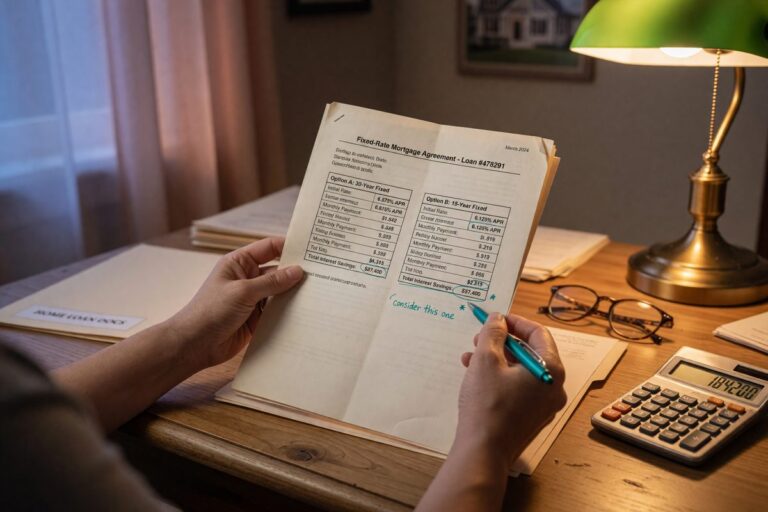

How a Balloon Payment Mortgage Exposes Borrowers to a Rate Shock at Maturity

When a balloon mortgage matures, 80–90% of your original balance comes due at once—and refinancing at higher rates can raise your monthly payment by $600 or more.

When a balloon mortgage matures, 80–90% of your original balance comes due at once—and refinancing at higher rates can raise your monthly payment by $600 or more.

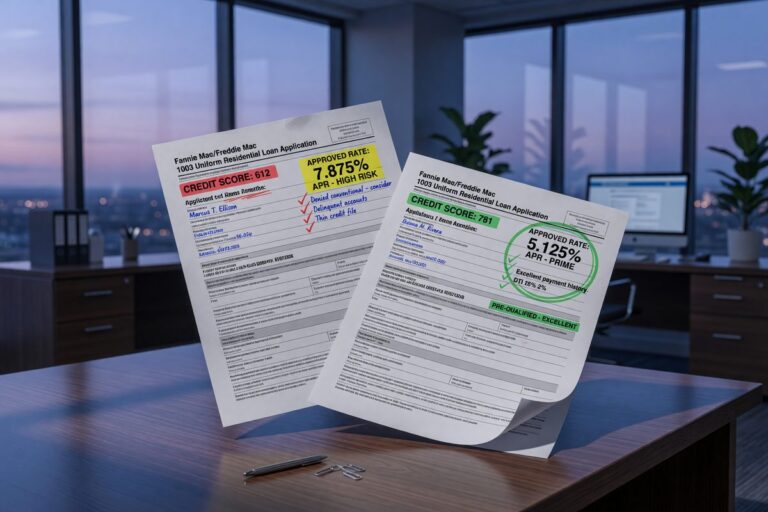

A 630 credit score co-borrower can raise your mortgage rate by 0.25–0.75%, costing $130–$200 monthly on a $400K loan. See when adding them actually makes sense.

Unsecured loans average 12–21% APR vs 7–9% for secured loans — a gap that can cost thousands over five years. Here's how to choose the structure that actually saves you money.

Bridge loans typically run 8.5%–12.5% annually—up to 4 points above prime. Here's what move-up buyers need to understand before juggling two closings.

Unemployment can push personal loan rates from 12.31% to 36%—or trigger outright denial. Here's how lenders reprice risk when your income disappears.

Nurses and teachers can cut their mortgage rate by 0.25%–0.50% or land up to $10,000 in down payment grants through programs like HUD's Good Neighbor Next Door.

Condo mortgage rates typically run 0.125%–0.75% higher than single-family loans — HOA instability and Fannie Mae eligibility rules explain exactly why.

Lenders require a 24-month history before side income counts toward your mortgage — without it, that extra money is invisible to underwriters and won't lower your rate.

Rural property buyers missing USDA loan eligibility could be paying 1.5% more in interest—costing tens of thousands over the loan term. Here's what you need to know.

Fixed-rate mortgages shield retirement budgets from payment shock, while ARMs can spike 30–50% under lifetime caps. See which structure fits your fixed income.