Fixed vs Adjustable Rate Loans for Self-Employed Borrowers: Key Differences Explained

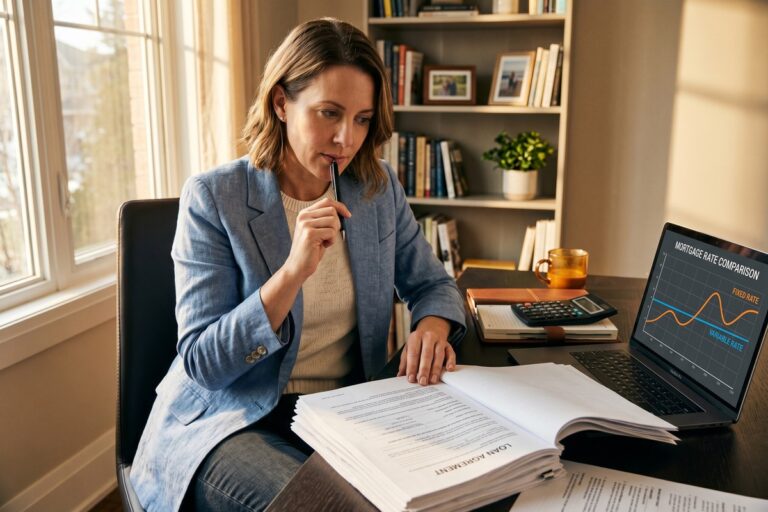

Fixed rates run 0.5–1.5% above initial ARM rates right now — a real cost difference when self-employed income docs can already shift your rate by 1.5 points.

Fixed rates run 0.5–1.5% above initial ARM rates right now — a real cost difference when self-employed income docs can already shift your rate by 1.5 points.

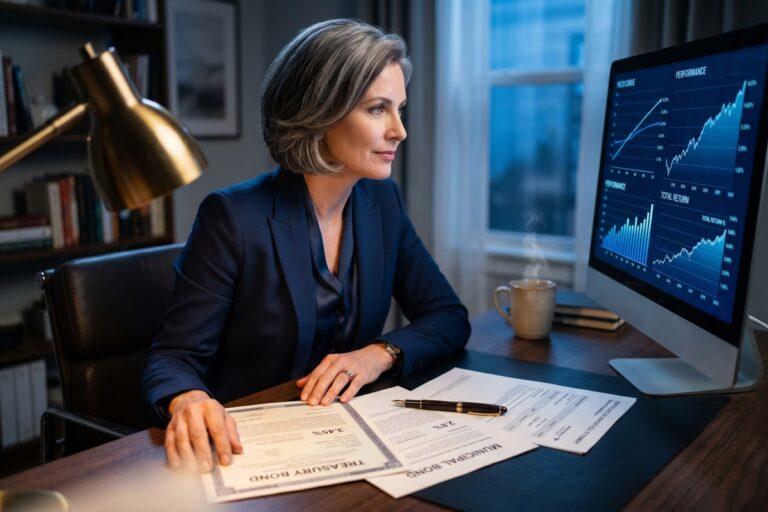

T-bills often yield 0.10%–0.40% more than bank CDs when the Fed pauses, but top online CDs can flip that gap. Here's how to compare both before locking in.

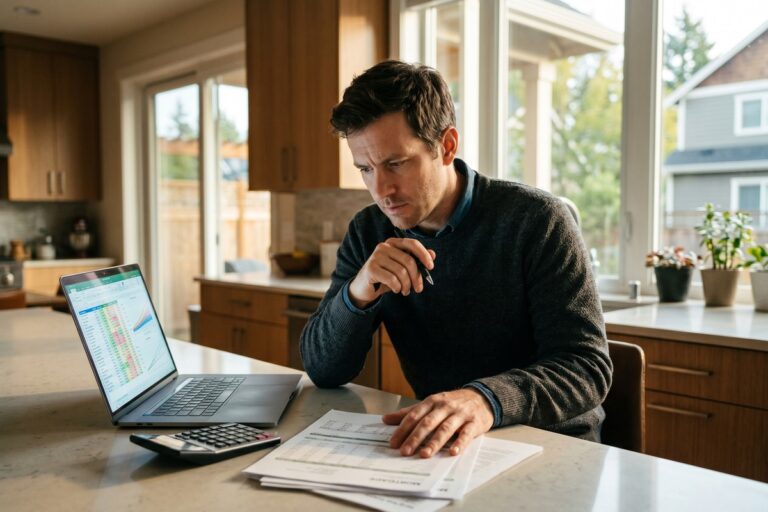

A $600 monthly payment spike is hitting ARM borrowers right now as 2019–2021 loans reset past 7%. Here's what to do before your adjustment date arrives.

Learn about self employed loan interest rate penalties. Discover proven strategies to fight back against hidden rate markups and secure fairer loan terms.

36% of self-employed workers struggle with monthly debt payments. Here's how to use income smoothing and debt avalanche strategy to pay down high-interest loans on a variable income.

A $5,000 credit card balance at 20% APR compounded daily can exceed $6,100 in a year—without a single new purchase. Here's exactly how that happens.

A single comparison error on a personal loan APR between 6.99%–35.99% can cost thousands. Here are the 5 mistakes borrowers make and how to avoid them.

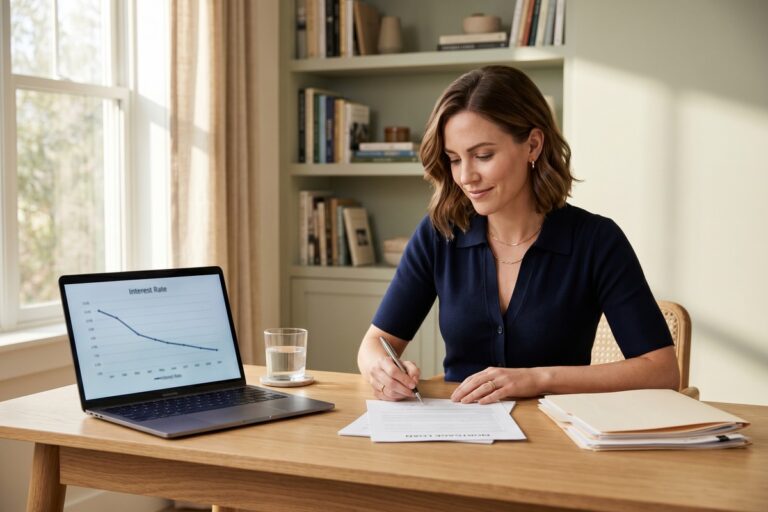

Mortgage rates are stuck in the mid-to-upper 6% range—act within your 30–60 day lock window now or risk paying hundreds more per month if the Fed moves rates higher.

Top 1-year CDs are hitting 5.00% APY while the best high-yield savings accounts pay 4.75%—the right choice depends entirely on when you need the cash.

Fixed rates range from 8–36%, while variable rates start lower but risk rising. See which loan type matches your financial priorities.