How Freelancers Can Qualify for Online Loans Without Steady Pay Stubs

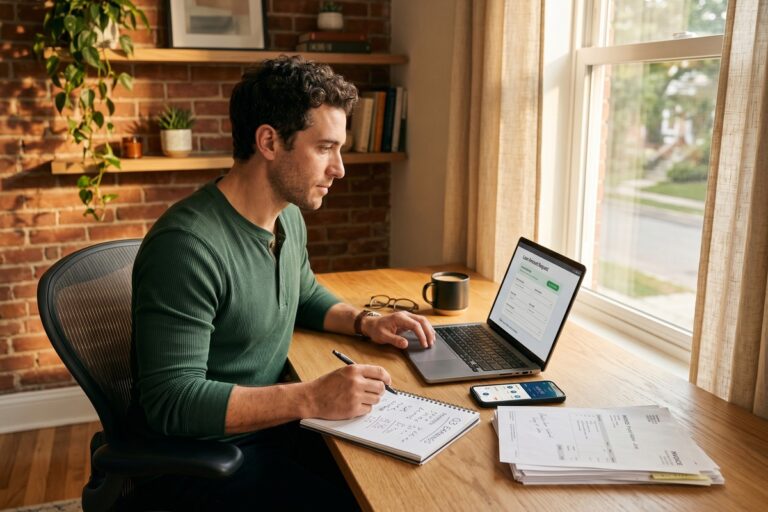

38% of U.S. workers freelanced in 2023, yet most lenders still flag self-employment. Bank statements, Schedule C, and 1099s can replace pay stubs for online loan approval.

38% of U.S. workers freelanced in 2023, yet most lenders still flag self-employment. Bank statements, Schedule C, and 1099s can replace pay stubs for online loan approval.

Over 40% of first-time digital borrowers underestimate total loan costs by 20% or more. Here are the five mistakes driving that gap—and how to avoid them.

Upstart, OppFi, and Avant approve scores as low as 300—but APRs can reach 160%. Here's how to compare bad-credit lending apps before you commit.

Digital banks can approve personal loans in 24 hours; P2P platforms take 3–5 days but accept borrowers banks turn down. Here's how to choose.

Five buried charges—including prepayment penalties and ACH fees—can push your loan's real APR 3–8 points above the advertised rate. Here's what to look for before you sign.

A single mother covered a $3,200 medical bill in under 48 hours using a fintech lender—no bank visit required. Here's how AI-powered underwriting made it possible.

45 million Americans are credit invisible to FICO models. Here's how cash flow lending compares to credit score lending—and which platform approach actually funds more borrowers.

Secured digital loans run 6%–12%; unsecured ones can hit 36%. Here's how your credit score and collateral determine which loan type actually saves you money.

Most fintech lenders cap approvals at 40–45% of verified income. See exactly what algorithms check and how to close the gap on your next application.

59 million gig workers can't produce W-2s, but bank statement analysis and platforms like Argyle or Pinwheel help them qualify. Here's what lenders actually check.