Fact-checked by the CapitalLendingNews editorial team

Quick Answer

Builder offered mortgage rates often appear 0.5%–1.5% lower than market rates but come with hidden costs — inflated home prices, restricted closing cost credits, and captive lender lock-ins that can cost buyers $15,000–$40,000 more over the life of a loan. As of July 2025, always compare at least three outside lenders before accepting a builder’s financing package.

Builder offered mortgage rates are one of the most misunderstood financing tools in new construction real estate. In July 2025, many national homebuilders — including D.R. Horton, Lennar, and PulteGroup — are dangling below-market interest rates through their captive lending affiliates to close deals faster and protect their profit margins. According to the Consumer Financial Protection Bureau’s mortgage comparison guidelines, buyers who accept the first financing offer they receive routinely overpay tens of thousands of dollars across a 30-year term.

New construction sales have stayed elevated even as existing home inventory has tightened throughout 2024 and into 2025. Builders have responded by leaning harder into financing incentives — rate buydowns, closing cost credits, and “preferred lender” perks — to keep sales moving. These offers look generous on the surface but frequently obscure price inflation, watered-down incentive packages, and long-term cost traps that savvy buyers can avoid with the right preparation.

This guide is for first-time and repeat buyers under contract — or considering a contract — on a new construction home. After following these steps, you will be able to identify the real cost of a builder’s financing offer, negotiate from a position of strength, and protect yourself from the most common traps that catch buyers off guard at closing.

Key Takeaways

- Builder-affiliated lenders originated roughly 35% of new construction purchase loans in 2023, according to National Association of Home Builders research, giving builders enormous leverage over buyers who don’t shop around.

- Builders routinely mark up the base home price by $5,000–$20,000 to offset the cost of rate buydowns they advertise as “free” incentives, effectively transferring the buydown cost to the buyer through a higher purchase price.

- A 1% difference in mortgage rate on a $400,000 loan translates to approximately $240 per month and more than $86,000 in total interest over 30 years, according to standard amortization calculations.

- Federal law under RESPA (Real Estate Settlement Procedures Act) prohibits builders from legally requiring buyers to use their affiliated lender, though builders can — and do — tie incentives to preferred lender use.

- Buyers who obtained outside mortgage quotes saved an average of $1,500 in closing costs and secured better loan terms in a majority of cases, per CFPB mortgage shopping research.

- Temporary 2-1 buydown programs offered by builders reduce the rate by 2% in year one and 1% in year two, but the full market rate applies in year three — a payment shock many buyers are not prepared for.

In This Guide

- Step 1: How Do Builder Offered Mortgage Rates Actually Work?

- Step 2: What Are the Hidden Costs Buried in Builder Financing Offers?

- Step 3: How Do I Compare Builder Financing Against Outside Lenders?

- Step 4: Can I Negotiate Builder Incentives Without Using Their Lender?

- Step 5: Should I Accept a Builder’s Rate Buydown Program?

- Step 6: How Do I Protect Myself From Builder Financing Traps at Closing?

- Frequently Asked Questions

Step 1: How Do Builder Offered Mortgage Rates Actually Work?

Builder offered mortgage rates are subsidized interest rates provided by a builder’s affiliated mortgage company, funded by the builder’s marketing budget rather than any generosity toward the buyer. Builders like Lennar Mortgage, DHI Mortgage (D.R. Horton’s in-house lender), and Pulte Mortgage operate as captive lenders — profit centers designed to capture the mortgage transaction alongside the home sale.

How the Builder Rate Subsidy Works

When a builder advertises a rate below the current market — say, 5.99% when the going 30-year fixed rate is 7.25% — they are buying down that rate using money that could otherwise be applied as a straight price reduction or closing cost credit. The builder purchases mortgage discount points on your behalf from their affiliated lender, reducing your rate for the loan’s life or a temporary period.

The key insight is that this money comes from somewhere. In most cases, builders offset the cost of the rate subsidy by pricing the home higher, reducing upgrade allowances, or structuring the deal so that the incentive package disappears if you choose an outside lender. According to NAHB housing economics data, builder incentive packages averaged $32,000 per home in late 2023 — but the form of that incentive matters enormously for the buyer.

What to Watch Out For

Buyers often confuse the advertised rate with the effective cost of the loan. A lower rate does not automatically mean a lower total cost if the home’s base price has been inflated, the closing cost credits are reduced for outside lenders, or the rate applies only for a temporary buydown period. Always separate the rate from the total financing package before making any comparison.

Builder-affiliated mortgage companies are required by the Real Estate Settlement Procedures Act (RESPA) to disclose their affiliated business arrangement. You should receive an Affiliated Business Arrangement Disclosure — if you don’t, ask for it. This document reveals the financial relationship between the builder and the lender.

Step 2: What Are the Hidden Costs Buried in Builder Financing Offers?

The hidden costs in builder financing offers fall into four main categories: inflated home prices, restricted incentive packages, less favorable loan terms, and limited negotiating leverage — any one of which can cost you more than the rate discount saves. Identifying these before you sign a contract is the single most important financial step in new construction buying.

How to Identify Hidden Costs

Start with the base price. Request a written breakdown of the home’s contract price and ask the sales agent directly: “Is this price contingent on using your preferred lender?” If the answer is yes, or if the price would be reduced with a large cash purchase, you are looking at a price that has been inflated to fund financing incentives.

Next, review the incentive structure. Builders commonly offer closing cost credits of $10,000–$25,000 — but these credits are often reduced or eliminated if you choose outside financing. Compare the total value of incentives under both scenarios, not just the interest rate.

Also examine loan fees. Builder-affiliated lenders sometimes charge higher origination fees, underwriting fees, or processing fees that partially offset the rate benefit. The Annual Percentage Rate (APR) — which includes fees — will be higher than the advertised note rate and gives you a more accurate cost comparison.

What to Watch Out For

Beware of upgrade credits tied to lender use. Some builders offer $5,000–$15,000 in design center credits only when you use their affiliated lender. These credits feel like savings but are often applied to options with high builder markups, meaning their real cash value is far less than advertised. Always ask for the cash equivalent value of any credit.

Some builder contracts include a clause stating that the purchase price will increase — often by $5,000–$10,000 — if you do not use the preferred lender. This is legal under RESPA as long as using the preferred lender is not formally required. Read every contract clause involving financing before signing.

Step 3: How Do I Compare Builder Financing Against Outside Lenders?

To properly compare builder financing against outside lenders, you must request a Loan Estimate from at least three lenders — including the builder’s preferred lender — and compare them on the same loan amount, term, and closing date. The Loan Estimate, standardized by the CFPB under the TILA-RESPA Integrated Disclosure (TRID) rules, makes side-by-side comparison straightforward if you know what to look at.

How to Do This

Step one: apply with two or three outside lenders simultaneously to receive competing Loan Estimates within three business days. Use lenders such as Better Mortgage, Rocket Mortgage, a local credit union, or a mortgage broker who can shop multiple wholesale lenders at once.

Step two: on each Loan Estimate, compare Page 1 (loan terms and projected monthly payment) and Page 2 (closing costs breakdown) side by side. The key number is the APR on Page 3 — this captures both the rate and all lender fees into a single comparable figure.

Step three: calculate the total cost scenario. Use a mortgage calculator from the CFPB’s mortgage tools portal to project total interest paid over 5, 10, and 30 years under each offer. A rate that appears only 0.25% lower can save — or cost — tens of thousands of dollars over the full loan term.

For buyers who want deeper guidance on understanding how rate differences compound over time, our breakdown of how interest rate compounding works shows exactly why small rate gaps matter far more than most people expect.

What to Watch Out For

Builder sales agents may discourage outside lender applications by citing closing timeline concerns — claiming outside lenders “won’t meet the builder’s closing date.” This is almost always a negotiating tactic, not a genuine limitation. Most outside lenders can close a new construction loan in 30–45 days, which aligns with typical builder timelines.

| Financing Option | Typical Rate Advantage | Closing Cost Credits | Flexibility | Total Cost Risk |

|---|---|---|---|---|

| Builder Preferred Lender (with full incentives) | 0.5%–1.5% below market | $10,000–$25,000 available | Low — captive lender | High if home price inflated |

| Outside Conventional Lender | Market rate (7.0%–7.5% in mid-2025) | $0–$5,000 from builder | High — competitive shopping | Low — transparent pricing |

| Mortgage Broker (wholesale) | 0.1%–0.3% below retail | $0–$5,000 from builder | High — multiple lender access | Low to moderate |

| Builder 2-1 Buydown Program | 2% below market year 1, 1% year 2 | $10,000–$20,000 tied to lender | None after closing | Very high — payment shock in year 3 |

| FHA Loan via Outside Lender | 0.1%–0.25% below conventional | $0–$5,000 from builder | High — widely available | Moderate — MIP adds long-term cost |

Ask every lender — including the builder’s preferred lender — to provide a Loan Estimate for the exact same scenario: same loan amount, same down payment, same loan type, same closing date. This creates a true apples-to-apples comparison and prevents the builder’s lender from showing a quote with reduced fees that disappears at closing.

Step 4: Can I Negotiate Builder Incentives Without Using Their Lender?

Yes — you can negotiate builder incentives without using their preferred lender, and doing so often produces a better overall financial outcome. The key is understanding that builder incentives are a negotiating lever, not a fixed benefit, and that builders have flexibility they rarely volunteer upfront.

How to Do This

Start by getting the full incentive package in writing before signing the contract. Ask the builder’s sales agent to itemize exactly which incentives apply with their preferred lender and which apply without it. This forces transparency and gives you a baseline for negotiation.

Next, use your outside lender quotes as leverage. Present the builder with your competing Loan Estimates and ask them to either match the outside lender’s total cost or convert the incentives into a direct purchase price reduction. Builders are motivated to close deals — especially on homes that have been sitting — and will often negotiate on price when they realize you are a serious, pre-approved buyer.

According to real estate attorney guidance published by the National Association of Realtors, buyers who come to the negotiating table with documented outside financing alternatives consistently secure better outcomes than those who negotiate without competing offers.

“Builders are running a business, and their preferred lender is a profit center. When a buyer walks in with a competing Loan Estimate and the knowledge that RESPA prohibits requiring captive lender use, the negotiating dynamic shifts immediately. You have more leverage than you think — but you have to exercise it before you sign, not after.”

What to Watch Out For

Some builder contracts include a “preferred lender deadline” — a date by which you must commit to using their lender to receive the advertised incentives. Do not let this deadline pressure you into a hasty financial decision. Request a deadline extension if you need more time to compare offers. Builders almost always grant it rather than risk losing the sale.

If you’re a repeat buyer using existing home equity as part of your financing strategy, see how repeat homebuyers can leverage equity to negotiate better mortgage rates — the same equity leverage principles apply when countering builder offers.

Buyers who negotiated with competing lender quotes in hand saved an average of $9,400 over five years compared to buyers who accepted the first offer, according to CFPB mortgage shopping research. That figure does not include savings from a negotiated purchase price reduction.

Step 5: Should I Accept a Builder’s Rate Buydown Program?

A builder’s rate buydown program is worth accepting only if the lower rate applies permanently to your loan, the home price has not been inflated to fund it, and you plan to stay in the home long enough to recover the embedded cost. Temporary buydowns — especially the popular 2-1 buydown — carry significant payment shock risk that many buyers underestimate.

How to Do This

First, determine whether the buydown is permanent or temporary. A permanent buydown reduces your rate for the entire loan term. A temporary buydown — such as a 2-1 or 3-2-1 program — reduces your rate for one to three years, then reverts to the full market rate. The full market rate is what you will be paying for the remaining 27–29 years of your loan.

Second, calculate the break-even on a permanent buydown. Each discount point typically costs 1% of the loan amount and reduces the rate by approximately 0.25%. On a $400,000 loan, buying the rate down by 1% costs roughly $16,000 and saves about $240 per month — a break-even of approximately 67 months, or five and a half years. If you sell or refinance before that, the buydown cost was a loss.

For a detailed analysis of when paying points makes financial sense, our guide on mortgage rate buydowns and whether paying points is worth it walks through the math for different loan scenarios.

Third, stress-test the temporary buydown scenario. If a builder offers you a 2-1 buydown on a $450,000 loan at an initial rate of 5.5%, calculate your payment at the full 7.5% rate in year three. If that payment strains your budget, the buydown is masking an affordability problem rather than solving it.

What to Watch Out For

Builders sometimes present temporary buydowns as the solution to high-rate environments by promising buyers can “refinance when rates drop.” This strategy has a name among mortgage professionals — “marry the house, date the rate” — and it carries real risk. Refinancing requires closing costs of 2%–5% of the loan amount, and rates may not fall on the schedule that makes refinancing cost-effective before the temporary buydown expires.

A 2-1 buydown on a $450,000 loan at 7.5% means your year-one payment is calculated at 5.5%, saving approximately $540 per month. In year three, that payment jumps by the full amount. If your income does not grow to match, this creates the same payment shock risk as an adjustable-rate mortgage reset. Read more about how to prepare for a rate reset before accepting any temporary rate structure.

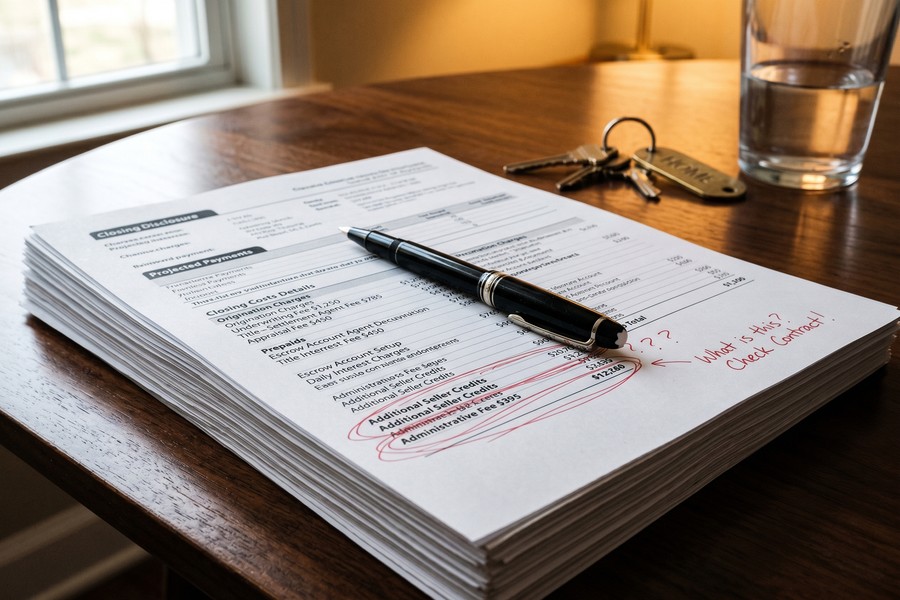

Step 6: How Do I Protect Myself From Builder Financing Traps at Closing?

Protecting yourself from builder financing traps at closing requires reviewing three documents in advance: the final Closing Disclosure, the loan’s Affiliated Business Arrangement Disclosure, and the builder contract’s financing contingency language. Surprises at the closing table are almost always traceable to a document the buyer did not read carefully before that day.

How to Do This

Receive and review your Closing Disclosure at least three business days before closing — this is your legal right under federal TRID rules. Compare it line-by-line against the Loan Estimate you received at application. Any fee that has increased beyond the allowable tolerance must be corrected before you sign.

Hire a real estate attorney to review your builder contract before signing, particularly the financing contingency and any clauses related to preferred lender use, incentive forfeiture, or price adjustment. Attorney fees typically run $500–$1,500 for contract review — a small cost relative to the potential exposure on a $400,000+ transaction.

Confirm that all verbal promises from the builder’s sales agent are memorialized in writing and attached to the contract as addenda. Verbal commitments about incentives, upgrade credits, or rate guarantees are unenforceable and routinely disappear at closing.

What to Watch Out For

Watch for last-minute fee additions from builder-affiliated lenders. These sometimes appear on the Closing Disclosure as administrative fees, document preparation fees, or loan processing fees that were not on the original Loan Estimate. Challenge any new fee that did not appear on your Loan Estimate — you have the legal right to demand a corrected Closing Disclosure.

“Buyers closing on new construction homes have the same federal disclosures and protections as any other mortgage borrower. The difference is that they often feel pressure to move quickly because of the builder’s timeline. That pressure is intentional. Slow down, read everything, and don’t sign until every number matches what you were promised.”

Common mistakes at this stage also include failing to comparison-shop during the earlier stages of the process. If you want a broader view of borrowing errors that compound into costly outcomes, our roundup of 5 mistakes borrowers make when comparing loan interest rates covers the patterns that show up repeatedly.

Request your Closing Disclosure as soon as it is ready — do not wait for the lender to send it automatically. Federal law requires delivery three business days before closing, but getting it earlier gives you more time to identify and correct errors before the closing date.

Frequently Asked Questions

Are builder offered mortgage rates always worse than going with an outside lender?

Not always, but they frequently are when you factor in the total cost rather than just the interest rate. Builder offered mortgage rates can provide genuine savings when paired with a permanent rate buydown funded entirely by the builder — but buyers must verify that the home price has not been inflated to offset the subsidy. The only way to know is to compare the full Loan Estimate from the builder’s lender against at least two outside offers on an identical loan.

Can a builder legally force me to use their mortgage company?

No. Under the Real Estate Settlement Procedures Act (RESPA), a builder cannot legally require you to use their affiliated lender as a condition of purchasing a home. However, builders can legally tie financial incentives — closing cost credits, design center upgrades, or price reductions — to using their preferred lender. This is legal as long as the incentives are disclosed and using the affiliated lender is framed as a choice, not a requirement.

What is a 2-1 buydown and is it a good deal on a new construction home?

A 2-1 buydown temporarily reduces your mortgage rate by 2% in year one and 1% in year two, reverting to the full market rate in year three for the remaining life of the loan. It is a good deal only if you plan to refinance at a lower market rate before year three, the full year-three payment is affordable on your current income, and the home price has not been inflated to fund it. Buyers who accept a 2-1 buydown without stress-testing the year-three payment frequently face unaffordable payment jumps of $400–$700 per month.

How much can I save by shopping outside of the builder’s preferred lender?

Buyers who shopped for their mortgage rather than accepting the first offer saved an average of $1,500 in closing costs alone, according to CFPB research on mortgage shopping behavior. When you include the potential for a lower rate and the negotiating leverage that competing quotes provide, total savings of $10,000–$40,000 over the life of the loan are realistic depending on the loan size and rate differential.

Should I use a mortgage broker or a direct lender to compete against a builder’s preferred lender?

A mortgage broker is often the stronger choice because they can shop your loan across multiple wholesale lenders simultaneously, frequently producing a lower rate than you could get by applying directly to individual banks. Brokers typically access wholesale rates that are 0.1%–0.3% lower than retail channel rates. That said, a direct relationship with a credit union or a well-rated online lender like Rocket Mortgage or Better.com can also produce competitive quotes worth using as leverage against the builder.

What documents should I bring to negotiate with a builder’s sales agent about their mortgage offer?

Bring printed copies of at least two competing Loan Estimates — standardized three-page documents issued within three business days of a completed mortgage application. Highlight the APR, total closing costs, and five-year total cost of ownership figures on each one. Presenting these documents signals that you are an informed buyer, which shifts the negotiation dynamic and gives the builder’s sales team a concrete benchmark to match or beat.

What happens to my builder incentives if I switch to an outside lender after signing the contract?

It depends entirely on your contract language. Many builder contracts specify that closing cost credits, design center allowances, or price concessions are conditional on using the preferred lender, and switching to an outside lender forfeits those incentives. Review the contract with a real estate attorney before signing to understand exactly which incentives are lender-contingent and whether the financial advantage of outside financing outweighs the lost credits.

Is a builder’s mortgage rate offer actually a discount point purchase, or is the rate genuinely lower?

In most cases, the lower rate is achieved through discount point purchases made by the builder on the buyer’s behalf — funded from the builder’s marketing budget, an inflated home price, or reduced incentives elsewhere in the package. The rate is real and will apply to your loan, but it is not “free.” You are paying for it somewhere in the transaction, whether through a higher purchase price, reduced upgrade credits, or a smaller closing cost contribution. Identifying exactly where that cost is embedded requires a full contract and Loan Estimate analysis.

How do I know if a builder inflated my home’s price to fund the mortgage rate incentive?

Compare the builder’s contract price for your specific home against recent closed sales of comparable homes in the same community or nearby new construction developments using Zillow’s sold data, Redfin, or your county assessor’s records. If similar homes — same square footage, same finishes, same subdivision — are selling for less with no financing incentives, the price difference is likely funding the rate subsidy. An independent appraisal ordered before closing can also flag overpricing relative to market value.

What should I do if I already closed on a new construction home and realize I overpaid through builder financing?

Refinancing is your primary option, and it makes sense if current market rates are meaningfully lower than your existing rate or if a lower rate is available that breaks even within your planned ownership horizon. Review our analysis of whether to refinance now or wait for rates to drop to assess whether your situation supports an immediate refinance. If rates have not moved favorably, focus on aggressive principal paydown in the short term to reduce your total interest exposure.

Sources

- Consumer Financial Protection Bureau — Compare Loan Offers

- CFPB — Consumers Who Shopped for Mortgages Saved Money

- National Association of Home Builders — Housing Economics Research

- Consumer Financial Protection Bureau — Loan Options and Mortgage Tools

- National Association of Realtors — Negotiating With Home Builders

- U.S. Department of Housing and Urban Development — RESPA Overview

- Consumer Financial Protection Bureau — What Is a Loan Estimate?

- Federal Reserve — Selected Interest Rates (H.15)

- Freddie Mac — Primary Mortgage Market Survey

- Consumer Financial Protection Bureau — Understanding Your Closing Disclosure