basis points, depending on the lender and loan product. Lender overlays vary, so understanding how DTI affects digital lending approvals can reveal which platform treats your income most favorably.

When Part-Time Income Has Little or No Effect on Your Rate

Several specific situations render part-time income irrelevant to your pricing. Short job tenure tops the list. If you started a part-time position fewer than 12 months ago, most conventional lenders will exclude it from the DTI calculation entirely, meaning the income appears on your application but contributes nothing to the qualifying figures that drive rate decisions.

Seasonal work has its own rules. Income from a job with clear off-seasons may be averaged across a full year, producing a much lower monthly figure than the peak-season pay stubs suggest. A tax preparer working 3 months per year cannot use those earnings at their seasonal rate; the annual average becomes the qualifying number. For a full picture of how seasonal earning patterns affect loan access, the challenges facing gig workers during income gaps follow the same underwriting logic.

Career mismatch also raises flags. If the part-time job is unrelated to your primary occupation, a software engineer driving rideshare on weekends, for example, some underwriters treat continuance as less certain. The CFPB’s guidance under Regulation B requires individual evaluation of actual circumstances rather than statistical generalizations, but that does not prevent a lender from noting field discontinuity as a documentation concern.

Finally, declining hours trigger scrutiny. If W-2s show you earned more from part-time work two years ago than last year, an underwriter may trend the income downward or exclude it on continuance grounds. Document an upward or stable trajectory wherever possible before submitting.

Key Takeaway: Part-time income started fewer than 12 months before application is typically excluded from DTI calculations, and declining-hour patterns can further reduce what lenders count. Per CFPB Regulation B interpretations, lenders must assess each applicant’s actual circumstances individually rather than applying blanket exclusions.

Personal Loans, Auto Financing, and Credit Cards: A Different Standard

Non-mortgage lenders operate with far simpler income verification, and that changes the part-time income loan rate equation considerably. For unsecured personal loans, most lenders, including major platforms like LendingClub, Upstart, and SoFi, verify income by asking for recent pay stubs or bank statements rather than conducting the full two-year documentation drill mortgage underwriters require. Part-time income counts if it shows up consistently.

Where the rate link breaks down in personal lending is precision. Personal loan APRs are driven almost entirely by credit score and the lender’s own risk model. Income affects whether you qualify for a certain loan amount, but moving from a $35,000 annual income to a $44,000 annual income by adding part-time earnings rarely shifts the APR quote by a meaningful margin. The rate tier thresholds in unsecured lending are credit-score gates, not DTI gates.

Auto financing sits between the two worlds. Lenders verify income to confirm you can service the monthly payment, a basic debt-service coverage check, but the rate is predominantly set by credit score and the loan-to-value on the vehicle. Part-time income makes approval more likely for a larger loan amount; it does not reliably lower the interest rate on a given loan. For borrowers considering more complex situations, the dynamics of co-borrower credit mismatches on joint loan rates follow a similar pattern, where one variable rarely overrides the dominant pricing factor.

Key Takeaway: Personal loan and auto loan APRs are governed primarily by credit score, not DTI thresholds. Part-time income helps establish qualifying loan amounts but rarely shifts the interest rate itself, a distinction that matters when comparing loan types and understanding where your documentation effort pays off.

Frequently Asked Questions

Can a lender legally ignore my part-time income when reviewing my application?

No. Under the Equal Credit Opportunity Act (ECOA) and CFPB rules implementing it, lenders cannot discount or refuse to consider income because it comes from part-time employment. They can, and must, evaluate its stability and likelihood of continuation, but the income source alone cannot be used as a basis for exclusion.

How long do I need to have a part-time job before it counts toward my mortgage application?

Conventional loans typically require 12 months of uninterrupted history; FHA loans effectively require 24 months to treat the income as a reliable qualifier. Income from a part-time job started less than 12 months ago will likely be excluded from your DTI calculation, leaving your qualifying income and potential rate unchanged.

Will adding part-time income lower my mortgage interest rate?

It can, indirectly. Verified part-time income lowers your DTI, and crossing a key DTI threshold, particularly the 36% mark, can move you into a better rate tier. The benefit disappears if your credit score is already above 740 and your down payment exceeds 20%, because you are likely already in the best available pricing tier.

Does gig work or platform income count the same as a traditional part-time job?

Not always. Traditional W-2 part-time income with a consistent schedule is easier to verify and count. Platform income from apps like DoorDash or Uber is typically documented through tax returns (Schedule C), averaged over two years, and may be reduced further by business expenses. Some fintech lenders now use payroll data connections that treat consistent platform deposits more favorably than conventional mortgage underwriting does.

Does part-time income affect my personal loan rate differently than my mortgage rate?

Yes. Personal loan APRs are set almost entirely by credit score, so part-time income primarily affects how large a loan you can qualify for, not the rate itself. Mortgage rates are more sensitive to DTI thresholds, making verified part-time income a more meaningful pricing lever in that context.

What documents should I gather before applying with part-time income on the application?

Collect two years of W-2s or tax returns, at least 30 days of current pay stubs, and a Verification of Employment letter from your part-time employer confirming current hours and expected continuation. If your hours vary, showing a stable or upward trend across those two years is more important than any single recent pay stub.

Sources

- Consumer Financial Protection Bureau, Can a Lender Consider Where My Income Comes From?

- Consumer Financial Protection Bureau, Regulation Z: Part-Time and Seasonal Income Documentation

- Consumer Financial Protection Bureau, Regulation B, Section 1002.6: Individual Evaluation of Income

- Consumer Financial Protection Bureau, Regulation B, Section 1002.6: Rules Concerning Evaluation of Applications

- U.S. Department of Housing and Urban Development, FHA Single Family Housing Policy Handbook 4000.1

- Federal Reserve, Selected Interest Rates (H.15 Statistical Release)