How Single-Income Households Are Stretching Budgets and Managing Loan Payments in 2026

Learn about single income household budgeting. Discover proven strategies families use in 2026 to stretch every dollar and stay on top of loan payments.

Learn about single income household budgeting. Discover proven strategies families use in 2026 to stretch every dollar and stay on top of loan payments.

Learn about debt to income ratio lending. Discover why lenders scrutinize your DTI more than you expect and how it shapes your borrowing power.

Learn about personal loan career change options. Discover if borrowing to fund a career transition or unpaid internship is a smart financial move for you.

Gig income swings 40–60% month to month—so the standard 3-month rule doesn't cut it. Here's a percentage-based system to build 6–9 months of savings on irregular pay.

With $58,700 in average student debt and a median salary of $61,820, teachers have almost no breathing room — here's how side income is changing that equation.

Borrow $2,000–$5,000 at 10–15% APR to jumpstart your emergency fund instead of turning to payday loans or credit cards. See if this strategy fits your situation.

Learn about personal loan fixed income. Discover how retirees borrow smart, protect their budget, and choose loans that won't strain their monthly cash flow.

The 50/30/20 rule fails high earners. See why the top 20% need different frameworks to manage complexity, taxes, and lifestyle inflation—and build real wealth.

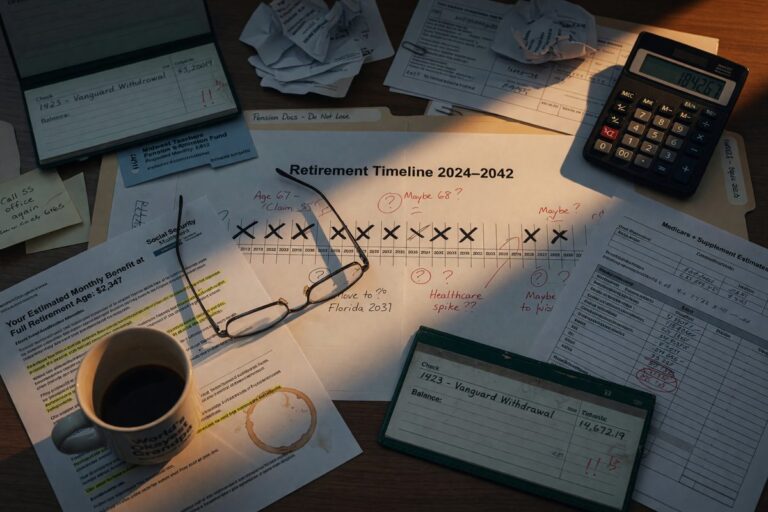

Skipping catch-up contributions and claiming Social Security too early can derail early retirement. See the 5 costly mistakes people over 50 make—and how to fix them.

A $1,200 balance triggered a $312 charge in one billing cycle. Here's how deferred interest clauses turn 0% APR offers into costly debt traps—and what to do instead.