Fact-checked by the CapitalLendingNews editorial team

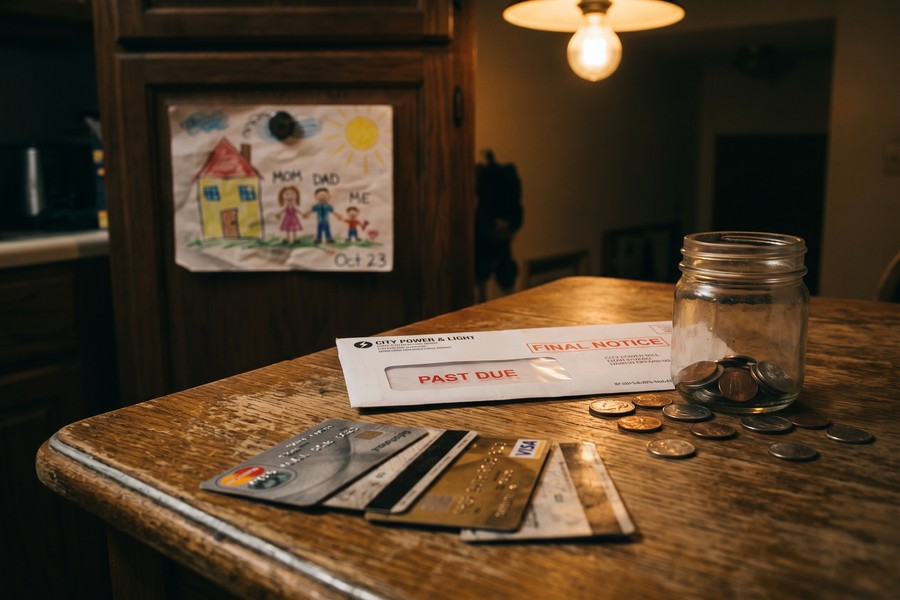

Single parents know the feeling well: it’s the 22nd of the month, the grocery bill just hit $280, the car needs an oil change, and there’s a field trip permission slip asking for $15 sitting on the kitchen counter. Budgeting for single parents is a daily act of survival, creativity, and sheer willpower. According to the U.S. Census Bureau, there are approximately 15.4 million single-parent households in the United States, and the vast majority are operating on one income in a two-income economy.

The numbers behind single-parent financial stress are stark. Pew Research Center data shows that single mothers earn a median annual income of just $26,000, compared to $40,000 for single fathers and $84,000 for married couples with children. Meanwhile, the USDA estimates that raising a child from birth to age 17 costs an average of $310,605, and that figure doesn’t account for inflation or college. Childcare alone can consume 30% to 40% of a single parent’s take-home pay in high-cost states, according to the U.S. Department of Labor. The result is a financial tightrope where one unexpected expense can trigger a debt spiral.

This guide is built for single parents who are determined to make their money work harder, without adding more debt to the pile. You’ll find concrete, tested strategies for cutting fixed and variable expenses, stacking public and private assistance programs, optimizing a bare-bones budget, and protecting your financial future even on a limited income. Every tactic here is grounded in real data and designed for households where every dollar is already spoken for.

Key Takeaways

- Single mothers earn a median of $26,000 per year, roughly 31% of what a dual-income household with children earns.

- Childcare costs average $10,000–$20,000 per year per child, and can consume up to 40% of a single parent’s income in expensive metro areas.

- The federal Child Tax Credit provides up to $2,000 per qualifying child, with up to $1,600 refundable, a critical cash injection for single-parent tax filers.

- Households that build even a $500 emergency fund are significantly less likely to take on high-interest debt after an unexpected expense, according to research from the Consumer Financial Protection Bureau.

- Single parents who use written budgets, even simple zero-based ones, report saving an average of $200–$400 more per month than those who track spending mentally.

- Federal and state assistance programs (SNAP, CHIP, LIHEAP, WIC) remain drastically underutilized, an estimated 20% of eligible families do not claim all benefits they qualify for.

In This Guide

- The Financial Reality of Single-Parent Households

- Budgeting Frameworks That Actually Fit Single-Parent Life

- Attacking Fixed Costs Without Disrupting Stability

- Slashing the Grocery Bill Without Sacrificing Nutrition

- Stacking Public Assistance and Benefit Programs

- Managing the Childcare Budget

- Building an Emergency Buffer on a Tight Income

- Low-Disruption Ways to Increase Income

- Managing Existing Debt Without Adding New Debt

- Protecting Your Financial Future as a Single Parent

The Financial Reality of Single-Parent Households

Single-parent households face a structural financial disadvantage that no amount of budgeting discipline can fully eliminate, but understanding its dimensions is the first step to working around it. The income gap is the most visible problem. One paycheck must cover rent, food, transportation, childcare, healthcare, clothing, and every emergency that life throws at a family.

What’s less visible is the time tax single parents pay. Without a partner to share administrative tasks, comparing insurance rates, clipping coupons, cooking from scratch, single parents often default to costlier shortcuts. Takeout instead of cooking. Full-price instead of comparison shopping. These micro-decisions add up to hundreds of dollars per month.

The Income-to-Expense Ratio Problem

The core challenge is mathematical. A single parent earning $36,000 a year takes home roughly $2,800 per month after taxes. The average two-bedroom apartment in the U.S. now rents for over $1,400 per month, according to Zillow’s 2024 rental market data. Add $600 in childcare, $350 in groceries, $300 in transportation, and $200 in utilities, and that parent is already at $2,850 before healthcare, clothing, or anything unexpected.

The result is a budget that starts in deficit. That’s not a character flaw, it’s an arithmetic problem that requires systemic solutions, not just willpower.

Single mothers head approximately 80% of all single-parent households in the U.S. Their median household income of $26,000 is 57% below the national median household income of $60,580, according to U.S. Census Bureau data.

Why Debt Becomes a Default Coping Strategy

When income doesn’t cover expenses, credit cards and personal loans become a pressure valve. The Federal Reserve reports that households earning under $40,000 annually carry an average credit card balance of $3,800, and single-parent households are disproportionately represented in that group. Interest on that balance at a 24% APR costs roughly $75 per month in finance charges alone.

This guide focuses on breaking that cycle, not through debt consolidation loans, but through expense reduction and resource stacking that doesn’t require borrowing. If you’re already managing existing debt, our article on debt avalanche vs. debt snowball methods provides a structured comparison of payoff strategies.

Budgeting Frameworks That Actually Fit Single-Parent Life

Generic budgeting advice often assumes predictable income, consistent expenses, and the mental bandwidth to track every transaction. Single parents frequently have none of these. The right budgeting framework is one that’s simple enough to maintain during the chaos of solo parenting and flexible enough to absorb the unexpected.

A honest caveat worth stating: no budgeting system fixes a structural income shortfall. If your expenses genuinely exceed what one income can cover in your area, a framework alone won’t close that gap. The strategies in this guide work best when paired with benefit enrollment and, where possible, some form of income supplementation. For parents whose budget deficit runs $500 or more per month, the assistance programs section may deliver more immediate relief than any spreadsheet.

Zero-Based Budgeting for Constrained Incomes

Zero-based budgeting (ZBB) assigns every dollar of income a specific job, spending category, savings, or debt payment, until the balance reaches zero. It’s particularly powerful for tight budgets because it forces a deliberate choice about every dollar rather than letting spending drift. A parent earning $2,800 per month would map every cent to a category before the month begins.

The clear advantage of ZBB: it makes immediately visible when expenses exceed income. That visibility is uncomfortable but productive, it creates urgency around cuts rather than letting overspending hide in the noise.

Use a free app like YNAB (You Need a Budget) or EveryDollar to implement zero-based budgeting digitally. Both offer mobile access, which matters when you’re managing finances in spare moments between pickups and bedtime routines. YNAB offers a 34-day free trial and a reduced rate for single-parent households that qualify as low-income.

The 50/30/20 Rule, Modified for Single Parents

The classic 50/30/20 rule (50% needs, 30% wants, 20% savings) is often unrealistic for single parents. When housing alone consumes 50% of income, there’s no room for wants or savings. A modified 70/10/20 split is more honest: 70% for essential needs, 10% for minimal discretionary spending, and 20% directed at savings and debt reduction, even if that 20% is only $200 per month to start.

The goal isn’t perfect adherence to a ratio. It’s creating a framework that prevents complete financial paralysis while still directing some money toward future security.

| Budget Framework | Best For | Income Range | Main Benefit |

|---|---|---|---|

| Zero-Based (ZBB) | Very tight budgets, irregular expenses | Under $35,000/yr | Maximum control over every dollar |

| Modified 70/10/20 | Moderate income with high fixed costs | $35,000–$55,000/yr | Realistic proportions for one-income families |

| Envelope Method | Cash spenders, overspending on variables | Any income level | Physical spending limits per category |

| Pay-Yourself-First | Parents who can save small amounts | $40,000+/yr | Automates savings before spending temptation |

Attacking Fixed Costs Without Disrupting Stability

Fixed costs, rent, insurance, utilities, subscriptions, are the hardest to cut but offer the biggest payoff when you succeed. A $150 reduction in monthly fixed costs saves $1,800 per year. That’s a car repair fund, a back-to-school wardrobe, or three months of emergency savings.

Housing: The Largest Line Item

Housing is typically the single largest expense for any family. Single parents who can reduce this one line item gain the most financial breathing room. Options worth exploring include co-housing arrangements, sharing a larger home with another single-parent family and splitting rent and utilities. This can cut housing costs by 30% to 50% while also providing built-in childcare support.

Subsidized housing programs through HUD’s Section 8 Housing Choice Voucher program can reduce rent to 30% of adjusted income for qualifying families. Wait lists are long in many cities, but applying now, even if placement is years away, is a smart move.

Insurance Audit

Single parents often pay for insurance coverage they no longer need. An annual insurance audit, reviewing auto, renters/homeowners, and life insurance policies, can uncover $50 to $300 in monthly savings. Shopping auto insurance quotes every 12 months is one of the highest-return financial activities a single parent can do. The average driver saves $700 per year by switching providers, according to the Insurance Information Institute.

Many utility companies offer low-income assistance programs beyond LIHEAP. Programs like “budget billing,” weatherization assistance, and appliance rebates can reduce monthly utility costs by $30–$80. Call your provider and specifically ask about every income-based discount available.

Subscription Audit: The Silent Budget Killer

The average American household pays for 4.5 streaming and subscription services, totaling $219 per month according to a 2024 J.D. Power study. Many single parents have subscriptions that were signed up for years ago and barely used. A monthly subscription audit, using your bank statement, not your memory, typically reveals $60–$120 in cuttable expenses.

Keep one streaming service. Cancel the gym membership you haven’t used since March. Drop the app subscriptions that auto-renewed. These small cuts compound quickly over a year.

| Fixed Cost Category | Average Monthly Cost | Potential Monthly Savings | Time to Implement |

|---|---|---|---|

| Auto Insurance | $167 | $40–$80 | 1–2 hours |

| Streaming/Subscriptions | $219 | $60–$140 | 30 minutes |

| Cell Phone Plan | $90 | $20–$50 | 1 hour |

| Utility Bill | $175 | $20–$80 | 1–3 hours |

| Housing (co-housing) | $1,400 | $300–$700 | Weeks to months |

Slashing the Grocery Bill Without Sacrificing Nutrition

Food is the most flexible major expense in a single-parent budget, and therefore the most important place to apply strategic effort. The average American spends $475 per month on food at home, according to Bureau of Labor Statistics data. Single parents feeding two or more people on that budget can succeed, but only with a deliberate system.

Meal Planning as a Financial Strategy

Meal planning is the single highest-impact grocery habit. Families who plan meals weekly spend 25% less on groceries and waste 30% less food than those who shop without a plan, according to research from the Natural Resources Defense Council. Planning four or five dinners per week based on what’s on sale, rather than what sounds good, can save $80–$120 per month immediately.

Batch cooking on Sunday evenings reduces both weeknight food spending and the temptation to order takeout when you’re exhausted at 7 p.m. One two-hour session can produce lunches and dinners for four to five days.

Store Strategy and Price Matching

Shopping at discount grocers like Aldi, Lidl, or WinCo instead of traditional supermarkets cuts the average grocery bill by 15%–30%. A family spending $400 per month at a discount grocer saves $60–$120 monthly compared to a name-brand chain. Store-brand substitutions on staples like pasta, canned goods, and dairy add another $30–$50 per month in savings.

Families enrolled in SNAP (Supplemental Nutrition Assistance Program) receive an average of $230 per month in food assistance. For a single parent with two children earning under $3,000/month, this benefit can cover nearly half the household grocery bill.

Apps like Flipp, Ibotta, and Fetch Rewards layer digital coupons and cash back on top of already-discounted prices. Users report saving an additional $20–$50 per month with minimal effort after the initial setup.

Stacking Public Assistance and Benefit Programs

One of the most consequential, and underused, strategies for budgeting for single parents is benefit stacking: identifying and claiming every public assistance program you qualify for. Research consistently shows that a significant portion of eligible families leave money on the table due to stigma, lack of awareness, or application complexity.

Federal Programs Every Single Parent Should Know

SNAP, WIC, Medicaid, CHIP, and LIHEAP are the major federal assistance programs available to low- and moderate-income single-parent households. Together, they can offset thousands of dollars in annual expenses. A family qualifying for all five programs may receive the equivalent of $6,000–$12,000 in annual purchasing power, without taking on a single dollar of debt.

According to the Center on Budget and Policy Priorities, many households earning just above the SNAP income threshold still qualify for overlapping programs: CHIP for the children, LIHEAP for utilities, and the Child Tax Credit. These benefits don’t cancel each other out, they stack, and failing to claim any one of them is money left permanently on the table.

The Child Tax Credit (CTC) alone is worth up to $2,000 per qualifying child, with up to $1,600 refundable as of the 2024 tax year. A single parent with two children could receive $3,200 back at tax time, money that can fund an emergency account or pay down high-interest debt.

| Program | Benefit Type | Average Annual Value | Income Limit (Family of 3) |

|---|---|---|---|

| SNAP | Food assistance | $2,760/yr | ~$32,000 gross |

| Medicaid/CHIP | Health coverage | $3,000–$8,000/yr | Varies by state |

| LIHEAP | Utility assistance | $400–$1,200/yr | ~$40,000 gross |

| WIC | Food/nutrition (young children) | $1,800/yr | ~$47,000 gross |

| Child Tax Credit | Tax refund | Up to $2,000/child | Under $200,000 single filer |

State-Level and Local Programs

Every state operates its own assistance programs on top of federal ones. Many counties have emergency utility funds, diaper banks, school supply programs, and free after-school care through local nonprofits. Calling 211, the national social services hotline, connects single parents to local resources within minutes.

Free tax preparation through the IRS Volunteer Income Tax Assistance (VITA) program ensures single parents claim every credit they’re owed. In 2023, VITA helped 3.1 million taxpayers receive $1.7 billion in refunds they may have otherwise missed.

Managing the Childcare Budget

Childcare is often the second-largest expense for single parents, and in many cities, it rivals rent. The average annual cost of childcare for one child ranges from $10,000 in rural areas to over $24,000 in cities like San Francisco and Boston, according to the Economic Policy Institute. For single parents, this is the budget line that most often triggers debt.

Subsidies, Sliding-Scale, and Co-Op Care

The federal Child Care and Development Fund (CCDF) provides subsidies to low-income families. Eligibility varies by state, but a family of three earning under $45,000 typically qualifies for partial or full subsidies. Many parents don’t apply because they assume they earn too much, but the income thresholds are higher than most expect.

Sliding-scale childcare centers adjust fees based on family income. Nonprofit and faith-based centers are more likely to offer this model than commercial chains. Calling five to ten centers and asking explicitly about sliding-scale fees takes two hours and can save $200–$600 per month.

The Child and Dependent Care Tax Credit allows single parents to claim up to 35% of childcare expenses, up to $3,000 for one child or $6,000 for two or more. At the $3,000 cap with a 35% credit rate, that’s $1,050 back at tax time. Many single parents leave this credit unclaimed.

Informal Care Networks

Childcare co-ops, informal networks of parents who trade childcare hours, can dramatically reduce costs. A network of four single parents, each contributing 10 hours per week of care, creates 30 hours of free childcare coverage per parent per week. This model requires trust and coordination, but it’s completely debt-free and builds genuine community support.

Family members providing childcare may also be paid through your Dependent Care FSA (if offered by your employer), allowing you to pay up to $5,000 in childcare expenses with pre-tax dollars, saving $750–$1,500 per year depending on your tax bracket.

Building an Emergency Buffer on a Tight Income

The absence of an emergency fund is the primary reason single parents take on debt. A $400 car repair or a $600 medical bill becomes a credit card charge when there’s no cash buffer. Research from the Consumer Financial Protection Bureau found that households with even $500 in emergency savings are significantly less likely to use high-cost credit products after a financial shock.

The $500 Starter Fund

The goal isn’t a three-month fund right away, it’s $500. That’s the threshold that prevents most common financial emergencies from becoming debt events. At $25 per week, it takes 20 weeks, five months, to get there. At $50 per week, you’re there in 10 weeks.

Automate this transfer on payday, before you’ve had a chance to spend the money on anything else. Most banks allow you to set up a scheduled transfer to a separate savings account for free. Putting the money in a separate account, even at the same bank, reduces the temptation to spend it.

Research from the Urban Institute supports the same conclusion: even a small liquid emergency reserve, $250 to $500, dramatically changes how families respond to financial shocks. The behavioral effect is real. Knowing the money exists reduces the panic that drives people toward payday lenders and high-fee borrowing.

Our detailed guide on building an emergency fund when you live paycheck to paycheck walks through specific tactics for families with very limited cash flow, including micro-saving strategies that work even when the budget feels completely full.

High-Yield Savings for Emergency Funds

Don’t park your emergency fund in a standard savings account earning 0.01% APY. Online high-yield savings accounts currently offer 4.5%–5.0% APY. On a $1,000 emergency fund, that’s $45–$50 per year in interest, not life-changing, but it’s money you weren’t earning before. More importantly, the slight friction of an online account (transfers take one to two business days) helps prevent impulse withdrawals.

Payday loans and “emergency” fintech lending apps charge APRs of 300%–600% or more. A $300 payday loan rolled over just twice can cost $150 in fees, 50% of the original loan amount. Before using any short-term lending product in a crisis, exhaust local emergency assistance funds through 211 first. If borrowing becomes necessary, compare options carefully, our guide on fintech loan apps vs. peer-to-peer lending platforms breaks down the real cost differences.

Low-Disruption Ways to Increase Income

Budgeting for single parents has a ceiling, you can only cut so much before you hit bone. At some point, the math requires more income. The challenge is that most single parents have almost no discretionary time. Income-boosting strategies must be low-overhead, flexible, and compatible with solo parenting schedules.

Skills-Based Side Income

Freelance work using existing professional skills is the most efficient income supplement. A single parent who works in accounting can do bookkeeping on nights or weekends through platforms like Upwork or Bench. A teacher can tutor online through Wyzant or Tutor.com. A nurse can pick up per-diem hospital shifts. The approach that works is one that draws on skills already in place, no retraining required.

Even 5–8 additional hours per week at $25–$50 per hour generates $500–$1,600 per month in supplemental income. That’s the difference between a budget that barely survives and one that starts building cushion.

Selling and Passive Income Channels

Selling unused household items on Facebook Marketplace or eBay is a one-time income boost that also declutters the home. The average household has $300–$700 in sellable items, according to OfferUp data. For a single parent, this is a tax-free financial injection that requires only a few hours.

More durable passive income options, renting a parking space, subletting a room, or selling digital products like lesson plans or templates, require upfront setup but generate recurring income with minimal ongoing effort. Even $100–$200 per month in passive income meaningfully changes the budget math over time.

The federal Earned Income Tax Credit (EITC) is one of the most powerful income supplements for single parents. A single parent with two children earning $24,000 per year can receive an EITC of up to $6,164. Yet the IRS estimates that 20% of eligible taxpayers fail to claim it each year.

Managing Existing Debt Without Adding New Debt

Most single parents arrive at the budgeting conversation already carrying some debt, credit cards, medical bills, personal loans, or student loans. The goal is to manage it strategically so it doesn’t consume the entire discretionary budget in interest payments.

Prioritizing by Interest Rate

The mathematically optimal debt payoff strategy is the debt avalanche method: paying minimum payments on all balances and directing every extra dollar toward the highest-interest debt first. This minimizes total interest paid over time. A single parent with $5,000 in credit card debt at 24% APR and $3,000 in a personal loan at 12% APR should attack the credit card first.

If motivation is a concern, the debt snowball method, paying off the smallest balance first, regardless of interest rate, provides psychological wins that help some people stay on track. Our side-by-side comparison of debt avalanche vs. debt snowball quantifies the cost difference so you can make an informed choice based on your situation.

Negotiating With Creditors

Medical debt, one of the most common debt categories for single parents, is far more negotiable than most people realize. Hospitals are required to offer charity care to qualifying patients, and even those above the eligibility threshold can often negotiate lump-sum settlements for 40%–60% of the original balance. Calling the billing department and asking for a hardship program is a two-phone-call effort that can save thousands.

Debt settlement companies charge 15%–25% of the enrolled debt as fees, often before they’ve resolved anything. Negotiating directly with creditors or working with a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC) is almost always a better option. NFCC counseling is free or low-cost.

If credit card interest is consuming your budget, a balance transfer to a 0% APR promotional card can freeze interest accumulation for 12–21 months. This restructures existing debt at zero cost, giving you time to pay down the principal. Check our analysis of common mistakes people make when paying off credit card debt before making a move.

Protecting Your Financial Future as a Single Parent

Survival mode is understandable, but even small investments in the future during lean years make a significant difference over time. The compounding power of early retirement contributions and insurance coverage creates security that no amount of future catch-up can fully replicate.

Retirement Contributions on a Tight Budget

Saving for retirement when you’re struggling to cover groceries can feel absurd, but even contributing $25–$50 per month to a Roth IRA during lean years preserves the compounding benefit of time. A $50 monthly contribution starting at age 30, earning 7% annually, grows to approximately $60,000 by age 65. That’s $21,000 contributed and $39,000 in growth, all from $50 per month.

If your employer offers a 401(k) match, contribute at minimum enough to capture the full match. An employer matching 50% of your 3% contribution gives you a 50% instant return on that money, no investment reliably beats that.

For a full comparison of retirement account options and their tax implications, our guide on Roth IRA vs. Traditional IRA walks through which account type saves more based on current vs. expected future income.

Life Insurance: The Non-Negotiable for Single Parents

Term life insurance is arguably more critical for single parents than any other demographic. You are your children’s entire financial support system. A 20-year, $500,000 term policy for a healthy 32-year-old single parent typically costs $25–$35 per month. That coverage ensures your children are financially protected even if you can’t be there. No other financial product provides this ratio of protection per premium dollar.

| Financial Priority | Monthly Investment | 10-Year Value | Why It Matters for Single Parents |

|---|---|---|---|

| Emergency Fund ($500) | $50/mo for 10 months | Prevents $3,000–$5,000 in debt | Eliminates need for emergency borrowing |

| Term Life Insurance | $25–$35/mo | $500,000 coverage | Protects children if sole earner dies |

| Roth IRA | $50/mo | ~$8,700 at 7% growth | Tax-free retirement income |

| Employer 401(k) Match | 3% of income | $6,000+ in free employer match | 50–100% instant return on contribution |

Real-World Example: Renata’s $800-Per-Month Turnaround

Renata, a 34-year-old single mother of two in Columbus, Ohio, was earning $38,000 per year as a medical billing specialist when she hit a wall in early 2023. Her take-home pay was $2,650 per month. After rent ($1,050), childcare ($820), groceries ($450), car payment ($280), utilities ($160), and her phone ($90), she had negative $200 before any discretionary spending. She was putting approximately $300 per month on credit cards just to bridge the gap.

Over six months, Renata made four major changes. First, she applied for, and received, a CCDF childcare subsidy that reduced her childcare cost from $820 to $340 per month. Second, she switched her car insurance provider after a 45-minute comparison shopping session and cut her premium from $190 to $120 per month. Third, she filed for the Child and Dependent Care Tax Credit and the EITC at tax time, receiving a $4,200 combined refund she hadn’t previously claimed. Fourth, she began meal planning with a weekly $90 grocery budget using Aldi and a Sunday batch-cooking routine, down from her previous $450.

By September 2023, Renata’s monthly budget had shifted dramatically. Childcare was $480 lower. Car insurance was $70 lower. Groceries were $360 lower. Her monthly cash flow swung from negative $200 to positive $610. She used the first three months of surplus to build a $500 emergency fund. She then began putting $100 per month toward her $3,800 credit card balance, on top of minimum payments, and $50 per month into a Roth IRA.

Within 18 months of starting, Renata had eliminated $2,900 of her credit card balance, accumulated $800 in emergency savings, and was no longer adding new debt each month. Her budget transformation was built entirely on benefit claiming, expense reduction, and system changes, not a single new loan.

Your Action Plan

-

Complete a full expense audit in the next 7 days

Pull your last two months of bank and credit card statements. Categorize every expense and total each category. Most single parents discover $100–$300 in completely invisible spending, subscriptions, unused memberships, forgotten auto-renewals, during this exercise alone.

-

Apply the zero-based budget to next month’s income today

Before the month begins, assign every dollar of expected income to a specific category. Use a free app like YNAB or EveryDollar, or a printed spreadsheet. The act of writing the budget creates accountability that mental tracking never does.

-

Check your eligibility for all five major federal assistance programs this week

Visit Benefits.gov or call 211 to screen your eligibility for SNAP, Medicaid/CHIP, WIC, LIHEAP, and CCDF childcare subsidies. Complete applications for every program you qualify for. Even partial benefits across two or three programs can equal $300–$600 per month in purchasing power.

-

Call your auto insurer and three competitors for new quotes

Dedicate 90 minutes this week to comparing auto insurance rates. Most people who do this save $50–$80 per month. Ask each provider about every available discount, safe driver, low mileage, good student (for your child), and multi-policy bundling.

-

Open a separate high-yield savings account and start a $25/week auto-transfer

Open a free high-yield savings account at a bank like Ally, Marcus, or SoFi. Set a recurring $25 weekly transfer for the day after payday. Don’t touch this account for anything except a true emergency. Your first goal is $500. Celebrate when you get there.

-

Implement one grocery strategy this month

Choose one approach: switch to a discount grocer for staples, implement weekly meal planning from a sale circular, or download Ibotta and Flipp before your next shopping trip. Do not try to implement all strategies at once. One consistent change saves more than three inconsistent ones.

-

File or amend your taxes to claim every credit you qualify for

If you haven’t claimed the EITC, Child Tax Credit, or Child and Dependent Care Credit, visit an IRS VITA site or use free tax software to file or amend your return. If you filed in the last three years without these credits, you can amend your return and receive the refund retroactively. This is often the largest single financial opportunity for single parents.

-

Get a term life insurance quote before the end of the month

Use an online broker like Policygenius or SelectQuote to get quotes on a 20-year term policy in 20 minutes. A $500,000 policy for a healthy non-smoker in their 30s typically costs $25–$35 per month. This is the one financial product where skipping is not an option for single parents.

Frequently Asked Questions

What is the most important first step in budgeting for single parents?

Start with an honest expense audit. You cannot create a realistic budget without knowing where your money is actually going. Pull two months of bank and credit card statements, categorize every transaction, and calculate your true monthly spending by category. Most single parents are surprised by what they find, the numbers are often more manageable than the mental version feels.

How much of my income should go toward housing as a single parent?

The traditional 30% housing guideline is often unachievable for single parents. If you’re spending 40%–50% of income on housing, the priority should be reducing that ratio, through co-housing, HUD subsidies, or relocating to a lower-cost area, rather than trying to squeeze savings from a budget where housing alone consumes half the income. Even a $200 monthly rent reduction creates $2,400 per year in breathing room.

Can I actually save money while earning under $35,000 a year as a single parent?

Yes, but the strategy shifts. At income levels under $35,000, the biggest financial gains come from benefit enrollment rather than pure savings. Claiming all eligible assistance programs (SNAP, CHIP, LIHEAP, childcare subsidies, EITC) can provide $5,000–$10,000 in annual value without touching your paycheck. That allows you to redirect your earned income more effectively, including toward a small emergency fund.

What’s the best way to handle unexpected expenses without going into debt?

A dedicated emergency fund is the most reliable protection. Even $500 covers the majority of common household emergencies, a car repair, a medical copay, an appliance failure. Beyond that, keeping a list of local emergency resources (211, community assistance funds, nonprofit emergency help programs) provides a second line of defense before reaching for a credit card.

Should I pay off debt or save first as a single parent?

Do both simultaneously, in small amounts. Build a $500 emergency fund first, this is the threshold that prevents new debt from forming. Then split your extra cash flow: put half toward high-interest debt and half toward growing the emergency fund to $1,000. Once you have $1,000 saved, direct all extra money toward the highest-interest debt until it’s paid off. This parallel approach avoids the trap of paying down debt aggressively only to charge it back up after the next emergency.

What childcare assistance programs are available for single parents?

The primary federal childcare assistance program is the Child Care and Development Fund (CCDF), which provides subsidies to low-income working families. Eligibility varies by state, but a family of three earning under $45,000 generally qualifies for at least partial subsidy. The Child and Dependent Care Tax Credit allows up to $3,000 per child in qualifying expenses at a credit rate of 20%–35%. Dependent Care FSAs allow up to $5,000 in pre-tax childcare payments through an employer plan.

How do I stop the cycle of using credit cards to cover monthly shortfalls?

Breaking the monthly credit card cycle requires either increasing income or decreasing expenses enough to create a genuine surplus. Start by identifying the two or three largest expense reductions available immediately, childcare subsidies, insurance comparison, subscription cancellations. Apply for any assistance programs you qualify for. Then use zero-based budgeting to ensure every dollar is allocated before it can be spent, which makes the shortfall visible rather than invisible. The goal is to manufacture even a $50–$100 monthly surplus as a starting point.

Is it worth making small retirement contributions when my budget is extremely tight?

Contributing even $25–$50 per month preserves the compounding benefit of time in a way that future catch-up contributions cannot fully replicate. The priority order should be: emergency fund first, then any employer match (it’s a 50–100% instant return), then Roth IRA contributions. If your employer offers a 401(k) with matching, contributing just enough to capture the full match is almost always the highest-return financial move available, at any income level.

What are the best free budgeting tools for single parents?

YNAB (You Need a Budget) is the most effective tool for zero-based budgeting, with a 34-day free trial and low-income scholarship options. EveryDollar offers a free tier suitable for basic budgeting. Mint (now Credit Karma’s budgeting tool) provides free automatic transaction categorization. For those who prefer simplicity, a Google Sheets budget template downloaded from the CFPB’s website costs nothing and requires no app installation.

How can I increase my income without paying more for childcare?

Look for income opportunities that align with your existing childcare schedule. Freelance work done during school hours or after bedtime eliminates childcare overhead entirely. Selling unused items on Facebook Marketplace or eBay requires no scheduled work time. Online tutoring through platforms like Tutor.com allows you to set your own schedule around your child’s hours. Some single parents arrange childcare swaps with another parent, enabling income-generating hours without added childcare cost.

Who is this budgeting approach NOT a good fit for?

These strategies work best when there’s at least some margin to work with, even $50 to $100 per month. If your housing cost alone exceeds your monthly take-home pay, or if you’re in active crisis (eviction, disconnected utilities, no food), the immediate priority is emergency assistance through 211 and local nonprofits, not a budget spreadsheet. This guide is designed for parents who are stretched but stable, not for households in acute financial emergency, where the calculus is different.