Fact-checked by the CapitalLendingNews editorial team

Quick Answer

First-time buyers can secure a lower interest rate without a large down payment by improving their credit score to 740 or above, choosing the right loan program (including the FHFA’s automatic rate discount that cuts conventional loan pricing by 0.25–0.375%), collecting at least four lender quotes, and negotiating seller-paid buydowns. Most buyers can execute this process in 60–90 days of preparation.

Securing a competitive first-time buyer interest rate does not require a 20% down payment. The real pricing levers are your credit score, debt-to-income ratio, loan program selection, and how many lenders you actually compare, and on all four of those dimensions, you have meaningful control before you ever submit an application. According to Bankrate’s review of NAR data, the median down payment for first-time buyers in 2024 was just 9%, which means most buyers are already working with less than 20% down and still closing on homes.

The timing matters. First-time buyers represented only 24% of all home purchases in 2024, the lowest share since the National Association of Realtors began tracking the figure in 1981. That compression reflects both elevated prices and higher rates, which makes knowing every available rate-reduction strategy more financially consequential than it has been in years. A buyer who pays even 0.5 percentage points more than necessary on a $350,000 mortgage will spend roughly $35,000 more in interest over 30 years.

This guide is for first-time buyers who have a down payment in the 3–10% range and want to close the rate gap with buyers who put down more. By the end, you will know which program choices automatically reduce your rate, how to use lender competition to your advantage, and which negotiations to have with sellers before you finalize a purchase offer.

Key Takeaways

- The median first-time buyer down payment was 9% in 2024, according to NAR data via Bankrate, proof that a sub-20% down payment is the norm, not a disadvantage to overcome.

- Getting four mortgage quotes saves approximately $5,000 over the life of a loan compared to accepting the first offer, per Freddie Mac research, making comparison shopping the single highest-ROI action available to any first-time buyer.

- The FHFA’s automatic first-time buyer discount waives loan-level pricing adjustments worth 0.25–0.375% on eligible conventional loans, potentially saving $15,000–$22,000 in lifetime interest on a $350,000 mortgage with no application required.

- Raising a credit score from the 680s to 740 or above can cut a mortgage rate by 0.5–0.75 percentage points, a far more powerful rate lever than increasing a down payment from 5% to 10%, which saves only about $16/month on a $200,000 loan.

- A Zillow survey covering seven months of 2024 found roughly 45% of buyers obtained a rate below 5% when prevailing rates were above 6.5%, with about one-third achieving this through seller or builder financing concessions.

- The median household income of a typical first-time buyer reached $97,000 in 2024, a jump of $26,000 in two years, according to NAR data via Today’s Homeowner, signaling how much the financial bar has risen and why rate optimization matters more than ever.

In This Guide

- Step 1: Why a Small Down Payment Doesn’t Have to Mean a Higher Interest Rate

- Step 2: How Do I Strengthen My Financial Profile to Get a Better Mortgage Rate?

- Step 3: Which Loan Type Gives First-Time Buyers the Best Rate With a Small Down Payment?

- Step 4: How Do I Shop Lenders and Make Them Compete on Rate?

- Step 5: Can I Negotiate a Rate Buydown From the Seller Without Increasing My Down Payment?

- Step 6: What First-Time Buyer Programs Actually Lower My Interest Rate?

- Step 7: When Is Chasing a Lower Rate at Closing the Wrong Goal?

- Frequently Asked Questions

Step 1: Why a Small Down Payment Doesn’t Have to Mean a Higher Interest Rate

The 20%-down rule is a myth that costs buyers real money. Lenders price mortgage rates based on a combination of four factors: loan-to-value ratio (LTV), credit score, debt-to-income ratio (DTI), and loan type. A low down payment raises the LTV component, but the other three levers remain fully within your control, and together they can close or eliminate the rate gap that a smaller down payment creates.

How Rate Pricing Actually Works

Lenders use a grid of loan-level pricing adjustments (LLPAs) to determine the rate premium added to a base conventional loan rate. An LTV above 80% does trigger a pricing add-on, but so does a credit score below 720. Moving from a 680 credit score to a 760 score can reduce your rate by 0.5–0.75 percentage points, a much larger impact than moving your down payment from 5% to 10%, which typically adjusts the rate by only about 0.125 percentage points. Targeting credit improvement returns more per dollar of effort than saving extra cash for the down payment, in most cases.

What to Watch Out For

The common mistake is treating the down payment as the only variable worth optimizing. Buyers who strain to reach 10% or 15% down while carrying high credit card balances or an installment debt near its limit are often worse off than a buyer who puts down 5%, carries no revolving debt, and holds a 750 credit score. Run the numbers on both paths before deciding where to put your pre-closing savings.

A fair lending principle limits how much individual “negotiation” you can do with a single lender. Lenders cannot legally offer different rates to similarly qualified applicants, so the real strategy is competitive comparison shopping to find the lender whose risk model prices your specific profile most favorably, not asking one lender for a private discount.

Step 2: How Do I Strengthen My Financial Profile to Get a Better Mortgage Rate?

Your credit score is the fastest rate lever you can pull before applying for a mortgage. Crossing the 740 threshold typically moves you into the best conventional pricing tier, while scores in the 620–679 range can add 1.0 percentage point or more to your quoted rate. The good news is that for many buyers, a 60–90 day sprint of targeted credit actions is enough to move one or two tiers.

How to Do This

Start by pulling your credit reports from AnnualCreditReport.com, the only federally authorized free source, and dispute any errors with the relevant bureau, Equifax, Experian, or TransUnion. Then focus on utilization: paying revolving balances below 10% of their credit limits is often the single fastest way to raise a score. If you have a car loan or personal loan near the end of its term, ask your lender whether paying it off early would reduce your DTI enough to shift pricing tiers. Understanding how DTI affects your application approval and pricing is worth reviewing before you apply.

The DTI Tier That Most Articles Skip

Most content says “keep your DTI low” without giving the specific numbers. For conventional loans, a DTI at or below 25% earns the most favorable pricing. Most lenders will approve up to 45–50%, but every tier above 36% typically adds basis points to your rate. A concrete pre-application target: if your monthly gross income is $6,000 and your proposed housing payment would be $1,500, your total monthly debts (including the housing payment) should stay under $1,500 to hit the 25% threshold. That often means paying off a car loan or clearing a credit card before submitting your application.

What to Watch Out For

Do not open new credit accounts, finance furniture, or take on a car loan in the 90 days before applying. Each hard inquiry lowers your score by a small amount, and new installment debt raises your DTI immediately. Many buyers lose ground in the final weeks before application by making purchases they planned to make “anyway.”

Ask each lender you contact for a “rapid rescore” if you’ve recently paid down a balance. Rapid rescoring updates your credit report with a bureau in 3–7 business days rather than the normal 30-day cycle, which can capture a score improvement before your application is submitted.

Step 3: Which Loan Type Gives First-Time Buyers the Best Rate With a Small Down Payment?

Choosing the right loan program is rate negotiation that happens before you contact a single lender. Each program has a different pricing structure, PMI structure, and set of eligibility rules, and for first-time buyers with less than 10% down, the differences in total monthly cost can be substantial. The detailed comparison between FHA and conventional loan costs over time is worth studying before you decide which path to pursue.

How to Do This

Below is a direct comparison of the programs most relevant to first-time buyers with 3–10% down. Rates shown are illustrative spreads relative to a 30-year conventional benchmark as of early 2025; actual figures depend on your lender, credit profile, and market conditions on the day you lock.

| Loan Program | Min. Down Payment | Rate vs. Conventional Benchmark | PMI / MIP Structure | Best For |

|---|---|---|---|---|

| Conventional 97 | 3% | Benchmark (FHFA discount may apply) | Cancellable at 20% equity | Buyers with 720+ credit score |

| Fannie Mae HomeReady | 3% | At or slightly below benchmark | Reduced PMI, cancellable at 20% | Low-to-moderate income buyers |

| Freddie Mac Home Possible | 3% | At or slightly below benchmark | Reduced PMI, cancellable at 20% | Buyers in high-cost or underserved areas |

| FHA Loan | 3.5% | Often 0.10–0.25% below conventional | Upfront 1.75% + annual 0.55–0.85%, lasts loan life if <10% down | Buyers with 580–679 credit score |

| USDA Loan | 0% | Often 0.25–0.50% below conventional | 0.35% annual guarantee fee | Buyers in eligible rural/suburban areas |

| VA Loan | 0% | Typically 0.25–0.50% below conventional | No monthly PMI; one-time funding fee | Active military, veterans, surviving spouses |

The FHFA First-Time Buyer Discount Most Articles Miss

The Federal Housing Finance Agency (FHFA) introduced an automatic pricing adjustment for first-time buyers on conventional loans backed by Fannie Mae or Freddie Mac. For eligible borrowers, this waiver removes LLPAs worth approximately 0.25–0.375% off the effective rate, on a $350,000 loan over 30 years, that translates to roughly $15,000–$22,000 in lifetime interest savings. No separate application is required; you qualify by meeting the definition of a first-time buyer (no ownership interest in a primary residence in the past three years) and by borrowing within conforming loan limits. The critical step: confirm with each lender that they are applying this waiver to your loan estimate, because not every loan officer proactively flags it.

What to Watch Out For

FHA loans have a lower headline rate but carry mortgage insurance premium (MIP) for the life of the loan if you put down less than 10%. For buyers who plan to stay more than five to seven years and can qualify conventionally, FHA’s lifetime MIP usually makes the total cost higher despite the better rate. Use an FHA quote as competitive leverage with conventional lenders, presenting a lower FHA rate gives you a documented benchmark to ask a conventional lender to match or beat, even if you ultimately go conventional.

Moving from a 5% to a 10% down payment on a conventional loan with excellent credit lowers the mortgage rate by only about 0.125 percentage points, saving roughly $16/month on a $200,000 loan. Improving a credit score from the 680s to the 740s, by contrast, can cut the rate by 0.5–0.75 percentage points, saving $65–$100/month on the same loan.

Step 4: How Do I Shop Lenders and Make Them Compete on Rate?

Comparison shopping is the single action with the highest return for a first-time buyer, and most buyers skip it. Freddie Mac research found that getting four mortgage quotes saves approximately $5,000 over the life of a loan compared to accepting the first offer. A large share of first-time buyers still contact only one lender, which means leaving that money on the table is common, not rare.

How to Do This

Collect quotes from at least four sources: a large national bank, a regional bank or local lender, a credit union, and a mortgage broker. Credit unions are particularly underused by first-time buyers; their non-profit structure often produces rates 0.1–0.25 percentage points below commercial banks for the same profile. Mortgage brokers have access to wholesale rates from dozens of lenders and can be especially useful when your profile has any complexity (self-employment income, non-traditional assets, etc.).

Rate shopping does not hurt your credit score the way applying for credit cards does. FICO treats all mortgage inquiries made within a 45-day window as a single inquiry. Submit all your applications within that window so the score impact is counted once, not multiple times.

Making Lenders Compete Directly

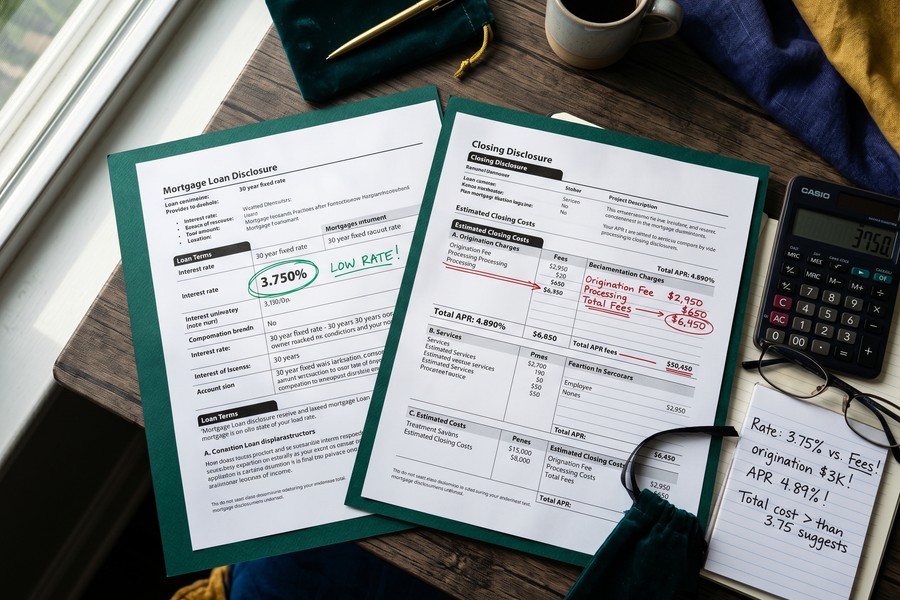

When you have two quotes in hand, call each lender and read the competing offer aloud. Ask specifically: “Can you match this rate and points combination, or can you beat the fees?” Most loan officers have some discretion on origination fees and discount points even when the base rate is set by secondary market pricing. Ask each lender to itemize the Loan Estimate form under RESPA so you are comparing rate, APR, origination charges, and third-party fees on a standard form, not just the headline rate. This process connects directly to how loan term choices also affect total interest cost, which is worth factoring into your comparison.

What to Watch Out For

Comparing only the interest rate without looking at the APR and total origination costs is a common trap. A lender offering a rate 0.125% lower but charging $2,000 more in fees may actually cost you more over five years. Always calculate the break-even point: divide the fee difference by the monthly savings to see how many months it takes to recoup the extra upfront cost.

Some lenders advertise low rates and then add back the cost through elevated origination fees, discount points, or third-party service markups. A Loan Estimate (the standardized three-page document lenders are required to provide within three business days of your application) is the only apples-to-apples comparison tool. Never make a lender decision based on a verbal quote or a mortgage calculator screenshot.

Step 5: Can I Negotiate a Rate Buydown From the Seller Without Increasing My Down Payment?

Yes, and in the market conditions of early 2025, this strategy is more realistic than most buyers realize. Seller-paid temporary buydowns let a seller reduce your effective mortgage rate for the first one to two years of the loan without requiring you to put more money down. A Zillow survey covering seven months of 2024 found that roughly 45% of buyers obtained a mortgage rate below 5% when prevailing rates were above 6.5%, with about one-third achieving this through seller or builder financing concessions. This is not a rare outcome, it is a documented, widely used tool.

How Temporary Buydowns Work

A 2-1 buydown reduces your rate by 2 percentage points in year one and 1 percentage point in year two, then resets to the note rate for the remaining life of the loan. The seller funds the difference between the reduced payment and the full payment into an escrow account at closing. On a $350,000 loan at a 7% note rate, a 2-1 buydown costs the seller approximately $7,000–$8,500, an amount many sellers in a slower market will accept rather than cutting the purchase price, because a price reduction also affects their remaining equity and future comparable sales in the neighborhood.

Permanent Points vs. Temporary Buydowns

Sellers can also contribute concessions that you use to purchase permanent discount points, each point costs 1% of the loan amount and typically buys down the rate by about 0.25%. On a $300,000 loan, one point costs $3,000 and saves roughly $50/month, meaning you break even in 60 months. This makes permanent points the better choice only if you plan to stay in the home more than five years. If you expect to sell or refinance before then, a temporary buydown or a direct price reduction usually produces better value.

To negotiate this effectively, frame the concession as an alternative to a price cut. Many sellers are more willing to contribute $8,000 toward a buydown than to reduce the listed price by $8,000, because the latter affects how the home is recorded in public records and can pull down nearby appraisals. If you want to understand how rate decisions interact with your plans to buy down points, the analysis in whether buying down your rate with points makes sense when home prices are high is directly relevant here.

What to Watch Out For

Temporary buydowns only make sense if you can comfortably afford the full note-rate payment when the buydown period ends. Buyers who can cover year-one payments but not year-three payments should not use this strategy without a clear plan, either a refinance or confirmed income growth to cover the reset payment.

When writing a purchase offer, ask your real estate agent to structure seller concessions as “up to $X toward buyer’s closing costs and/or financing costs.” This broad language gives you flexibility at the closing table to allocate funds toward a temporary buydown, permanent points, or prepaid interest, whichever the lender and market conditions favor at that moment.

Step 6: What First-Time Buyer Programs Actually Lower My Interest Rate?

State and federal programs can produce rate savings that no amount of individual negotiation can match. The most powerful are State Housing Finance Agency (HFA) programs, which offer below-market rates to income-qualified first-time buyers funded by tax-exempt mortgage revenue bonds. In many states, these rates run 0.5–1.0 percentage points below prevailing market rates.

How to Do This

Every state has an HFA, and most offer both a below-market first mortgage and a down payment assistance (DPA) component. To find your state’s program, use the HUD local homebuying programs directory, which links directly to each state agency. Income limits typically range from 80% to 120% of the area median income (AMI), and purchase price limits vary by county. Apply through an HFA-approved lender, not directly through the agency.

Mortgage Credit Certificates and DPA as an Indirect Rate Tool

A Mortgage Credit Certificate (MCC) is a federal tax credit issued by state HFAs that lets you claim 20–25% of your annual mortgage interest as a dollar-for-dollar reduction in federal income taxes. An MCC does not change your stated interest rate, but it reduces the effective cost of borrowing. On a $300,000 mortgage at 7%, the first year generates roughly $21,000 in interest; an MCC at 20% would produce a $4,200 tax credit, effectively lowering your real annual cost as though you were borrowing at a lower rate.

Down payment assistance programs also function as an indirect rate tool: a $10,000 DPA grant that covers your down payment frees cash you could redirect toward purchasing discount points at closing, moving your loan into a better pricing tier, or building the cash reserves that some lenders reward with marginally better pricing. Think of DPA not just as help getting in the door but as capital you can deploy to optimize rate. For buyers still deciding whether homeownership is the right move financially, running the rent-vs.-buy numbers can sharpen the comparison before you commit to a loan strategy.

What to Watch Out For

HFA loans and MCCs come with recapture tax provisions in some states: if you sell within the first nine to ten years and your income has risen significantly, you may owe a portion of the tax benefit back. This is uncommon in practice but worth understanding. Ask your HFA lender for a written explanation of the recapture rules before signing.

Step 7: When Is Chasing a Lower Rate at Closing the Wrong Goal?

Not every first-time buyer should optimize for the lowest possible rate at closing. There are two scenarios where accepting a slightly higher rate is the smarter financial decision, and ignoring them can lead to paying more over your actual holding period than necessary.

Lender Credits vs. Discount Points

The relationship between rate and closing costs is an inverse one: lenders can offer you a credit toward closing costs in exchange for accepting a slightly higher rate, or charge you discount points to lower the rate. If you plan to sell or refinance within five years, taking a lender credit, even at a rate 0.25% higher, often costs less in total than paying points to get the lowest rate. The math is straightforward: if a credit saves you $3,000 at closing but costs $22/month extra in interest, it takes 136 months (over 11 years) to break even. A buyer who moves in year four came out ahead by taking the credit.

PMI Removal as the Better Near-Term Target

For buyers with 5–10% down, private mortgage insurance (PMI) typically adds 0.5–1.5% of the loan amount annually to the monthly payment. On a $350,000 loan, that is $145–$435 per month. Removing PMI by reaching 20% equity, either through appreciation or accelerated principal paydown, can free more monthly cash than shaving 0.25% off the rate at closing. Consider whether directing extra cash toward principal paydown is a higher priority than buying discount points before making the points decision.

The Refinance Exit Ramp

The “marry the house, date the rate” framing is genuinely useful here. If rates drop 1–2 percentage points from where you locked, refinancing into a lower rate becomes financially attractive. The break-even on refinancing costs typically runs 18–30 months at a standard rate drop, so buyers who are confident they will stay long enough to recapture closing costs should plan for a refinance rather than paying heavily for the lowest possible rate today. Understanding whether to wait for rates to drop or lock in now is an important parallel decision to the rate optimization strategies in this guide. Similarly, if you eventually have a co-borrower, knowing how mismatched credit scores affect joint loan pricing helps you plan that step carefully.

What to Watch Out For

The refinance exit ramp is only viable if rates actually fall. Buyers who take on a higher rate expecting to refinance “soon” and then see rates hold flat or rise are stuck with that payment. Build your budget around the rate you lock, treat a future refinance as a bonus, not a plan.

A rate lock duration is itself a silent cost. Lenders price rate locks in 15-day increments, adding roughly 0.125 percentage points for each additional 15-day period. Writing a purchase offer with a 30-day closing timeline rather than 45-day can save basis points without any lender conversation, making the closing date you negotiate in your purchase contract a direct rate tool.

Frequently Asked Questions

Can I get a good mortgage rate with only 3% down as a first-time buyer?

Yes. Programs like Conventional 97, Fannie Mae HomeReady, and Freddie Mac Home Possible allow 3% down and offer competitive rates, especially for buyers with credit scores above 720. The FHFA’s automatic pricing discount for first-time conventional borrowers can also waive LLPAs worth 0.25–0.375%, further reducing the rate without any additional cash down. The bigger rate factor is your credit score and DTI, not the down payment percentage itself.

How much does a credit score improvement actually affect my mortgage interest rate?

Moving from a credit score in the 680s to 740 or above can reduce a conventional mortgage rate by 0.5–0.75 percentage points. On a $300,000 loan, that difference saves roughly $100–$130 per month and over $36,000 over the life of the loan. Most competing articles focus on saving more for a down payment, but credit improvement produces a far larger rate reduction per dollar of effort for most borrowers.

What is the FHFA first-time homebuyer interest rate discount and how do I qualify?

The Federal Housing Finance Agency waives certain loan-level pricing adjustments (LLPAs) for first-time buyers on conventional loans backed by Fannie Mae or Freddie Mac, saving approximately 0.25–0.375% off the effective rate. You qualify if you have had no ownership interest in a primary residence in the past three years and your loan is within conforming limits. No separate application is required, but you should explicitly ask each lender to confirm they are applying the waiver to your Loan Estimate.

Should I use an FHA loan or a conventional loan if I have a 650 credit score and 5% down?

At a 650 credit score with 5% down, an FHA loan will likely offer a lower headline rate than conventional, typically by 0.10–0.25 percentage points. However, FHA mortgage insurance premium (MIP) lasts for the life of the loan if you put down less than 10%, adding roughly 0.55–0.85% annually to borrowing costs. For buyers who plan to stay more than seven years, the lifetime MIP often makes the total cost higher than a conventional loan with cancellable PMI, even at a slightly higher rate. Comparing both options side-by-side using APR, not just the stated rate, is the most reliable way to decide. For a full cost comparison, see FHA vs. conventional rates over time.

How do I ask a seller to pay for a rate buydown without killing the deal?

Frame the request as a concession in lieu of a price reduction: “Rather than lowering the price by $8,000, we’d like the same value applied to closing costs and financing assistance.” Most sellers respond better to concessions than price cuts because a price reduction affects their recorded sale and local comparables. A 2-1 buydown on a $350,000 loan typically costs the seller $7,000–$8,500 and reduces your rate by 2 full percentage points in year one, making it a meaningful benefit you can quantify in the offer conversation.

How many mortgage lenders should I contact to get the best rate?

At least four. Freddie Mac research found that getting four quotes saves approximately $5,000 over the life of a loan compared to accepting the first offer. Include at least one credit union in the mix, as their non-profit structure often produces rates 0.1–0.25 percentage points below commercial banks. Submit all applications within a 45-day window to limit the credit score impact to a single hard inquiry.

What DTI ratio do I need to qualify for the best first-time buyer mortgage rate?

A DTI at or below 25% earns the most favorable pricing on conventional loans. Most lenders will approve DTIs up to 45–50%, but each tier above 36% typically adds basis points to your rate. A practical pre-application target: if your gross monthly income is $6,000, your total monthly debt payments (including the proposed housing payment) should stay below $1,500 to hit the 25% threshold.

Does my rate lock period affect my mortgage interest rate?

Yes. Lenders price rate locks in 15-day increments, adding roughly 0.125 percentage points for each additional 15-day period beyond the base lock. Writing a purchase offer with a 30-day closing instead of a 45-day closing can therefore save basis points with no lender negotiation at all, a strategy almost no first-time buyer resource explains. If market conditions make a longer lock necessary, ask whether a “float-down option” is available, which lets you capture a lower rate if rates fall before closing, sometimes without an added fee.

Are there first-time buyer programs in every state that reduce mortgage rates?

Yes. Every state has a Housing Finance Agency offering below-market rate mortgages funded by tax-exempt bonds, often running 0.5–1.0 percentage points below prevailing rates for income-qualified buyers. To find your state’s program, use the HUD local homebuying programs directory. Many state programs also offer Mortgage Credit Certificates and down payment assistance, which can be combined with the below-market rate to reduce total borrowing costs significantly.

Should I lock my mortgage rate now or wait for rates to drop?

There is no reliable way to time mortgage rate movements, and waiting carries real risk: home prices may rise while rates hold flat, or rates may increase before falling. The better strategy is to lock a rate you can afford, use the tools in this guide to reduce it as much as possible before locking, and plan for a refinance if rates drop 1–2 points during your holding period. For a detailed analysis of this decision, see whether to wait for rates to drop or lock in now and the related discussion of when to lock vs. float when the Fed signals a pause.