Reviewed by the CapitalLendingNews Editorial Team

Our Take

For most single parents carrying high-interest debt with little or no emergency cushion, the right fintech strategy is to build both simultaneously, not sequentially. A $500–$1,000 starter emergency fund should come first, funded through automated micro-savings tools like round-ups or paycheck splits, while maintaining minimum debt payments. Only after that starter fund exists should extra income go toward accelerated payoff. The case for debt-first is real: high-APR balances compound fast. But for single-income households, a single car repair without any buffer pushes you straight back onto a credit card, erasing weeks of payoff progress.

Single parents are facing a documented savings gap that has barely budged in years. According to the FDIC’s 2024 research on single-parent financial resilience, only 55 percent of single parents had saved for unexpected expenses or emergencies, compared to almost two-thirds of all households. That gap is not a discipline problem. It is a structural one: single parents absorb both the income risk of one earner and the expense volatility of caring for children alone, and traditional bank tools were never built to address both pressures at once. Fintech emergency fund strategies built for single parents are now closing that gap in ways that standard checking accounts simply cannot.

This article is for single parents who carry at least one active debt and have under three months of expenses saved. What makes the recommendation work is automation, the best fintech platforms remove the decision point entirely, moving money into savings and toward debt before it can be spent elsewhere. What makes it not work is choosing the wrong platform, misreading fee structures, or treating automation as a substitute for adjusting when income shifts.

Key Takeaways

- Only 55% of single parents had emergency savings in 2024, versus nearly two-thirds of all U.S. households, according to FDIC 2024 data.

- More than two-thirds of single parents already access their bank account primarily through mobile banking, per the same FDIC report, meaning fintech adoption is not the barrier; the right product selection is.

- Just over half of single parents used nonbank peer-to-peer apps like PayPal, Venmo, or Cash App in the prior 12 months, per FDIC 2024, those tools rarely help build savings or reduce debt interest.

- Nationally, only 55% of U.S. adults had set aside three months of expenses in an emergency fund in 2024, per the Federal Reserve’s 2025 Economic Well-Being report, single parents trail even this already-low national benchmark.

- In my read of this space, the single most underused fintech feature among single parents is paycheck-split automation, not round-ups, because it moves meaningful amounts before spending decisions are made.

The Financial Pressure Single Parents Actually Face in 2026

Here’s the thing: most debt and savings advice assumes a two-income buffer that single parents simply do not have. A job loss, a sick child, or a car transmission failure is a catastrophic event for a solo-income household in a way it is not for a dual-income family with even modest savings. This is the structural reality that makes fintech emergency fund planning so critical for single parents specifically.

The FDIC’s 2024 data highlights this clearly. Single parents trail all households in emergency savings, and the disparity is sharpest in lower-income brackets, nearly 60% of Black and Hispanic single-parent households earn under $30,000 annually, a threshold at which traditional bank savings products offer almost nothing useful. High minimum balances, low or zero APY on standard savings, and overdraft fees that trigger when paycheck timing shifts all work against this demographic.

Why Irregular Income Compounds the Problem

Many single parents work gig shifts, seasonal jobs, or part-time hours that don’t produce steady biweekly paychecks. If you’re in that situation, the standard advice to “automate a fixed transfer on payday” breaks down immediately. The fintech tools that actually solve this problem are the ones built to handle variable income, percentage-based rules instead of fixed dollar amounts, or conditional transfers that only trigger when a balance threshold is met. Our piece on digital lending for gig workers during income gaps covers this dynamic in more detail, but the savings side of the equation follows the same logic.

What I see in practice: Readers who work irregular hours often set a fixed $25 weekly transfer and then cancel it during a slow month, then never reinstate it. Percentage-based rules eliminate that friction entirely. If the paycheck is small, the transfer is small. The habit stays intact without requiring a manual decision.

Should You Build the Emergency Fund First or Attack the Debt?

Build a starter emergency fund first, even a small one, before directing extra money toward debt. This is the defensible position for single parents, and here is the arithmetic that supports it.

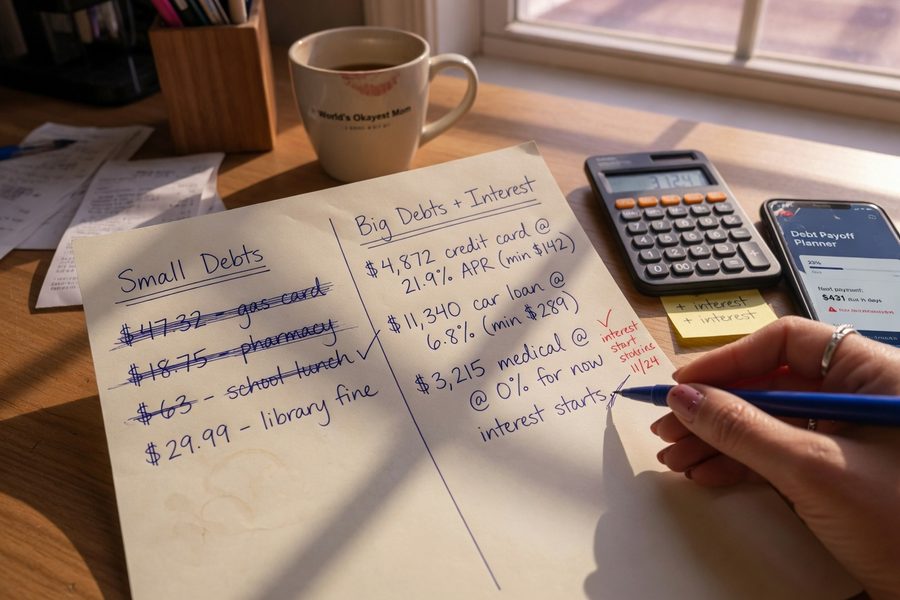

Say you’re carrying $4,000 in credit card debt at 22% APR and have zero savings. You redirect $100/month to extra debt payments: that saves you roughly $880 in interest over three years and pays it off about 14 months early. But one $600 car repair sends you back to the card. Now you owe $4,600, and those 14 months of progress are erased in a single afternoon. A $500–$1,000 emergency buffer, built first, through automated micro-savings over two to three months, makes the debt payoff strategy actually stick.

The Consumer Financial Protection Bureau puts it directly: “Setting up a dedicated savings or emergency fund is one essential step to prepare for unplanned expenses or financial emergencies and avoid turning to credit cards or loans that can lead to harder-to-pay-off debt.” For single parents, that point is not theoretical.

Debt Snowball vs. Debt Avalanche for Solo Households

Once the starter fund exists, the avalanche method, highest interest rate first, is mathematically superior. But the snowball (smallest balance first) has a real psychological advantage for single parents who are managing everything alone and need visible wins to stay motivated. Some fintech platforms now build hybrid trackers that show both the mathematical payoff date and the motivational milestone progress side by side. That dual view is worth looking for when choosing a platform. For a deeper look at how loan term length controls total interest cost, that framing applies directly to debt payoff sequencing decisions.

Fintech Tools That Automate Savings Without Requiring Willpower

The best fintech tools for this goal share one design principle: they move money before the account holder sees it. Round-up apps like Changed redirect the spare change from everyday purchases, say, rounding a $3.60 coffee to $4.00, into either a savings bucket or directly toward a debt. The amounts are small per transaction, but they compound. A household making 15 purchases per day at an average $0.30 round-up accumulates roughly $135/month without a single deliberate savings decision.

Paycheck-split automation, available through platforms like Chime, Current, and several neobanks built specifically for variable-income households, is more powerful. It routes a defined percentage of each direct deposit into a separate FDIC-insured savings account before the spendable balance is ever displayed. For a single parent earning $3,200/month, routing 5% automatically builds $160/month toward an emergency fund, roughly $1,920 over a year, without occupying a single minute of mental bandwidth.

What clients often miss: The “savings rate” shown in many fintech apps reflects interest earned, not contribution rate. I’ve seen readers feel good about a 4.5% APY and ignore the fact that they’re only contributing $10/month. APY matters after the balance exists; contribution rate is what builds it.

What to Look for in the Account Itself

FDIC insurance is non-negotiable. So is instant or same-day access, a true emergency fund locked behind a 3-business-day transfer window is not an emergency fund; it is a savings account. Look for platforms offering APYs above 4.0% on savings buckets (competitive as of mid-2026), zero monthly maintenance fees, and no minimum balance requirement. Several neobanks now offer all four. Traditional savings accounts at major banks still average well below that threshold.

How the Best Fintech Platforms Handle Debt Payoff Alongside Savings

Dual-goal automation is now table-stakes for serious fintech platforms. The differentiation is in the details: how they handle multiple debt types, how they surface progress, and whether they integrate with external accounts or only their own.

| Feature | Basic Fintech App | Dedicated Debt + Savings Platform |

|---|---|---|

| Savings APY | 0.5%–2.0% | 4.0%–5.0% |

| Round-up to debt | No | Yes (Changed, Qoins) |

| Paycheck split automation | Fixed dollar only | Percentage-based, variable income-ready |

| Debt tracker (external accounts) | No | Yes, credit cards, medical, student loans |

| Monthly fee | $0 | $0–$8 |

| Emergency fund bucket (separate from checking) | Rarely | Yes, instant-access |

What we tell readers in this situation: the $0 fee is appealing until you realize a basic app earning 0.8% APY on a $1,500 emergency fund is generating about $12/year, while a dedicated platform earning 4.5% returns $67.50 on the same balance. Over 24 months, that difference funds another half-month of grocery spending. It adds up. If you’re already evaluating whether to refinance existing debt, our overview of when digital loan refinancing actually saves money pairs directly with this platform selection question.

Combining Savings and Debt Goals on One Platform: What Actually Works

The strategy that holds up for single parents with irregular income is a two-bucket rule: every deposit, regardless of size, splits automatically, a fixed percentage to the emergency fund until it hits a target (say, $1,000), then that same percentage redirects to debt overpayment once the target is reached.

Platforms that allow conditional rules, “if emergency fund balance is below $1,000, route 5% here; if above, route 5% there”, eliminate the rebalancing decision entirely. That matters for solo parents who do not have a partner to share financial management tasks with. The single most common failure point we see is manually adjusting rules during a busy week, forgetting to restore them, and letting the savings habit lapse for months.

“Setting up a dedicated savings or emergency fund is one essential step to prepare for unplanned expenses or financial emergencies and avoid turning to credit cards or loans that can lead to harder-to-pay-off debt.”

Pitfalls That Can Quietly Undermine Your Progress

Here’s the thing: the fintech platforms most aggressively marketed to people in debt are often the least aligned with this dual-goal strategy. Debt settlement apps in particular, which promise to negotiate balances down, typically require you to stop paying creditors while accumulating funds, which destroys credit scores and can trigger lawsuits. That is the wrong tool for a single parent who needs credit access in an emergency. Look for apps that support active debt payoff, not suspension of it.

Fee structures deserve scrutiny before signup. Some savings features that look free carry a monthly subscription after a trial period. Others charge for instant transfers, which defeats the purpose of an emergency fund. Data privacy is also a real concern: linking bank accounts, payroll providers, and multiple debt accounts creates a consolidated financial profile. Before connecting accounts, it is worth checking a platform’s data-sharing policy, specifically whether they sell aggregated financial behavior data to third parties. Our piece on what happens to your data after a digital loan closes covers the retention side of this concern in more detail.

Where this gets tricky: Single parents who rely on SNAP, WIC, or housing assistance sometimes worry that savings account balances affect benefit eligibility. In most cases, FDIC-insured accounts used for emergency savings are excluded from asset tests for major federal programs, but state-level rules vary. Verify with your local benefits office before aggressively building a balance.

Where This Recommendation Falls Short

The drawback of the “build savings and pay debt simultaneously” approach is real: every dollar going into a savings account earning 4.5% APY is a dollar not reducing a credit card balance charging 22% to 29% APR. The math is unambiguous. If your debt is high-interest and your income is stable enough that an emergency is unlikely to require immediate cash access, the pure debt-first strategy does save more money over time.

The tradeoff gets sharper for single parents in specific circumstances. If you have family nearby who could absorb a one-time emergency cost, a parent who could lend $500 for a car repair without strings, then the case for putting every extra dollar toward debt first is stronger. The emergency fund is partly insurance against isolation; if you have a genuine safety net in your personal network, you can weight the calculation differently.

There is also a real risk here with automation: it assumes your income and expenses stay roughly stable. A custody arrangement change, a child aging into a more expensive healthcare tier, or a shift from salaried to gig work can all break the logic of a set-and-forget rule. The catch is that fintech automation feels permanent once configured, many users do not revisit settings for 12 to 18 months. This platform calculates as if your life in month one is your life in month eighteen. It is not. Review your automation rules every six months, minimum.

Finally, this recommendation is not for everyone carrying debt. If you are behind on rent or utilities, or carrying any debt that is already in collections, the debt-or-savings question is secondary to stabilizing current obligations. Fintech micro-savings tools are designed for people who are current on their bills but not yet ahead of them. If you are in a more acute financial crisis, a nonprofit credit counselor through the National Foundation for Credit Counseling is a better first step than any app.

How We Sourced This

This article draws primarily from the FDIC’s 2024 single-parent financial resilience report (published at fdic.gov), the Federal Reserve’s 2025 Report on the Economic Well-Being of U.S. Households covering 2024 data, and the CFPB’s emergency fund guide. Platform feature comparisons reflect publicly available product documentation for Changed, Qoins, Chime, and Current as of May–June 2026; specific APY ranges represent competitive benchmarks from those platforms’ published rates and may shift with Federal Reserve policy changes. Fee and feature data was verified directly against each platform’s current terms of service. Arithmetic examples in the article use exact figures drawn from cited statistics; derived calculations were independently checked for internal consistency before publication.

Related reading: 3 Advanced Tactics for Paying Off $20K+ in Medical Debt.

Frequently Asked Questions

Can a single parent realistically build an emergency fund while paying off debt at the same time?

Yes, but the sequencing matters. Build a starter emergency fund of $500 to $1,000 first using automated micro-savings, while maintaining minimum debt payments. Once that buffer exists, redirect additional dollars to debt overpayment. Doing both simultaneously from the start, without any starter cushion, usually collapses when the first unexpected expense hits.

What fintech features matter most for single parents with irregular income?

Percentage-based savings rules matter far more than fixed-dollar transfers for variable-income households. Look for platforms that calculate savings contributions as a percentage of each deposit rather than a fixed weekly amount, this means a $900 paycheck and a $2,100 paycheck both contribute proportionally, and the automation survives slow months without manual cancellation. Instant access to the saved funds is equally non-negotiable.

Are fintech savings accounts FDIC-insured?

Most reputable fintech savings products are FDIC-insured, but through a partner bank, not the fintech company itself. Confirm the specific bank partner and verify the insurance coverage limit before depositing. The standard FDIC limit is $250,000 per depositor per institution, which covers the emergency fund balances typical single parents hold.

Will building a savings account balance affect my government benefits?

For most major federal programs, including SNAP, Medicaid, and CHIP, emergency savings accounts are either excluded from asset tests or covered by state-level exemptions. State-administered programs vary, so verify your specific situation with a local benefits counselor before aggressively growing your balance. The concern is legitimate, but for most single parents using these programs, a $1,000 emergency fund does not create a benefits risk.

How do I choose between a debt-focused fintech app and a savings-focused one?

If you are carrying high-interest debt (above 18% APR), prioritize a platform that handles both goals, look specifically for round-up-to-debt features and external debt account integration, not just a savings bucket. If your debt is lower-interest (student loans at 5–7%, for example), a high-APY savings-first platform makes more sense. Our breakdown of paying off a personal loan versus building a savings portfolio covers the rate threshold decision in more detail.

Sources

- FDIC, Single Parents: Financial Resilience, Banking, and Mobile Technology (2024)

- Federal Reserve, Report on the Economic Well-Being of U.S. Households in 2024: Savings and Investments (2025)

- Consumer Financial Protection Bureau, An Essential Guide to Building an Emergency Fund

- National Foundation for Credit Counseling, Find a Nonprofit Credit Counselor

- Capital Lending News, Digital Lending for Gig Workers Between Contracts: How to Borrow During Income Gaps

- Capital Lending News, Digital Loan Refinancing: When a Rate Drop Actually Saves Money (and When It Doesn’t)

- Capital Lending News, What Happens to Your Data After a Digital Loan Closes: A 7-Year Reality

- Capital Lending News, Should You Pay Off a Personal Loan or Build an Investment Portfolio First?

- Capital Lending News, How Loan Term Length Quietly Controls How Much Interest You Actually Pay