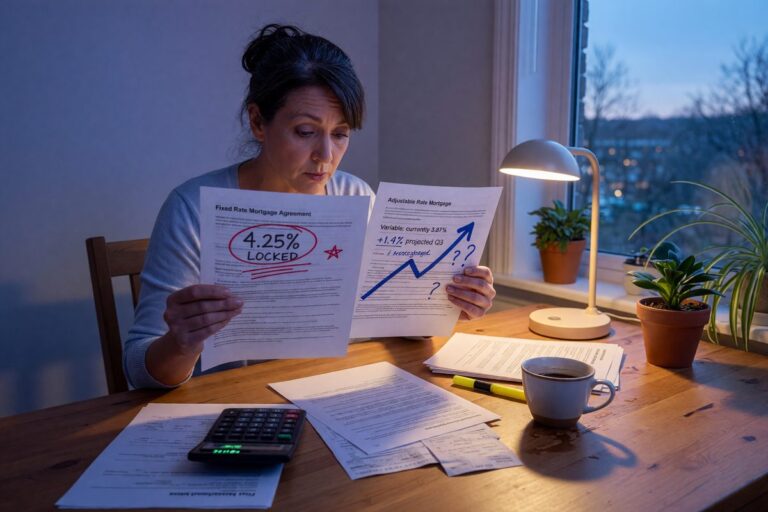

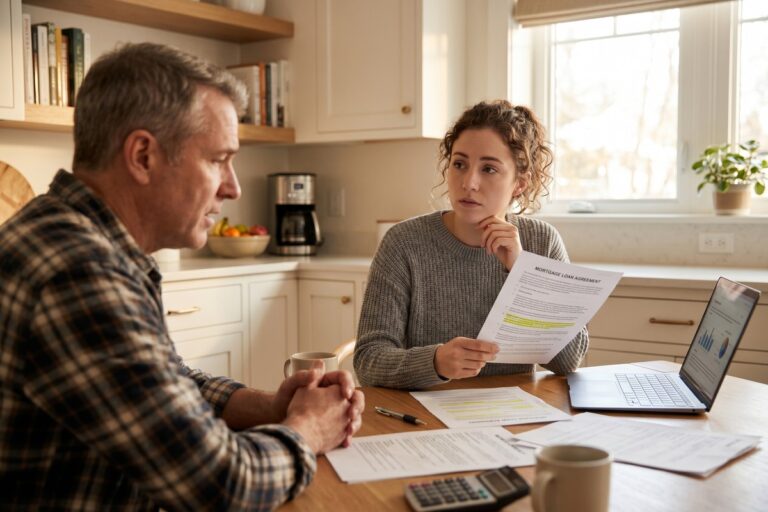

Fixed vs Variable Rate Personal Loans: When Locking In Actually Costs You More

Fixed rates win for most borrowers—but locking in can backfire on 3-year loans if rates fall. See when variable actually makes sense.

Fixed rates win for most borrowers—but locking in can backfire on 3-year loans if rates fall. See when variable actually makes sense.

Save $300+ annually on interest by setting aside $100/month for predictable expenses. See how the sinking fund budgeting strategy keeps you out of debt.

Self-employed borrowers with two years of tax returns and 3–6 months of bank statements qualify for the lowest personal loan APRs. See what lenders actually verify.

Personal loans fund in 1–7 days; cash-out refinances take 42+ days. Here's which option actually works for a financial emergency.

Households earning $75K–$100K could afford only 21% of listings in early 2025. Here's how to use the price-to-rent ratio to decide if buying actually makes sense.

At 12.27% APR, paying off your personal loan beats investing in most cases. Here's exactly where the math flips and when building a portfolio wins instead.

About 25% of married couples rely on one paycheck. Here's how they cap housing at 28% of gross income and use zero-based budgeting to cover childcare and debt.

45 million Americans have no usable credit score—but renters are crossing 700 in 12–24 months using rent-reporting, credit-builder loans, and authorized user status.

With average households carrying $7,200 in credit card debt, the budgeting system you choose matters more than your intentions. Here's which method actually moves the needle.

A co-signer with a score below 670 or a DTI over 43% can trigger higher rates or outright denial. Here's what to do instead without the shared liability.