How a Debt-to-Income Ratio Above 40% Affects the Interest Rate You Qualify For

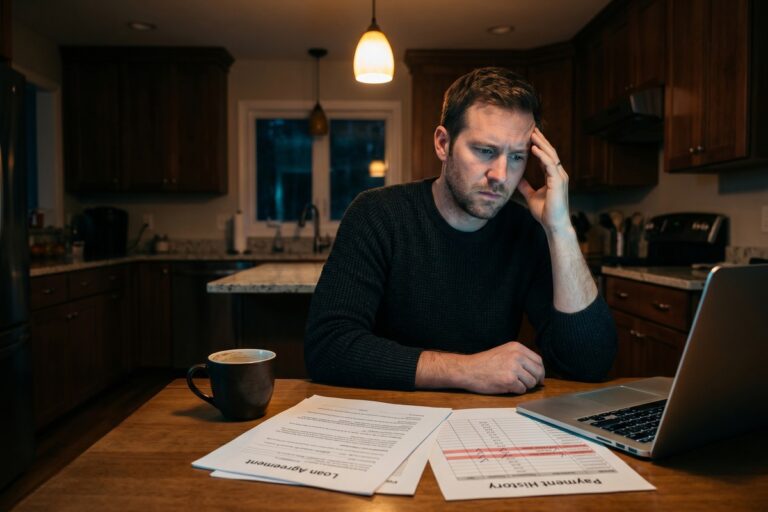

A DTI above 40% can raise your mortgage or personal loan rate by 1–3 percentage points and push you into subprime terms. Here's exactly how lenders price that risk.

A DTI above 40% can raise your mortgage or personal loan rate by 1–3 percentage points and push you into subprime terms. Here's exactly how lenders price that risk.

The 10-year Treasury sits near 4.3% and mortgage rates are stuck above 6.5%. Here's what the yield curve's slow re-steepening means for your borrowing costs.

One late payment can drop your credit score by up to 110 points and push your personal loan APR past 25%. Here's exactly how lenders price that risk against you.

CD yields drop within weeks of a Fed rate cut. Here's how retirees can protect income with dividend stocks, TIPS, bond ladders, and a 3.5–4% withdrawal rate.

With the Prime Rate at 7.50% and the Fed on hold, a variable rate loan can save money — but only if your cash flow can handle a 2–4 point swing in under 36 months.

Auto loans average 7.1% vs 12.4% for personal loans—a gap that compounds fast over 48–72 months. See when each option actually makes sense for your purchase.

The 10-year Treasury–mortgage spread is still 2.5–2.7 points wide in 2026. When it normalizes, borrowers could save $150–$300 a month—here's how to track it.

Over 73% of med school graduates carry $200K+ in debt—yet specialty mortgage programs let physicians bypass the risk tiers that penalize that debt load.

The 2004–2006 ARM boom wiped out $7 trillion in household wealth partly because of weak cap structures. Here's what to check before accepting any adjustable-rate mortgage.

45 million Americans have unscorable credit files—and most make 5 mistakes that add thousands in rate premiums. Here's what lenders actually look at.