Winter Homebuyers Get 0.125%–0.25% Lower Mortgage Rates: Here’s Why It Works

Winter homebuyers lock in 0.125%–0.25% lower mortgage rates on average, plus 4–8% cheaper home prices. See how seasonal timing and Freddie Mac data prove the edge is real.

Winter homebuyers lock in 0.125%–0.25% lower mortgage rates on average, plus 4–8% cheaper home prices. See how seasonal timing and Freddie Mac data prove the edge is real.

Bond markets move multiple times daily, and your mortgage rate quote can vanish within hours without a formal lock. A 0.125% rate increase costs $900 more on a $300k purchase—here's how to protect yourself.

Most widowed homeowners can preserve sub-4% rates through loan assumption instead of refinancing—no credit check or income verification required. Here's when it works.

At 6%+ rates, a 15-year mortgage saves $263,000 in interest but costs $728 more per month. See the trade-offs and find your optimal term.

Save $12,000 in the first five years with an interest-only mortgage—but only if the rate premium stays below 0.5% and you invest the payment difference.

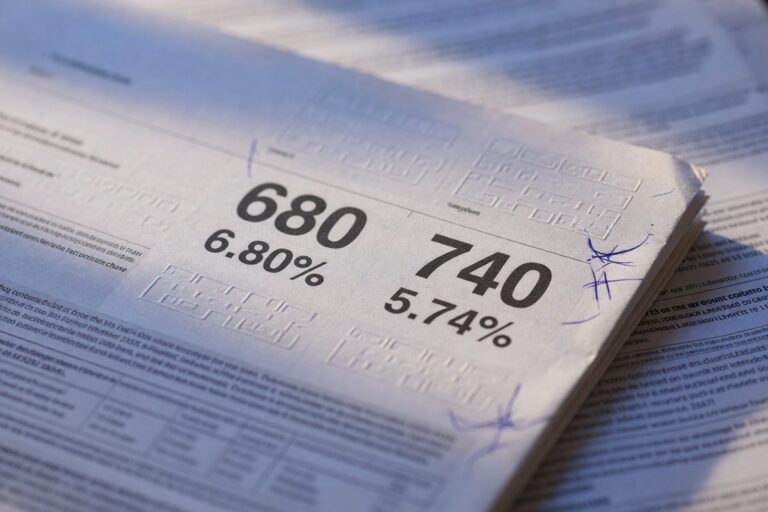

A 60-point credit score jump from 680 to 740 cuts your mortgage rate by 0.25–0.35%, saving $50–$65 monthly and over $20,000 across the loan term.

Secure today's rate 60–90 days before making an offer with Lock & Shop programs. First-time buyers protect against rate spikes and strengthen offers in competitive markets.

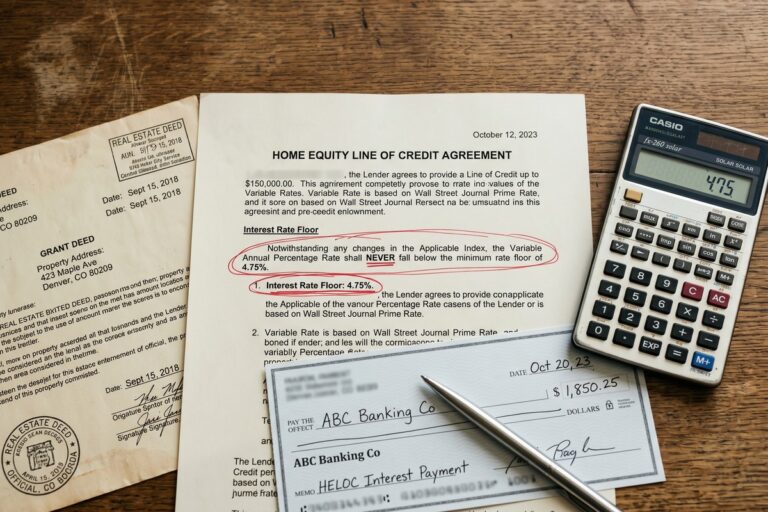

HELOC interest rate floors often cap out at 4–8% regardless of Fed cuts. See why borrowers who expected savings hit a ceiling, and how to protect yourself before signing.

Inheritance recipients are saving thousands by using lump-sum paydowns to drop 0.25%–0.75% in interest rates without refinancing. Here's how the strategy works.

Specialized healthcare worker mortgage rates save money only if the rate is within 0.25% of conventional loans and you qualify for at least $5,000 in grants. See when they don't pencil out.