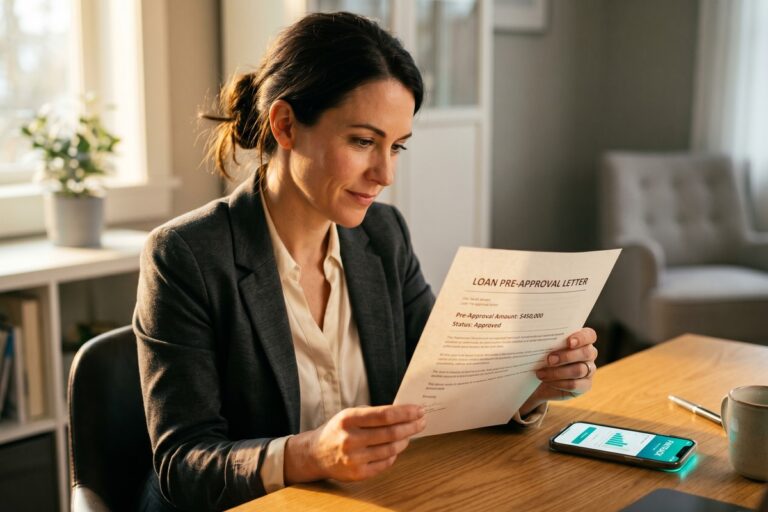

Fintech Lender vs Credit Union After a Job Loss: Which Should You Choose?

Learn about fintech vs credit union lending. Compare rates, flexibility, and approval odds to find the best borrowing option after losing your job.

Learn about fintech vs credit union lending. Compare rates, flexibility, and approval odds to find the best borrowing option after losing your job.

The CFPB now treats pay-in-four BNPL products as credit cards, and the UK's FCA expects full oversight by 2026—here's what that means for Affirm, Klarna, and Afterpay.

43% of self-employed adults are denied business credit — fintech platforms like Pipe and BlueVine let freelance designers convert invoices into same-day capital instead.

Fintech lenders approve caregivers with irregular income using alternative data and bank patterns. Platforms like Upstart and Dave offer personal loans with APRs far below payday loans.

Get 0.25% rate cuts or lower fees by collecting 3 competing fintech offers in 14 days, then presenting them to your lender. Most borrowers finish in under a week.

Fintech lenders analyze 7 data signals beyond your credit score—cash flow, device behavior, rent history—and can decide in 3 minutes. Here's what to know before you apply.

Fintech lenders using AI underwriting approve 27% more thin-file applicants by reading 1,000+ data signals FICO never considers — here's exactly what they see differently.

The embedded finance market hit $138B in 2025 and is headed to $588B by 2030 — here's how faster credit access, contextual loans, and new privacy risks affect you.

Approval in as little as 24 hours and up to $100,000 — fintech platforms are giving the 18.6 million U.S. veteran homeowners faster options the VA loan system doesn't always cover.

Retirees with variable income see 38% higher approval rates on fintech platforms versus traditional banks, with closings in 11 days instead of 38.