Fact-checked by the CapitalLendingNews editorial team

The Verdict

Adding a co-borrower with bad credit to your mortgage is worth it only when their income drops your combined debt-to-income ratio below 43% and lets you qualify for a loan you otherwise could not get. It is not worth it if you already qualify alone, because the weaker credit score will almost certainly raise your rate by 0.25 to 0.75 percentage points or more.

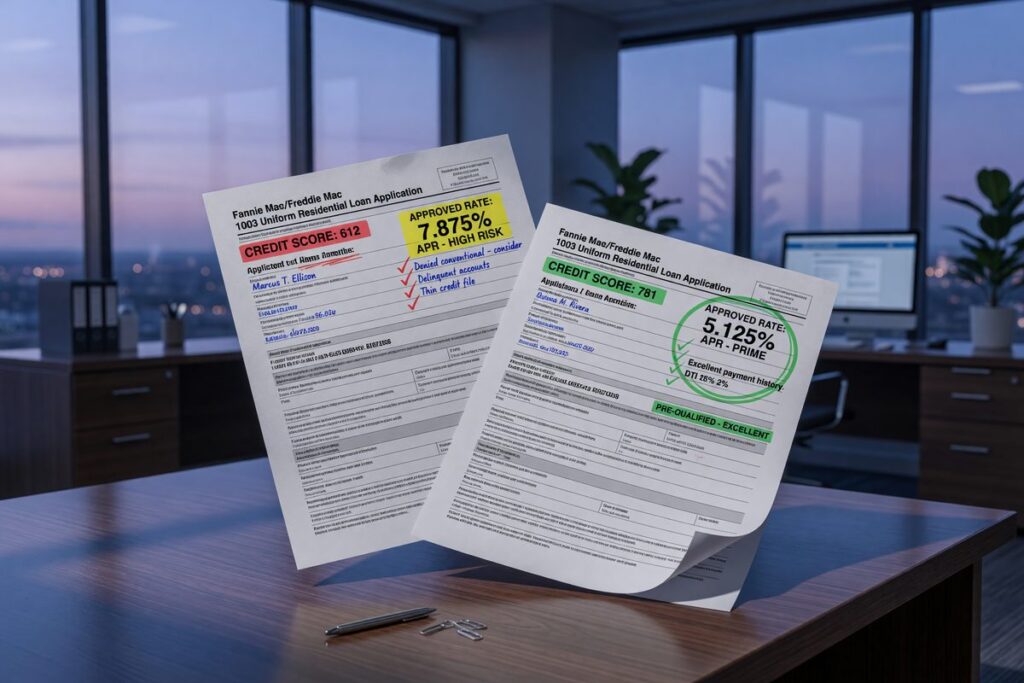

Start with a concrete picture: a borrower with a 760 median credit score applies for a conventional mortgage and qualifies for a rate around 6.75%. Their co-borrower carries a 630 median score. Under the most common lender pricing method, that 630 becomes the number the rate is built on, and the final quote jumps to somewhere between 7.25% and 7.75%. That spread on a $400,000 loan adds roughly $130 to $200 per month. The co-borrower bad credit mortgage rate problem is real, consistent, and often underestimated by borrowers who assume lenders average the two scores together.

With mortgage rates still elevated heading into late 2025, the cost of a bad co-borrower score is amplified. Even a modest rate penalty that might have been tolerable when rates sat at 4% becomes a significant long-term liability at current levels.

| Factor | Reasons to Add the Co-Borrower | Reasons Not to Add the Co-Borrower |

|---|---|---|

| Qualification | You cannot qualify alone; co-borrower income is required to meet lender minimums | You already qualify; adding them serves no purpose except to raise risk |

| Rate Impact | Income improvement outweighs the rate penalty in total monthly cost | Their score drops the qualifying median below 680, triggering significant Loan-Level Price Adjustments |

| DTI Relief | Combined DTI falls from 51% to 42%, moving you into an approvable tier | Co-borrower carries high existing debt that pushes combined DTI above 45% |

| Loan Type | FHA allows non-occupant co-borrowers with fewer credit restrictions | Conventional loans penalize LLPAs more sharply when the qualifying score is below 740 |

| Future Credit | Both borrowers build payment history from day one | Joint liability limits both parties’ borrowing capacity for up to 2 years after application |

| Exit Strategy | Refinance is feasible if the co-borrower rebuilds credit within 2 to 3 years | Removing the co-borrower requires a full refinance or assumption; no simple release available |

Key Takeaways

- The co-borrower’s score (not an average) sets the qualifying rate in most conventional loan scenarios, unless the file goes through Fannie Mae’s Desktop Underwriter averaging method

- Adding a co-borrower is likely worthwhile if their income drops your combined DTI by at least 5 percentage points and gets you below 43%

- If the co-borrower’s median credit score is below 640, expect Fannie Mae Loan-Level Price Adjustments to add 1.5 to 2.75 points in upfront cost on a conventional loan

- FHA loans are more forgiving on co-borrower credit but layer on mortgage insurance premiums that currently sit at 0.55% annually for most borrowers

- Both borrowers carry the full mortgage liability on their credit reports, affecting future rate quotes for up to 24 months after application

- A rate reduction refinance is the only realistic exit strategy, meaning you should have a clear credit-repair timeline before signing jointly

- PMI pricing on conventional loans factors in the qualifying (lower) credit score, meaning the insurance premium compounds the rate penalty if that score falls below 680

How Lenders Actually Evaluate a Joint Application With Mixed Credit

The qualifying score on a joint mortgage is almost never the average of both borrowers’ numbers. Most lenders pull three scores from each borrower across Equifax, Experian, and TransUnion, take the middle value for each person, and then use the lower of those two middle values as the representative score for pricing and eligibility. This is the single most important mechanical fact for any borrower considering a co-borrower with bad credit.

According to the Consumer Financial Protection Bureau, most conventional lenders will offer a rate based on the smallest median credit score between the applicants rather than averaging the two numbers together.

There is one meaningful exception. Fannie Mae’s updated guidelines allow lenders using Desktop Underwriter to calculate eligibility based on the average of both borrowers’ median scores for certain loan files, a change that took effect in 2021. In practice, many lenders still use the lower-score method for rate locking even when the averaged score technically clears the eligibility threshold. The distinction matters because a borrower with a 760 and a co-borrower with a 630 has an average of 695, which unlocks better pricing than a straight 630 floor. Ask your lender explicitly which method they are applying to your file.

Automated underwriting systems like Fannie Mae’s Desktop Underwriter and Freddie Mac’s Loan Product Advisor do more than check a score. They assess payment history depth, recent delinquencies, revolving utilization, and the age of open accounts for every borrower on the application. A co-borrower with a 630 score driven by two recent 30-day late payments is treated differently than one with a 630 from a thin credit file. The former flags additional risk overlays; the latter may slide through with fewer compensating requirements.

Why a Bad-Credit Co-Borrower Raises Your Rate: The Pricing Mechanics

Loan-Level Price Adjustments, or LLPAs, are the primary tool Fannie Mae and Freddie Mac use to translate credit risk into cost. They are expressed as a percentage of the loan amount and are either paid upfront at closing or absorbed into a higher interest rate. Per the Fannie Mae LLPA matrix, a co-borrower with a 630 median score does not just slightly raise your rate; it can trigger adjustments that cost 1.5 to 2.75 points on the loan amount before a single other risk factor is added.

LLPAs do not operate in isolation. They stack with loan-to-value ratio. A borrower putting 10% down with a 630 qualifying score faces a higher combined adjustment than the same score at 25% down. The LLPA grids illustrate how these two variables intersect, and the penalties grow sharply once the qualifying score drops below 680. Below 640, many conventional programs simply stop approving the file, regardless of compensating factors.

PMI compounds the problem. Private mortgage insurance on conventional loans with less than 20% down is priced, in part, on the qualifying credit score. When the co-borrower’s score pulls that number below 680, the borrower pays both a higher base rate and a higher PMI premium. These two costs layer on top of each other, not alongside. For a genuine picture of the co-borrower bad credit mortgage rate impact, a borrower needs to calculate the fully loaded monthly payment including PMI, not just compare headline interest rates.

Debt-to-income ratio intersects here too. If the co-borrower’s income genuinely improves the file’s DTI from a borderline 48% down to a clean 41%, lenders may grant a slightly better rate tier even though the credit score dropped. The DTI improvement does not erase the LLPA, but it can offset a portion of the effective APR. This is the narrow scenario where adding a weak-credit co-borrower might still make financial sense. For a deeper look at how DTI shapes lender decisions, see our breakdown of how debt-to-income ratio quietly kills loan applications.

Conventional vs. FHA, VA, and Non-QM: Rate Treatment Across Programs

FHA loans handle co-borrower credit differently, and for some borrowers that difference is the deciding factor. The Federal Housing Administration allows non-occupant co-borrowers on owner-occupied FHA loans with fewer credit restrictions than Fannie Mae or Freddie Mac impose. A parent with poor credit can co-sign an FHA loan for an adult child who is the occupying borrower, and the program does not disqualify the file solely on the co-borrower’s score the way conventional guidelines can.

The tradeoff is the mortgage insurance premium. FHA MIP currently runs at 0.55% annually for most 30-year loans with a down payment above 10%, per HUD’s 2023 mortgage letter. That insurance is calculated on the full loan balance and does not drop off automatically until the loan reaches certain age and equity thresholds. Conventional PMI, by contrast, can be removed once the borrower reaches 20% equity, and is not required at all above that threshold. For borrowers who plan to refinance once the co-borrower improves their credit, the conventional route with its removable PMI may cost less over a three-to-five year horizon even if the upfront rate is higher.

VA loans, available to eligible veterans and active service members, do not use LLPAs in the conventional sense, and VA does not set a minimum credit score at the program level (though individual lenders typically apply overlays around 580 to 620). A co-borrower on a VA loan who is not a veteran or spouse, however, means the VA guarantee applies only to the veteran’s share of the loan, which can increase the effective cost and limit the loan amount. Non-QM lenders offer a third path: they may accept co-borrower scores below 580 and underwrite to their own guidelines, but rates on non-QM products typically run 1 to 2 percentage points above comparable conventional products to begin with. The flexibility comes at a substantial cost.

For borrowers weighing these program tradeoffs, our detailed comparison of FHA loan rates versus conventional mortgage rates over time provides a useful framework.

Who Should and Who Should Not Add a Bad-Credit Co-Borrower

Good candidates

Adding a co-borrower with poor credit makes sense in a specific set of circumstances where the income benefit clearly outweighs the rate cost.

- A borrower who cannot qualify alone because their income is insufficient, and the co-borrower’s income drops combined DTI by at least 5 percentage points into the approvable range

- A borrower applying for an FHA loan where the credit floor is more forgiving and the co-borrower’s poor score does not disqualify the file outright

- A borrower with a realistic plan to refinance within two to three years once the co-borrower rebuilds their credit score above 680 or 720

- A borrower where the co-borrower’s score is close to a better LLPA tier (for example, 655 vs. the 660 threshold) and could qualify under Fannie Mae’s averaging method with a specific lender

Who should skip it

For others, the math simply does not work in favor of adding a borrower with damaged credit.

- A borrower who already qualifies alone with a score above 720 and a DTI below 43%; adding a co-borrower with a 600 score gains nothing and costs real money in rate premium

- A borrower purchasing an investment property, where non-occupant co-borrower restrictions are tighter and LLPAs are already higher across the board

- A borrower who cannot afford a higher rate during the period before a refinance is possible, particularly if they are near the edge of their monthly budget

- Anyone in a relationship where removing the co-borrower is likely to be contested, since the only exit requires a full refinance or assumption and both parties must consent

Joint Liability, Future Borrowing Power, and Getting Out

Both borrowers carry the full mortgage balance as a liability on their credit reports from the day the loan closes. This is not a shared 50-50 split; each person’s credit file shows the entire balance, which affects their individual debt-to-income calculations for any future borrowing. A co-borrower who later tries to buy their own home or refinance a vehicle faces the full weight of the joint mortgage in their file.

Credit inquiries from the joint application process also linger. Hard pulls remain on each borrower’s report for two years, and new accounts carry an age penalty that can suppress scores in the near term. As FICO explains in its credit education resources, new credit inquiries and recently opened accounts both affect score calculations in ways that borrowers often underestimate. Those who understand that a joint application has consequences for both parties’ future rate quotes are better positioned to make the decision rationally. The relationship between credit score mismatches and joint loan pricing is explored further in our article on how co-borrowers with mismatched credit scores affect interest rates on joint loans.

Removing a co-borrower after closing is harder than most borrowers expect. Lenders do not grant a simple administrative release of liability. The standard options are a full refinance into the stronger borrower’s name alone (requiring that borrower to qualify independently at current rates), a loan assumption (rare on conventional loans, more common on FHA and VA), or a sale of the property. Given that rates in late 2025 remain meaningfully higher than the levels many borrowers locked in during 2020 and 2021, a refinance exit strategy carries its own cost. Build that cost into the decision before you sign.

If the goal is to use a co-borrower’s income strategically while keeping options open, borrowers should also review how repeat homebuyers can use equity to negotiate better mortgage rates, since accumulated equity in a property can eventually support a solo refinance without requiring the co-borrower’s continued involvement.

Frequently Asked Questions

Does adding a co-borrower with bad credit always raise my mortgage rate?

In most conventional loan scenarios, yes. The lender uses the lower of the two borrowers’ median credit scores for rate pricing, so a co-borrower with a significantly lower score will pull the qualifying number down and trigger higher Loan-Level Price Adjustments. The exception is when a lender applies Fannie Mae’s averaging method under Desktop Underwriter, which uses the average of both median scores for certain files. Ask your lender explicitly which method applies to your application.

Can a co-borrower’s income offset the rate penalty from their bad credit?

Partially. Strong income from the co-borrower can lower your combined debt-to-income ratio enough to move into a more favorable approval tier, and a lower DTI can slightly improve rate pricing. It does not eliminate the LLPA credit-score penalty, but it can reduce the net cost difference. The income benefit has to be large enough to justify the higher rate and PMI cost over the life of the loan before the comparison makes sense.

Is an FHA loan better when my co-borrower has a low credit score?

Often, yes, particularly when the co-borrower is a non-occupant. FHA allows non-occupant co-borrowers with more flexibility than conventional guidelines, and the program does not disqualify a file solely on the co-borrower’s score. The ongoing mortgage insurance premium, currently at 0.55% annually for most loans, is the real cost to weigh against the flexibility. If you plan to stay in the loan for more than five to seven years, that cumulative insurance cost may exceed what a conventional LLPA penalty would have cost upfront.

How do I remove a co-borrower from a mortgage after closing?

A full refinance into the remaining borrower’s name alone is the most common path, and it requires that borrower to qualify independently at whatever rates exist at that time. Loan assumptions are possible on FHA and VA loans but require lender approval and qualification by the assuming borrower. Conventional loan assumptions are extremely rare. There is no simple administrative release option; lenders will not remove liability without re-underwriting the file.

Sources

- Fannie Mae Selling Guide: General Requirements for Credit Scores

- Fannie Mae Loan-Level Price Adjustment (LLPA) Matrix

- Fannie Mae Desktop Underwriter Overview

- Freddie Mac Loan Product Advisor Overview

- U.S. Department of Housing and Urban Development: FHA 203(b) Mortgage Insurance Program

- HUD Mortgagee Letter 2023-16: Annual Mortgage Insurance Premium Rates

- U.S. Department of Veterans Affairs: VA Home Loan Program

- Consumer Financial Protection Bureau: What Is a Co-Borrower?

- myFICO: How Credit Inquiries Affect Your Credit Score

- Bankrate: Should You Add a Co-Borrower to Your Mortgage?

- Equifax: Credit Score Information

- Experian: Credit Score Resources

- TransUnion: Credit Score Information

- Consumer Financial Protection Bureau: Explore Interest Rates Tool

- Urban Institute: The Case for Mortgage Credit Score Reform