Fact-checked by the CapitalLendingNews editorial team

The Verdict

Avoiding mortgage rate negotiation mistakes on a second mortgage is worth the effort when you collect at least four competing Loan Estimates and use your existing equity as leverage. It is not worth rushing if your combined debt-to-income ratio exceeds 43%, because no amount of shopping fixes an underwriting disqualifier. Fix the profile first, then negotiate.

A repeat homebuyer walking into a second mortgage negotiation with the same playbook they used for their first home is starting at a real disadvantage. Second liens carry rate premiums of 0.25% to 0.75% above primary residence mortgages in the current market, and lenders price that risk in before you say a word. The most common mortgage rate negotiation mistakes repeat buyers make are not rookie errors, they are experienced-buyer assumptions that no longer apply. According to a 2024 LendingTree survey, 54% of homebuyers with a mortgage only received one loan offer, leaving a substantial portion of potential savings on the table.

In December 2024, with rates still elevated and second-mortgage underwriting tighter than it was three years ago, the cost of these mistakes is higher than ever. Knowing which errors to sidestep before you apply can mean the difference between a rate you negotiate down and one you simply accept.

| Factor | Reasons to Negotiate Aggressively | Reasons to Pause First |

|---|---|---|

| Rate premium | Second liens price 0.25–0.75% above primaries; more negotiation room exists | If your credit score is below 700, shopping won’t offset underwriting adjustments |

| Quote volume | 45% of shoppers who got multiple quotes received a lower offer than their first (LendingTree 2024) | Hard credit pulls from 5+ lenders in 30 days can ding your score briefly |

| Equity leverage | Proven equity and payment history give repeat buyers loyalty discounts unavailable to first-timers | Combined LTV above 80% eliminates most rate discounts regardless of history |

| Lender type | Credit unions and portfolio lenders often price second liens below large banks | Specialty lenders may charge higher origination fees that erode rate savings |

| Points strategy | Buying down rate makes sense when break-even is under 3 years | The CFPB found 87.4% of cash-out refi borrowers paid points in 2023, many without calculating break-even |

| DTI position | Combined DTI under 36% gives you real negotiating credibility with lenders | DTI above 43% makes rate negotiation secondary to debt paydown |

Key Takeaways

- Your combined loan-to-value ratio is below 80%, giving lenders less risk to price into your rate

- You have collected at least four Loan Estimates from different lender types (bank, credit union, online specialist, portfolio lender)

- Your combined DTI, first mortgage plus second mortgage payment, stays at or below 43%

- You have at least 12 months of on-time payment history on your existing first mortgage to use as loyalty leverage

- Your credit score is 740 or above, the threshold where most lenders offer best-tier second-mortgage pricing

- You have compared the full APR, not just the interest rate, across all Loan Estimates for the second lien

- You are prepared to walk away if a lender’s match offer raises fees to offset the rate reduction

Do Second Mortgages Actually Have More Negotiation Room?

Yes, and by a meaningful amount. Because second liens sit behind the primary mortgage in the event of default, lenders assign them a risk premium that is built directly into the rate quote. That premium creates space for negotiation that simply does not exist to the same degree on a primary purchase loan.

The typical adjustment runs 0.25% to 0.75% above what the same borrower would receive on a primary residence mortgage. On a $200,000 second mortgage at 7.5% versus 7.0%, the monthly payment difference is roughly $67, about $804 per year. Over five years that is over $4,000 in additional interest before principal reduction is considered. When you put a number like that next to the time it takes to collect four competing quotes, the math justifies the effort.

Buyers with strong primary-residence histories sometimes assume that earns an automatic discount. Some lenders do offer loyalty pricing, but only when you ask, and only when you can demonstrate it with documentation. The lender holding your first mortgage has already priced in your credit quality once. They are not going to volunteer a discount on the second unless you give them a reason to: a competing offer, verifiable equity, or a clean combined DTI. Understanding how repeat homebuyers can leverage equity to negotiate a lower mortgage rate is the foundation the rest of these mistakes build on.

Mistake #1: Shopping Only One Type of Lender

Most repeat buyers go back to the bank that handled their first mortgage, and that is often the highest-rate option in the room. Large national banks price second liens for volume and consistency, not for your specific equity position. Credit unions, regional portfolio lenders, and online second-lien specialists frequently quote 0.25% to 0.50% lower on identical loan profiles because their cost structures and risk appetites differ.

A Fannie Mae study found that 36% of 2021 homebuyers received only one mortgage quote. For second mortgages, that single-quote habit is even more costly because the rate spread across lender types is wider than on conforming primary purchases. Your first-mortgage bank may offer a loyalty discount, but loyalty discounts are rarely as large as the discount a competing lender will quote to win your business from scratch.

The practical fix: treat your existing lender as one of four to five quotes, not as a starting point you negotiate from. Get quotes from at least one credit union you qualify to join, one portfolio lender (a bank that holds loans on its own books rather than selling to the secondary market), and one online second-lien specialist. Then bring the lowest Loan Estimate back to your existing lender. That sequence produces results that shopping your bank first and hoping for a discount rarely achieves.

One honest caveat here: this strategy demands time and organization. Gathering four to five quotes, tracking fee variations, and following up with competing lenders over a compressed window is real work. For borrowers whose schedules don’t allow a focused two-week effort, the process often stalls after two quotes, which is still better than one but leaves money on the table. If you’re not prepared to see it through, a mortgage broker who shops multiple lenders simultaneously may produce better results than a half-finished DIY comparison.

“If your lender says ‘if you find a better deal, bring it back and I’ll match it,’ just dump that lender now. There are honest lenders that offer you their lowest upfront and that’s really what you want. You don’t want someone where you have to play carnival tricks in order to get a decent deal.”

Mistake #2: Watching the Rate and Missing the Total Cost

A lower interest rate on a second mortgage can cost more than a higher one. That sentence is worth reading twice. On smaller second liens, origination fees and points represent a larger percentage of the loan amount than they would on a $500,000 primary. A lender who offers 6.75% with $4,000 in fees may be more expensive over a five-year horizon than one offering 7.0% with $800 in fees, depending entirely on how long you hold the loan.

The Consumer Financial Protection Bureau reported that 60.7% of home purchase borrowers paid discount points in 2023. The problem is not paying points, it is paying them without calculating the break-even period. If you plan to sell or refinance within three years, points almost never recover their cost. On a second mortgage with a break-even of 48 months, paying 1 point upfront to shave 0.25% off a $150,000 balance costs $1,500 and saves roughly $375 per year, meaning you need four years just to recover the fee.

The Consumer Financial Protection Bureau’s Loan Estimate form (standardized under RESPA) requires lenders to disclose the full APR, not just the note rate. Comparing APR across all Loan Estimates is the single fastest way to expose a low-rate-high-fee offer for what it is. Understanding how loan term length quietly controls how much interest you actually pay extends this same logic to second-mortgage term selection.

One more thing to verify: lender fee worksheets sometimes contain errors that borrowers assume will be corrected automatically. Ask for any corrections in writing before you proceed, and do not rely on verbal assurances that figures will sort themselves out at closing.

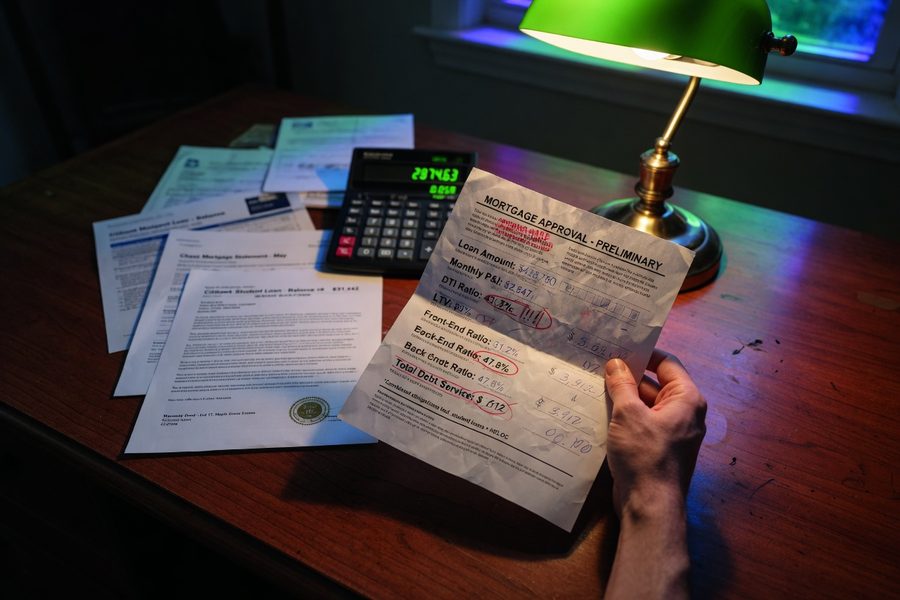

Mistake #3: Ignoring Your Combined Debt-to-Income Ratio

Combined DTI is the number that quietly determines whether rate negotiation is even relevant. Lenders pricing second mortgages stack your proposed second-lien payment on top of your existing first-mortgage payment, then divide the total by gross monthly income. A borrower with a 740 credit score and a combined DTI of 47% will receive worse pricing than a borrower with a 710 score and a combined DTI of 35%, in most second-mortgage underwriting frameworks.

This catches experienced buyers off guard more often than it should. The primary mortgage was approved years ago, income has grown, and there’s a natural assumption that the underwriting will reflect that progress. But lenders recalculate everything from scratch for a second lien. Car payments, a business line of credit, or other installment debt added since the first mortgage closed all raise combined DTI and push the second-mortgage rate upward. The debt-to-income ratio is the number that quietly kills applications on second mortgages just as often as it does on other credit products.

The threshold that matters: most second-mortgage lenders price their best rates for borrowers with combined DTI at or below 36%. At 43%, you are at the outer edge of qualified-mortgage territory, and some lenders exit the competitive pricing tier entirely at that point. Paying down revolving balances before applying, even a few thousand dollars on a credit card, can shift combined DTI enough to move you into a better pricing band. Check your credit report at AnnualCreditReport.com before any second-mortgage application, because errors on your file affect both the rate quote you receive and your DTI calculation if any debt is misreported.

If you are purchasing with a co-borrower, be aware that the weaker credit profile typically drives second-mortgage underwriting. The dynamics of how co-borrowers with mismatched credit scores affect the interest rate on a joint loan apply directly to second-mortgage applications.

Who Should and Who Should Not

Good candidates

Repeat buyers with equity, clean payment history, and DTI room are well-positioned to negotiate second-mortgage rates effectively.

- Borrowers with at least 20% equity in the primary home and a combined LTV below 80% on the proposed second, giving lenders less risk to price in

- Repeat buyers with 24+ months of on-time primary mortgage payments, which creates a documentable loyalty case with existing lenders

- Borrowers with credit scores of 740 or above and combined DTI under 36%, which qualifies them for best-tier pricing across most lender types

- Buyers purchasing a second property in a market with multiple competing portfolio lenders or credit unions, where quote variation tends to be widest

- Borrowers who plan to hold the second mortgage for five or more years, making rate reduction efforts and break-even calculations on points worthwhile

Who should skip it

Some repeat buyers are better served fixing their financial profile before opening any negotiation.

- Borrowers with combined DTI above 43%, where even the most competitive rate quote will face underwriting pushback

- Buyers whose combined LTV exceeds 80%, eliminating most risk-based rate discounts regardless of credit strength

- Repeat buyers with recent late payments on their primary mortgage, which removes loyalty leverage entirely and signals elevated risk to second-lien underwriters

- Borrowers planning to sell or refinance within two years, where closing costs on a negotiated second mortgage rarely recover before exit

Frequently Asked Questions

How many quotes should I get for a second mortgage?

Get at least four Loan Estimates from different lender types: one large bank, one credit union, one portfolio lender, and one online specialist. According to a 2024 LendingTree survey, 45% of mortgage shoppers who compared offers received a lower rate than their first quote. On a second lien, where rate premiums are already elevated, that difference compounds quickly.

Does shopping for a second mortgage hurt my credit score?

Multiple mortgage inquiries within a 14- to 45-day window (depending on the scoring model used) are typically treated as a single inquiry by FICO and VantageScore. The short-term dip from rate shopping is generally small, often fewer than five points, and recovers within a few months. Spreading applications over several weeks instead of a concentrated window increases the impact, so be efficient.

Can I use my first mortgage payment history to negotiate a lower rate on a second?

Yes, but you have to make the case explicitly. Your existing lender can see your payment history internally, but other lenders need documentation. Bring 12 to 24 months of mortgage statements showing on-time payments and present them alongside competing quotes. Buyers who document their loyalty position alongside a competing offer give lenders a concrete reason to reduce fees or shave rate.

Is it worth paying discount points on a second mortgage?

Only if your break-even period is shorter than how long you plan to hold the loan. The CFPB found that 58.7% of home purchase borrowers paid discount points in the first three quarters of 2023, but many do so without calculating the payback window. On a $150,000 second at 7.25%, paying one point ($1,500) to drop to 7.0% saves about $31 per month, a break-even of roughly 49 months. If you might sell or refinance within four years, keep the cash. For deeper analysis of whether rate buydowns make sense in the current market, see whether buying down your mortgage rate with points is worth it when home prices are still high.

What is the biggest mistake repeat buyers make when negotiating second-mortgage rates?

Focusing on the interest rate and ignoring total loan cost. On second mortgages, which are often smaller than primary loans, origination fees and points represent a larger share of the balance. A lender offering 0.25% lower but charging $3,000 more in fees will cost more than a higher-rate competitor over any holding period under four to five years. Always compare the full APR disclosed on the standardized Loan Estimate, not the note rate alone.

Sources

- Consumer Financial Protection Bureau, Data Spotlight: Trends in Discount Points Amid Rising Interest Rates

- LendingTree, Mortgage Shopping Around Survey (2024)

- Fannie Mae, Homebuyers Who Shop Around for Mortgages

- CNBC Select, How to Negotiate Mortgage Rates

- Consumer Financial Protection Bureau, What Is a Loan Estimate?

- Federal Reserve, Selected Interest Rates (H.15 Release)