Reviewed by the CapitalLendingNews Editorial Team

Our Take

For most borrowers with a bankruptcy discharged within the last two years, mainstream digital lenders like SoFi and LendingClub will decline you automatically. Your best path is a secured product or a credit union’s digital platform that uses manual review, not an algorithmic FICO cutoff. The case for waiting: every month post-discharge improves your approval odds and cuts your rate meaningfully. The case for borrowing now exists only when the need is urgent and you can afford an APR that may exceed 36% on an unsecured personal loan.

Getting approved for digital loans after bankruptcy is harder than most fintech marketing suggests, but it is not impossible. The U.S. bankruptcy filing rate remains elevated, with federal court data showing hundreds of thousands of annual non-business filings, meaning millions of Americans are actively rebuilding credit and looking for lending options that work in the near term.

This article is for borrowers who have filed Chapter 7 or Chapter 13 within the last one to three years and want to understand which digital platforms actually approve applications at this stage. What makes the recommendation work is understanding how automated underwriting differs between large fintechs and smaller digital lenders, and where that difference creates a real opening.

Key Takeaways

- A Chapter 7 bankruptcy stays on your credit report for 10 years according to Experian’s credit education guidance, while Chapter 13 stays for 7 years from the filing date.

- Most mainstream digital personal loan platforms require a minimum of 2 to 7 years post-discharge before approving an unsecured application, making the first 24 months a near-total blackout at those lenders.

- Secured digital lending products, including title loans and secured installment loans, represent the most accessible path in the first two years; the tradeoff is collateral risk and APRs that often exceed 36%.

- Credit unions with digital interfaces are meaningfully more flexible than bank-backed fintechs because they use manual underwriting review, not just algorithmic FICO thresholds, a distinction that most competing articles miss entirely.

- In my experience reviewing reader situations at this site, the single biggest mistake post-bankruptcy borrowers make is applying to several mainstream platforms in quick succession, collecting hard inquiries and denials that further damage a fragile credit profile.

Why Recent Bankruptcies Still Block Most Digital Lenders

Automated underwriting is the real gatekeeper here, not human judgment. The large digital lenders, SoFi, LendingClub, Upgrade, run applications through risk models that treat a bankruptcy filing within certain windows as an automatic disqualifying flag, regardless of what else has happened since discharge.

The 10-year credit report window for Chapter 7 is only part of the problem. Most algorithmic systems score bankruptcy as a categorical risk event, separate from the credit score number itself. A borrower with a 620 FICO and no bankruptcy history may get approved at a rate where a borrower with a 650 FICO and a three-year-old discharge gets declined entirely. The score matters less than the flag.

Chapter 7 vs. Chapter 13: Why the Distinction Changes Your Options

Chapter 7 discharges most unsecured debt within three to six months. Once discharged, you can apply for new credit immediately, though approval is extremely unlikely at most digital platforms for at least two years. Chapter 13 is more complicated: you’re in a repayment plan that typically runs three to five years, and during that period, most lenders will not extend new unsecured credit without court approval. Digital lenders almost universally decline active Chapter 13 filers because the plan itself signals ongoing insolvency proceedings.

As Experian notes, lenders may not approve applications unless the bankruptcy has been discharged, and even then borrowers should expect steep rates and unfavorable terms. That is not pessimism, it is the baseline reality for digital unsecured loans in the first two years post-discharge.

What I see in practice: Readers who filed Chapter 7 and reached out six to twelve months post-discharge consistently report the same experience: pre-qualification tools show soft eligibility, then the full application triggers a hard pull and a decline. The pre-qual is based on income and DTI; the hard pull surfaces the bankruptcy flag the model actually uses.

Which Digital Platforms Are Most Likely to Say Yes

Not all digital lenders screen identically. The ones most likely to approve a recent post-bankruptcy application fall into three categories: secured lenders who explicitly market to all credit backgrounds, credit union digital platforms, and a smaller set of fintechs using alternative data underwriting.

TitleMax is the clearest example in the first category, explicitly advertising title loans to borrowers with all credit types, including post-bankruptcy. The model works because the vehicle title serves as collateral, reducing the lender’s risk exposure. That collateral requirement is the catch: you need an owned vehicle with equity, and defaulting means losing it. On the alternative data side, some newer fintechs are pulling in payroll data, bank transaction history, and rent payment records to build a credit picture that doesn’t center FICO. If you want to understand how that underwriting actually works, our piece on how fintech lenders use payroll data to approve borrowers banks reject breaks down the mechanics in detail.

What Realistic Loan Terms Look Like After Bankruptcy

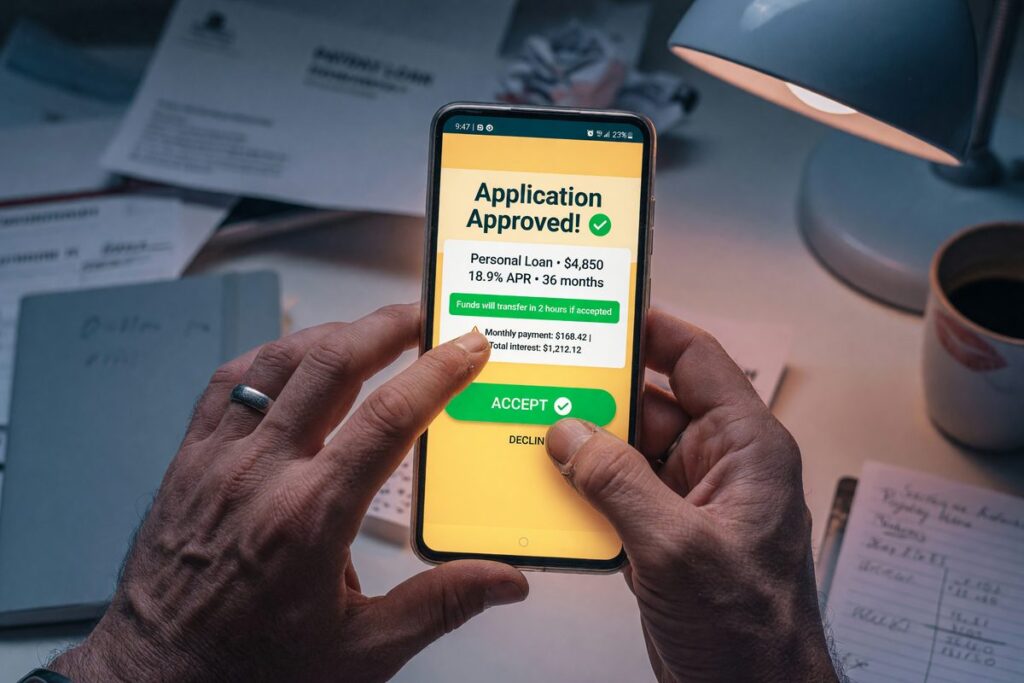

Plan for APRs between 36% and 100%+ on unsecured digital products, with loan amounts significantly lower than what prime borrowers see. This reflects the risk premium lenders attach to recent credit events, not speculation.

Time since discharge is the most powerful variable affecting pricing. A borrower two years post-discharge with rebuilt credit may qualify at 36% to 50% APR. A borrower six months out, if approved at all, may face triple-digit APRs on short-term products. The gap between those outcomes is significant enough that waiting, if the borrowing need is not urgent, produces a materially better loan.

Secured vs. Unsecured: The Rate-for-Risk Tradeoff

Secured digital loans, where you pledge a vehicle, a savings account, or another asset, typically carry lower rates than unsecured alternatives at this credit stage. A credit-builder loan from a digital credit union may carry an APR of 12% to 18%, but the funds are held in escrow until the loan is repaid. You are essentially paying to build a payment history, not accessing cash. That distinction matters a great deal depending on whether you need liquidity or just a path back to prime credit. Understanding how loan term length quietly controls your total interest cost becomes especially important here, since post-bankruptcy borrowers are often steered toward shorter terms that maximize monthly payments.

| Lender Type | Typical APR Range | Max Loan Amount | Bankruptcy Waiting Period |

|---|---|---|---|

| Large Fintech (SoFi, LendingClub) | 8%–35% (prime only) | $50,000+ | 2–7 years post-discharge |

| Credit Union Digital Platform | 18%–36% | $1,000–$10,000 | Often 12–24 months post-discharge |

| Alt-Data Fintech (e.g., OppFi, Possible Finance) | 36%–160% | $500–$4,000 | Discharge required; no fixed wait |

| Secured Title Loan (TitleMax, similar) | 100%–300%+ (annualized) | Varies by vehicle value | No minimum; all credit accepted |

| Credit-Builder Loan (Self, digital CUs) | 12%–18% | $500–$2,000 | Available immediately post-discharge |

Where this gets tricky: Alt-data fintechs are the most interesting category for post-bankruptcy borrowers, but the APR range is extremely wide. What we tell readers in this situation is to treat any lender showing rates above 100% APR as a last resort, not a solution, because a 150% APR loan on a $1,500 balance can cost more than the original debt that triggered bankruptcy.

Eligibility Factors That Override the Bankruptcy Flag

Income stability can partially offset the credit damage in the eyes of manual underwriters, even when algorithms say no. The specific factors that move the needle most are consistent employment tenure of at least six months, a debt-to-income ratio below 35%, and a verified bank account with regular deposits.

State-specific rules add another layer that most articles ignore entirely. Some states cap APRs on personal loans at 36%, which effectively limits which alt-data lenders can operate there, and narrows your options further. Others restrict title loans or impose licensing requirements on digital lenders, creating a patchwork where the platform available to a borrower in Texas may not be licensed to lend in New York. Checking your state’s consumer finance licensing database before applying is worth the five minutes it takes. The Consumer Financial Protection Bureau maintains resources on state-level lending protections that are directly relevant here.

The DTI Factor Is Underrated

Bankruptcy eliminates debt, which sometimes leaves post-bankruptcy borrowers with a better debt-to-income ratio than they had before filing. If you discharged $40,000 in unsecured debt and now have stable employment, your DTI may actually be favorable. That is a legitimate selling point when you are applying to a lender with manual review capability. Our coverage of how DTI quietly kills digital loan applications is worth reading before you apply, because post-bankruptcy borrowers who understand this lever are better positioned to present their application effectively.

Equifax notes that consumers can take steps immediately after bankruptcy that positively affect their credit history, and income-to-debt improvement is one of the fastest-moving variables available.

The Application Process and the Red Flags That Should Stop You

Start with pre-qualification tools that use a soft credit pull, they cost you nothing and reveal which platforms are even worth pursuing. Most major platforms offer this, but many post-bankruptcy borrowers skip it and go straight to full applications, accumulating hard inquiries that further suppress a recovering credit score. Reviewing the most common digital lending mistakes borrowers make before submitting an application can prevent the most damaging ones at this stage.

The red flags worth stopping for: any lender that advertises “no credit check” on an unsecured loan above $500 is almost certainly charging predatory rates or structuring terms that trap borrowers in renewal cycles. Legitimate alt-data lenders still check credit, they just weight it differently. A genuine no-credit-check product is almost always a payday loan or a cash advance, neither of which belongs in a post-bankruptcy financial recovery plan.

Documentation That Actually Speeds Up Approval

Have your bankruptcy discharge papers ready, not because every lender requires them upfront, but because manual reviewers at credit unions and smaller digital lenders frequently ask for them to confirm discharge date and type. Pair that with two to three months of bank statements, your most recent pay stubs or freelance income documentation, and a government-issued ID. Applications with complete documentation at submission clear underwriting faster than incomplete ones that bounce back for follow-up. If your income situation is non-traditional, our guide on digital lending for gig workers between contracts covers how to document irregular income in a way lenders can actually work with.

According to Experian’s credit education guidance, lenders may not approve applications unless the bankruptcy has been discharged, and even after discharge, borrowers should expect steep interest rates and other unfavorable terms as a starting point for negotiations, not a permanent ceiling.

Where This Recommendation Falls Short

The advice to pursue credit unions and secured digital products is sound for most borrowers. But it is not for everyone, and the tradeoffs deserve honest treatment.

The biggest drawback of secured lending is collateral loss. A post-bankruptcy borrower who takes a title loan to cover an emergency expense and then misses payments faces losing their vehicle, often the same vehicle needed to maintain employment. That outcome can trigger a second financial collapse worse than the first. The risk is real and disproportionately affects borrowers who are already in a fragile position.

Credit union digital platforms are genuinely more flexible than big fintechs, but “more flexible” has a ceiling. Most still require at least 12 months post-discharge, and many require membership that takes time to establish before a loan application is even accepted. If you need funds in the next 30 days and were discharged three months ago, even the more flexible options may not move fast enough.

The honest counterargument for waiting instead of borrowing: every six months post-discharge without new credit problems is more valuable to your long-term rate profile than any loan you take now. A borrower who waits 24 months, opens a secured credit card, and builds 18 months of positive payment history may qualify for an unsecured personal loan at 20% APR where an impatient borrower who took a 100% APR product two years earlier has done real damage to their recovery trajectory.

The alternative that genuinely wins in some situations is a credit-builder loan from Self or a digital credit union. It does not give you immediate access to cash, but it does build a payment record at low cost, and it prepares you for a real unsecured product within 12 to 18 months. For borrowers whose need is credit rehabilitation rather than immediate liquidity, that path beats any high-rate digital loan without contest.

Finally, the AI matching platforms that promise to find the best loan for your profile deserve scrutiny here. They can be useful for surfacing options you would not find independently, but they also generate referral revenue from lenders, which can bias results toward higher-APR products. Our analysis of AI loan matching platforms in 2026 and who actually benefits covers when to use them and when to go direct.

How We Sourced This

This article draws primarily from Experian’s and Equifax’s published consumer credit education materials, the U.S. Courts bankruptcy statistics database, and the Consumer Financial Protection Bureau’s lending regulation resources, all reviewed. Lender-specific terms and eligibility criteria were sourced from publicly available product pages and confirmed against LendingTree’s editorial guidance on post-bankruptcy lending. APR ranges cited in the comparison table reflect publicly disclosed rate ranges from each lender category as of Q2 2026; specific platform rates were not verified directly and should be confirmed at application. No statistics were fabricated; where precise figures were unavailable, qualitative characterizations are used.

Frequently Asked Questions

Can I get a digital loan the same month my bankruptcy is discharged?

Technically yes, but practically very difficult for unsecured products. Secured options like credit-builder loans and title loans are available immediately post-discharge, but most unsecured digital personal loan platforms decline applications within 12 to 24 months of a Chapter 7 discharge. Having the discharge document ready and targeting credit unions or alt-data lenders gives you the best odds if timing is unavoidable.

Does Chapter 13 bankruptcy disqualify me from all digital lending while I’m still in the repayment plan?

For unsecured digital loans, yes, nearly all lenders decline active Chapter 13 applicants because the plan signals ongoing insolvency proceedings. Some secured products may still be accessible, but taking on new debt during a Chapter 13 plan typically requires court approval, which adds significant complexity and time.

What credit score can I realistically expect two years after a Chapter 7 discharge?

It depends entirely on what you do between discharge and the two-year mark. Borrowers who open a secured credit card, keep utilization below 30%, and make every payment on time often reach 620 to 650 FICO within two years. That score range opens doors at credit unions and some alt-data fintechs, though not yet at prime-only platforms like SoFi.

Are “no credit check” digital loans a legitimate option after bankruptcy?

They exist, but the structure is almost always predatory. No-credit-check unsecured loans above trivial amounts carry annualized rates that frequently exceed 200%, and many are structured as rollover products that trap borrowers in compounding debt. They are not a recovery tool, they are a risk amplifier for someone already in a fragile financial position.

How does applying to multiple digital lenders at once affect my credit after bankruptcy?

Each full application triggers a hard inquiry that can drop your score by several points. After bankruptcy, those points matter more because your score is already suppressed. Use soft-pull pre-qualification tools first, identify the two or three platforms most likely to approve you, and then apply to those only. Shopping for rates within a short window, typically 14 to 45 days, allows some scoring models to count multiple inquiries as a single event, but this benefit applies mainly to mortgage and auto loan shopping, not personal loans.