Digital Loan Prepayment Penalties: How Lenders Hide Fees in the Fine Print

While only 0.248% of mortgages carry prepayment penalties, digital lenders routinely hide them in contracts using deliberately vague language. Here's what borrowers miss.

While only 0.248% of mortgages carry prepayment penalties, digital lenders routinely hide them in contracts using deliberately vague language. Here's what borrowers miss.

College students can access $500–$50,000 through fintech lenders using alternative underwriting. Learn how to compare offers, avoid credit damage, and borrow only what you need.

When a SaaS employee lost his job with no warning, a digital loan kept his mortgage paid through 22 weeks of unemployment. Here's how he made it work.

Variable rates start 2–4 points lower than fixed, but borrowers on digital platforms taking loans past 36 months almost always pay more. Here's what the math actually shows.

Over 16 million U.S. small businesses face seasonal revenue gaps that turn banks away. Here's how digital lenders are filling that gap — and what to watch out for.

Learn about comparing APR digital lenders. Discover hidden fees, rate structures, and key factors most borrowers overlook when evaluating digital lending platforms.

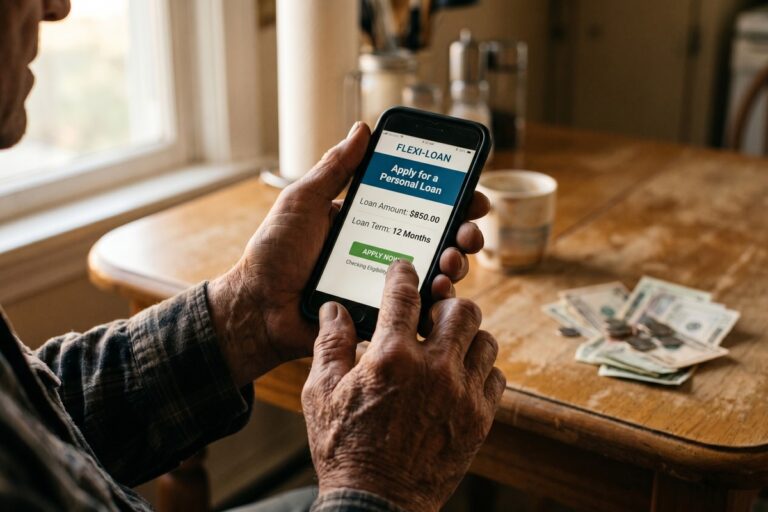

Seniors can get approved for digital loans on fixed income in 15–30 minutes by documenting all income sources and using soft prequalification tools. The ECOA protects you from credit denial based on Social Security income.

A 6–8 week licensing backlog can halt a travel nurse's income entirely. Here's how one nurse used a digital loan to stay solvent across three state transfers.

Earnin, Dave, MoneyLion, and Possible Finance can put $50–$500 in your account within the hour — but APRs can top 300%. Here's what each platform actually delivers.

A hard pull can drop your score 5–10 points and sits on your report for 2 years—yet most borrowers trigger one without realizing it by accepting a pre-qualified offer.