Everything You Need to Know About Embedded Finance and What It Means for Borrowers

The embedded finance market hit $138B in 2025 and is headed to $588B by 2030 — here's how faster credit access, contextual loans, and new privacy risks affect you.

The embedded finance market hit $138B in 2025 and is headed to $588B by 2030 — here's how faster credit access, contextual loans, and new privacy risks affect you.

Approval in as little as 24 hours and up to $100,000 — fintech platforms are giving the 18.6 million U.S. veteran homeowners faster options the VA loan system doesn't always cover.

Retirees with variable income see 38% higher approval rates on fintech platforms versus traditional banks, with closings in 11 days instead of 38.

Fintech lenders now set your rate in seconds using live data — strong borrowers may see 7.99%, while thin profiles can pay 10–15 points more. Here's how to prepare.

Fintech credit lines fund in 24 hours; factoring advances cash in 24–72 hours. Match your cash flow fix to the real problem: operating gaps or slow-paying customers.

Hard inquiries drop your score by fewer than 5 points, but soft inquiry pre-qualification costs nothing. Compare offers risk-free across lenders before submitting one application.

When your debt-to-income ratio exceeds 43%, digital platforms approve 63% more personal loans than banks. See which lender type actually works for your situation.

A $628 origination fee on a $7,500 digital loan cuts your actual payout before your first payment. Here's what lenders bury in the fine print.

Compare up to 5 lenders without denting your credit score using soft pull pre-qualification. Lock in estimates before committing to a hard pull.

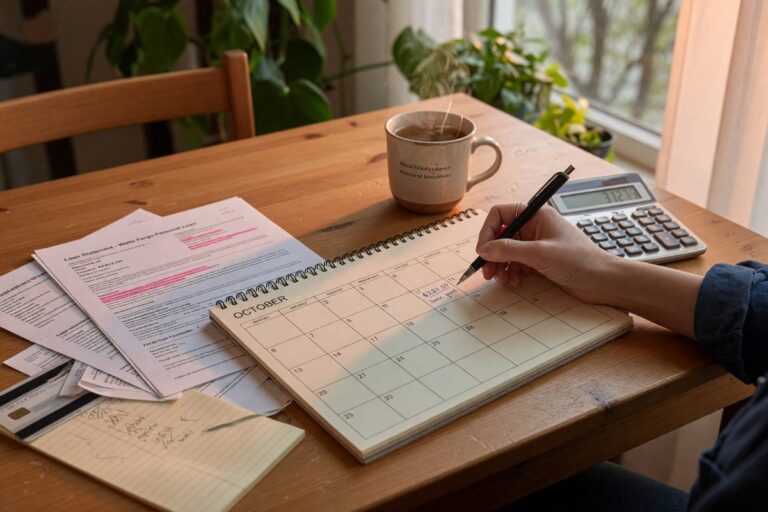

Staggered loan due dates cut missed-payment risk by 15–30%. Map your income calendar, request free due-date shifts, and stop multiple auto-drafts from draining your account.