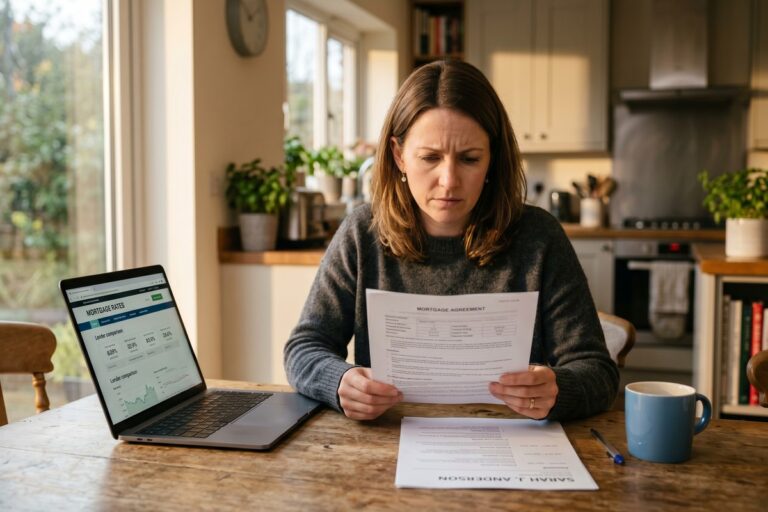

Should You Buy Down Your Mortgage Rate With Points When Home Prices Are Still High?

Learn about buy down mortgage rate points. Discover if paying points makes sense when home prices are high and how to calculate your break-even timeline.

Learn about buy down mortgage rate points. Discover if paying points makes sense when home prices are high and how to calculate your break-even timeline.

With the 30-year fixed rate near 6.8% and forecasters predicting only a 0.25–0.50% drop by year-end, waiting may cost you equity and expose you to rising home prices.

Learn about FHA vs conventional rates. Compare total loan costs, MIP vs PMI, and find out which mortgage path saves you more money over time.

Learn about divorce buyout mortgage rates. Discover how buying out a spouse affects your rate, loan terms, and what lenders require to refinance.

A single employment gap can raise your mortgage rate by 0.25%–0.50% or trigger a denial. Here's how underwriters score gaps and what documentation saves your rate.

The 30-year fixed rate has fallen to 6.4% after peaking at 7.8% in 2023—here's what's driving the drop and whether rates will reach 6.0% by year-end.

If your mortgage rate is above 7.5%, refinancing now likely makes sense — even with further Fed cuts possible. Here's how to run the numbers for your situation.

One point costs 1% of your loan and cuts your rate by ~0.25% — but you'll need 5–7 years to break even. Here's how to tell if buying down your rate is worth it.

Two years of tax returns, a 700+ credit score, and a DTI below 43% are the benchmarks lenders use—here's how self-employed borrowers can meet them and close.

30-year fixed rates now range from 6.4%–7.1%, with FHA loans averaging 6.2%. Here's how today's rates affect what first-time buyers can actually afford.