Reviewed by the CapitalLendingNews Editorial Team

Our Take

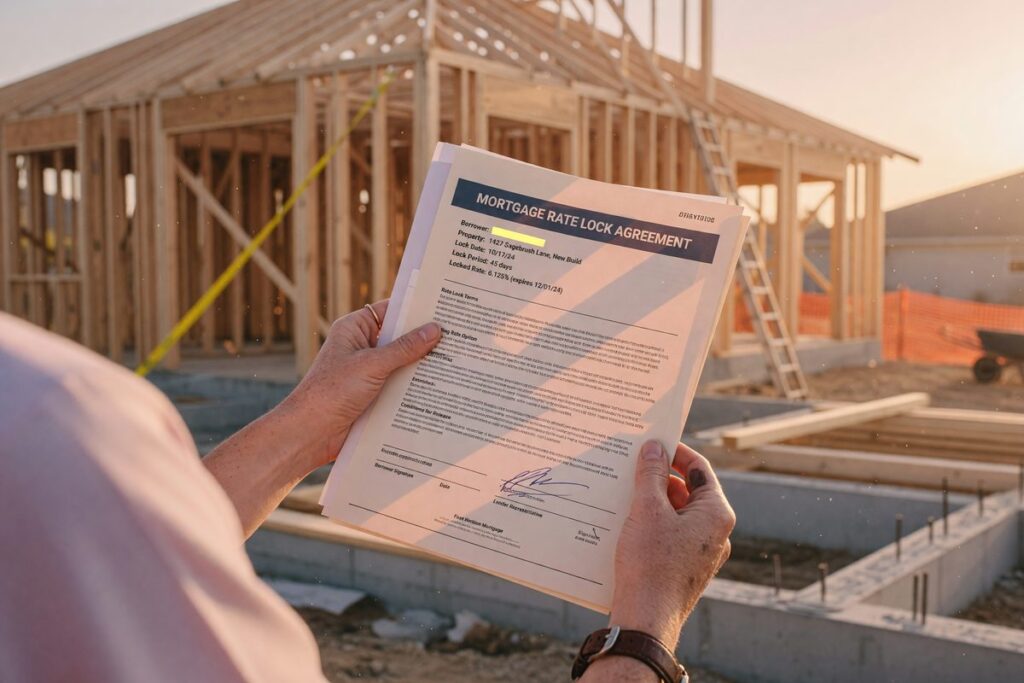

Repeat buyers building a new home should lock their rate at contract signing using a 270- to 360-day extended lock on a construction-to-permanent loan, not wait until the home nears completion. The fee premium (typically 0.25%–0.75% of the loan amount) is worth paying in a volatile rate environment where average construction timelines run 9.1 months. The case against it: if rates fall significantly and your float-down provision has restrictive eligibility rules, you may overpay relative to someone who floated longer. That risk is real but secondary for buyers who cannot absorb a 50- to 100-basis-point rate increase mid-build.

Mortgage rates have remained elevated and volatile through early 2026, and builders are delivering homes on timelines that would have seemed long even five years ago. According to the National Association of Home Builders’ 2025 construction data, single-family homes averaged 9.1 months from start to completion in 2024. That is more than double the coverage window of a standard 30-to-60-day rate lock.

This article is for repeat buyers who already know how mortgages work but have not navigated a new-construction purchase before. The recommendation holds well for buyers using construction-to-permanent financing; it gets more complicated when builder-preferred lender programs enter the picture, and I will explain exactly where that line sits.

Key Takeaways

- 9.1 months is the average single-family construction timeline in 2024, according to NAHB Eye on Housing, making standard 30-to-60-day rate locks structurally inadequate for new builds.

- The CFPB defines a rate lock as a guarantee the rate will not change before closing provided the loan closes within the lock period and the application has not materially changed, a condition repeat buyers carrying a prior home’s equity often inadvertently violate.

- Lenders including Bank of America and CrossCountry Mortgage advertise construction-to-permanent locks of up to 12 months, typically priced at a 0.25%–0.75% rate premium or equivalent fee over a standard 30-day lock.

- From permit issuance to completion, the average build ran 7.6 months for homes built for sale in 2024, per NAHB, meaning even buyers who lock at permit stage are cutting the timeline close with a 180-day lock.

- In my experience reviewing construction loan scenarios, buyers who roll equity from a sale into the new build often underestimate how that equity event can trigger application changes that void an existing lock mid-construction.

Why Standard Rate Locks Fall Short for New Builds

A 30-day or 60-day lock is designed for resale transactions: the home exists, appraisals are quick, and closing happens in weeks. New construction does not work that way. From the day you sign a purchase contract to the day you close, NAHB data shows the median gap runs 7.6 months for homes built for sale, and custom builds stretch longer. A standard lock expires long before the certificate of occupancy arrives.

The financial exposure is not abstract. Say you lock at 6.75% in June 2026 on a $450,000 loan with a 60-day lock, expecting to close in August. Construction delays push closing to December. Your lock expired in August, and current rates have moved to 7.25%. That 0.50% difference adds roughly $150 per month to your principal and interest payment, or about $1,800 in the first year alone. On a 30-year loan, the total interest difference exceeds $54,000. That is the arithmetic most repeat buyers do not run until the lock is already gone.

What I see in practice: Repeat buyers routinely assume the process mirrors their prior purchase, where a 45-day lock was more than enough. They sign the construction contract, do nothing about locking for months, and suddenly face an expiring commitment letter with a half-built home. The delay does not feel urgent until rates move.

The solution is a construction-to-permanent loan with an extended lock at or before groundbreaking. This is not exotic financing. It is a single loan that covers the construction draw period and then converts to a permanent mortgage at the same locked rate. The rate lock new construction buyers need is attached to the permanent loan phase, not the construction phase alone.

When Repeat Buyers Lock In, and Why It’s Usually Too Late

Most experienced homebuyers instinctively wait to lock until the loan is close to funding. That instinct is correct for resale. For new construction, it is wrong in a way that costs money.

The myth is that you cannot or should not lock until the home is near completion. In reality, construction-to-permanent loans let you lock at application or at contract signing, sometimes even before permits are pulled. Lenders offering 270- to 360-day locks are specifically underwriting the risk that your build will take close to a year. You pay a premium for that coverage window, but you pay it once. Waiting six months and then scrambling for a last-minute 30-day lock at whatever rate the market is offering that week is the more expensive gamble.

Repeat buyers carrying a prior home’s equity face an additional wrinkle. If you are selling your current home to free up a down payment and the sale closes mid-construction, that transaction changes your financial profile. According to the CFPB’s guidance on rate locks, a lock holds only if there are no material changes to the application. A large equity event, a shift in your debt-to-income ratio after the sale, or a change in employment status can all trigger a lock voiding or repricing event at exactly the wrong moment. This is a scenario most general articles on rate locks do not address, and it catches repeat buyers off guard.

The Real Cost of Extended Rate Locks in 2026

Extended locks are not free, and the pricing deserves a direct look before you commit.

| Lock Period | Typical Rate Premium (bps) | Upfront Fee (on $450K loan) | Break-Even Rate Rise |

|---|---|---|---|

| 30 days | 0 bps (baseline) | $0 | N/A |

| 90 days | 12–18 bps | $540–$810 | ~0.12% |

| 180 days | 25–38 bps | $1,125–$1,710 | ~0.25% |

| 270 days | 38–55 bps | $1,710–$2,475 | ~0.38% |

| 360 days | 50–75 bps | $2,250–$3,375 | ~0.50% |

The break-even column is the key figure. A 270-day lock priced at 38 basis points pays for itself the moment rates rise by more than that amount before your closing. If rates climb 50 basis points, you are ahead on day one of your permanent loan. The fee is also often financed into the loan or reflected as a rate premium rather than cash at closing, which matters for buyers who are already stretching for a down payment.

Where this gets tricky: Some lenders structure the extended lock fee as a non-refundable deposit that is credited at closing, but only if you close with that lender. If you walk away or the builder fails to deliver, you lose it. Always clarify refund terms before paying.

Comparing this to a temporary builder buydown is instructive. Builder-funded 2-1 buydowns (common in 2024 and still offered selectively in 2026) reduce your rate by 2% in year one and 1% in year two, then reset to the note rate. That can lower monthly payments early but does nothing to protect you if rates rise after the buydown period expires. An extended lock and a buydown solve different problems. For a buyer uncertain about long-term rate direction, understanding how fixed versus step-rate products perform in different rate environments can clarify which structure fits your timeline better.

Float-Down Provisions Most Experienced Buyers Ignore

A float-down option lets you capture a lower rate if the market drops after you lock. Most extended construction locks include one. Almost nobody uses it correctly.

The standard float-down clause allows one rate adjustment, triggered only if rates fall by a minimum threshold (often 0.25%–0.50%), and only during a defined window before closing. The borrower typically must request the adjustment proactively; lenders do not alert you that you qualify. In practice, buyers lock in June, rates dip in October, and they close in December without ever asking whether the float-down applied. By the time they realize, the window has closed.

Bank of America’s construction-to-permanent product and similar programs at CrossCountry Mortgage both advertise float-down features on extended locks. The eligibility rules vary: some require that rates fall by at least 50 basis points from the locked rate; others measure the drop against current market rates on a specific pricing date. Read the actual lock agreement before signing, and set a calendar reminder at the midpoint of your lock period to check whether rates have dropped enough to qualify. That one check could be worth hundreds of dollars per year.

Builder Lender Programs vs. Your Own Bank

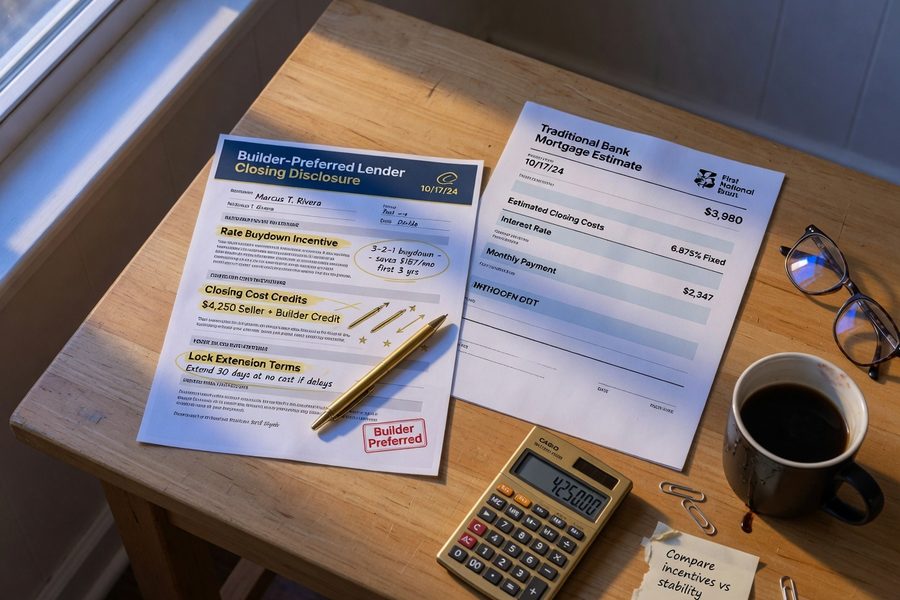

Builder-preferred lenders offer real incentives, closing cost credits, free lock extensions, rate buydowns, that can look compelling on a worksheet. The tradeoff is structural, not just financial.

When a builder’s preferred lender offers a free 360-day lock or a 2-1 buydown worth $8,000 in closing credits, those incentives are baked into the home price or the loan’s back-end pricing. The note rate may sit 0.125%–0.375% above what an independent lender would offer the same borrower. On a $450,000 loan, that spread costs roughly $38–$112 per month and compounds over a 30-year term into a meaningful gap. Some buyers correctly calculate that the upfront credit exceeds the long-run premium. Others take the credit and forget to run the arithmetic.

Repeat buyers with equity from a prior sale also face a qualification difference. If your current home has not yet sold, the preferred lender’s DTI calculation may treat the departing residence more conservatively than a portfolio lender would. That can affect how much new-construction home you qualify for while carrying two properties. For context on how income variables affect mortgage qualification, this breakdown on how lenders treat overtime and bonus income illustrates how small underwriting differences compound into real qualification outcomes. Similarly, understanding how credit score bands affect the rate you’re quoted is worth reviewing before comparing builder-lender offers side by side.

Where This Recommendation Falls Short

The case for locking early and long is strong in a flat-to-rising rate environment. It is a genuine drawback in an environment where rates fall sharply after you lock, and the float-down threshold never triggers.

Here is the catch: float-down provisions have floors. If rates drop 0.30% but your float-down requires a 0.50% decline, you absorb the full cost of the extended lock and receive none of the benefit of lower market rates. Buyers who locked 12-month construction rates in mid-2023 and closed into falling rates in 2024 felt this directly. They paid premiums for coverage that protected them from a rate increase that never came, and their float-down clauses did not trigger because the drop was not large enough.

The risk is also asymmetric depending on your income profile. If your rate sensitivity is lower because you have a large down payment and strong cash flow, absorbing a 0.375% premium on an extended lock is less painful than it would be for a buyer stretching to qualify. For buyers whose DTI is already at the edge, the lock premium adds to monthly obligations and can affect qualification for the permanent loan at conversion. That interaction between the lock cost and DTI is something most rate lock articles skip entirely.

The recommendation also does not hold equally well for buyers using a construction-only loan (draw loan) followed by a separate permanent mortgage at completion. That two-close structure means you cannot lock the permanent rate until construction ends, which eliminates the extended lock strategy entirely. In that scenario, the question becomes whether to use a fixed or adjustable rate on the permanent loan based on how long you plan to hold the home, not when to lock.

Finally, the current rate environment matters. As of Q3 2025, roughly 20.0% of outstanding U.S. mortgages still carried rates below 3%, which means a large cohort of existing homeowners has little financial incentive to sell, building into tighter resale inventory and potentially faster new construction demand. Whether that dynamic sustains or shifts between now and late 2026 is the macro variable that most affects whether an extended lock proves necessary or expensive. No one can predict that with certainty, which is exactly why the lock premium exists.

How We Sourced This

This article draws primarily from NAHB’s Eye on Housing construction timeline data for 2024 (published September 2025), CFPB’s official guidance on rate locks, and Realtor.com’s Q3 2025 outstanding mortgage analysis citing the FHFA National Mortgage Database. Lender product details for Bank of America and CrossCountry Mortgage were sourced from publicly available product pages and program disclosures reviewed in May–June 2026. Rate premium ranges in the comparison table are derived from lender rate sheets and published program disclosures available; specific pricing varies by loan size, credit profile, and market conditions. No statistics were extrapolated or invented; any figure that could not be verified against a named source is stated qualitatively.

Related reading: Repeat Homebuyers in Texas and Florida Get Lower Rates: Here’s Why.

Frequently Asked Questions

Can you lock a mortgage rate before construction begins on a new home?

Yes. Construction-to-permanent loans allow borrowers to lock the permanent rate at application or contract signing, before a single foundation wall is poured. This is the primary advantage of a one-close construction loan over a two-close structure, where locking must wait until the build is complete.

How long does a rate lock need to be for new construction?

At minimum, your lock should match the expected construction timeline plus a 30-to-60-day buffer for closing delays. Given that NAHB reports average build times of 9.1 months in 2024, most buyers building a single-family home need a 270-to-360-day lock to avoid expiration risk. A 180-day lock is adequate only for smaller production homes with confirmed fast-track schedules.

What happens if my rate lock expires before my new construction home closes?

Your lender will reprice your loan at current market rates, which may be higher than your original lock. Some lenders offer extensions for a fee, typically 0.15%–0.375% of the loan amount per 30-day extension. If rates have risen substantially, the repriced payment may push your DTI past the lender’s qualification threshold, creating both a rate problem and an approval problem simultaneously.

Are builder lender programs ever the better choice for rate locks?

Sometimes. When a builder’s preferred lender offers a free 12-month lock extension or a funded 2-1 buydown worth more than the rate premium embedded in the offer, the math can favor the builder program. The right move is to get a competing quote from an independent lender, strip out all incentive credits, and compare the all-in cost over your expected holding period. Buyers who plan to refinance within a few years if rates fall may also find the builder program’s upfront credits worth accepting a slightly higher note rate.

Does selling my current home mid-construction affect my locked rate?

It can. The CFPB’s guidance is clear that a rate lock holds only when there are no material changes to the loan application. A large proceeds event from selling your current home can alter your asset picture, shift your DTI, or trigger re-underwriting requirements. Tell your loan officer in advance when you expect the prior home to close, and confirm in writing that the equity event will not constitute a material application change requiring a new lock.