Fact-checked by the CapitalLendingNews editorial team

The Verdict

A personal loan is almost always the right call when you need cash within two weeks or less. A cash-out refinance makes sense only if you need more than $50,000, already have strong equity and credit, and can wait 30 to 60 days without the situation worsening. For a true financial emergency, the refi timeline alone disqualifies it for most borrowers.

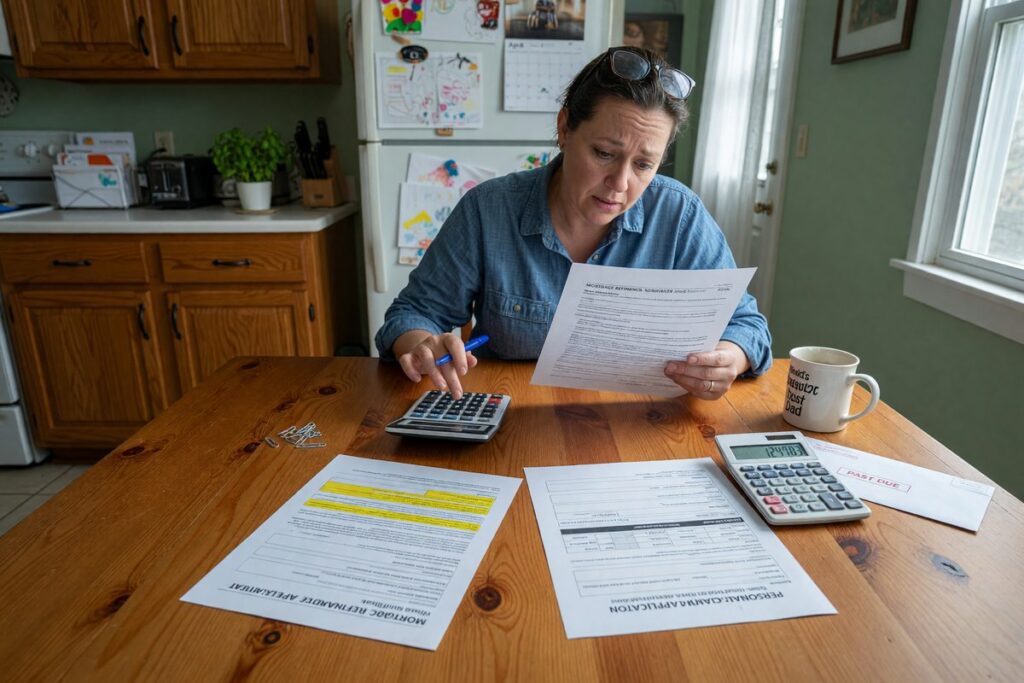

The choice between a personal loan cash-out refinance often comes down to a single variable: how fast you actually need the money. Personal loans routinely fund in one to seven days, while a cash-out refinance averages 42 days from application to closing, and that clock does not start until you have already gathered two years of tax returns, recent pay stubs, bank statements, and an appraisal order. In a genuine emergency, that paperwork sprint alone can burn a week before the 42 days even begins.

Mortgage rates remain elevated enough that many homeowners taking cash out are trading a low existing rate for a significantly higher one, making the long-term math of a refi even harder to justify for short-term cash needs. The question is not just which option is cheaper. It is which one you can realistically complete before the emergency gets worse.

| Factor | Reasons to Choose Personal Loan | Reasons to Choose Cash-Out Refinance |

|---|---|---|

| Speed to funding | 1–7 days; same-day possible with top online lenders | 30–60 days minimum; often longer in busy markets |

| Upfront costs | Origination fee typically 1–10% of loan amount | Closing costs 2–5% of the full new mortgage balance |

| Collateral risk | Unsecured, home is not on the line if you miss payments | Home is direct collateral; missed payments risk foreclosure |

| Loan size flexibility | Strong for amounts up to $50,000 | Better suited for $75,000+ when equity supports it |

| Qualification requirements | Credit and income review; no appraisal, no title work | Full mortgage underwriting, appraisal, title search required |

| Equity requirement | None; no home ownership needed | Must retain at least 20% equity post-close |

| Rate environment sensitivity | Rate is fixed to your credit profile, not broader mortgage market | Replaces existing rate with today’s rate, costly if current rate is lower |

| Emergency income disruption | Most lenders require only current income documentation | Recent job change or gap can trigger full denial mid-process |

Key Takeaways

- You need cash in hand within 14 days or fewer, cash-out refinance cannot clear underwriting that fast.

- The loan amount you need is under $50,000, personal loan origination fees in absolute dollars will typically be lower than refi closing costs on a new, larger mortgage balance.

- Your credit score is 670 or above, borrowers with FICO scores of 800+ have an 82% approval rate for personal loans, and rates improve sharply above 720.

- Your existing mortgage rate is below the current refinance rate, swapping a 3.5% mortgage for a 7%+ cash-out refi to cover a $25,000 repair bill is almost never sound math.

- You have experienced a recent income disruption (job change, reduction, medical leave), this can trigger refi denial mid-process, well after the appraisal fee is paid.

- You do not have at least 25–30% equity in your home, most lenders require you to retain 20% post-close, making small cash-out amounts structurally unavailable to recent buyers.

- You want to keep your home off the table as collateral while resolving the crisis.

How Quickly Can You Actually Get Cash in Hand?

Personal loans win on speed, and it is not close. Leading online lenders including SoFi, LightStream, and Marcus by Goldman Sachs advertise next-day or same-day funding after approval, with full applications taking under 15 minutes. Even at the slower end, most borrowers see funds in three to five business days. A cash-out refinance, by contrast, averages 42 days from application to closing based on ICE Mortgage Technology data through August 2025.

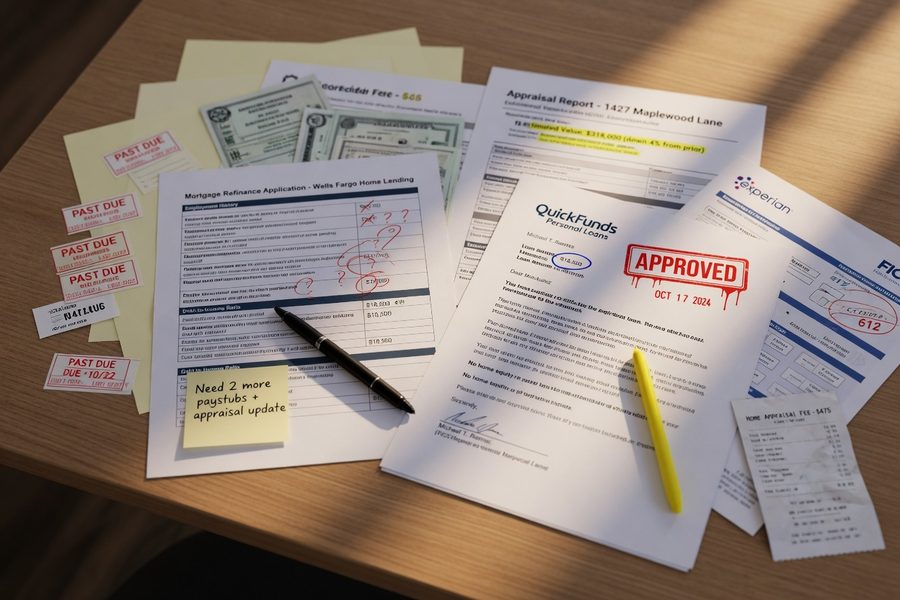

That 42-day average understates the real calendar time for many emergency borrowers. Before the application is even submitted, you need to locate two years of federal tax returns, compile 60 days of bank statements, pull together pay stubs, and coordinate an appraisal with a licensed appraiser who may have a one- to two-week backlog. Add five to seven business days for the mandatory right of rescission period on a primary residence refinance, and the practical timeline stretches to six to eight weeks from the moment you decide to act.

This is the gap most comparisons ignore. The 42-day clock starts when the lender receives a complete file. The clock to solve your emergency started the moment the bill arrived. For context on what consumers are doing in practice: total unsecured personal loan balances reached $207.1 billion in 2025 according to Experian, a figure that reflects just how often borrowers are choosing speed and flexibility over mortgage-tied products.

Upfront Costs and Hidden Delays That Actually Matter

For loans under $50,000, personal loan origination fees are almost always cheaper in absolute dollar terms than cash-out refi closing costs. A personal loan with a 5% origination fee on a $30,000 balance costs $1,500 upfront. A cash-out refinance on a $350,000 home, structured to pull out that same $30,000, carries closing costs of 2–5% on the full new loan balance, potentially $7,000 to $17,500. You are not paying closing costs on the cash-out portion alone; you are paying them on the entire refinanced mortgage.

The cash-out refi also introduces cost layers that have nothing to do with your rate: the appraisal itself (typically $400–$700), title insurance, lender fees, and potentially points. These are paid before you receive a single dollar of proceeds. If the appraisal comes in low, a real risk in softening local markets, the lender may reduce the approved cash amount or deny the loan entirely, after you have already spent the money and the time.

Personal loans carry their own caveat worth naming: interest rates are considerably higher than mortgage rates, and for large amounts held long-term, the total interest paid will exceed what a cash-out refi would cost. The crossover point is roughly $50,000 or higher, held for five or more years. Below that threshold or within a shorter payoff window, the personal loan’s lower absolute closing cost and faster access usually win on net cost. If you are weighing a longer-term borrowing strategy, understanding how loan term length controls total interest paid is worth doing before you commit to either product.

Personal Loan vs Cash-Out Refinance: Which Is Harder to Qualify For During a Crisis?

Cash-out refinancing is significantly harder to qualify for, and an emergency itself can be the disqualifying factor. Full mortgage underwriting examines debt-to-income ratio, employment stability (typically requiring two years in the same field), and home equity levels. A medical emergency that triggers unpaid leave, or a job change made under financial pressure, can kill a refi application that was proceeding normally. Lenders often re-verify employment within 24 hours of closing; a status change at that moment causes an immediate denial.

The Consumer Financial Protection Bureau has noted that cash-out mortgage refinance borrowers tend to improve their credit scores after completing the process, but that framing assumes the borrower successfully closes. Many emergency borrowers do not reach closing, having been denied mid-process or forced to abandon the application when their financial situation shifted.

Personal loans have their own qualification bar, but it is lower and faster to clear. Borrowers with FICO scores above 800 are approved 82% of the time. Even in the 660–720 range, approval rates at online lenders are meaningful, and many fintech lenders now incorporate payroll data and bank transaction history to approve borrowers that traditional underwriting would reject. For a deeper look at how lenders are reading signals beyond your credit file, alternative data points digital lenders weigh in 2026 are worth understanding before you apply.

One scenario that completely blocks a cash-out refi: recent home purchase. If you bought your home within the past year, you likely lack the equity cushion needed. Most conventional lenders require you to retain at least 20% equity after the cash-out, meaning you need 25–30% equity to pull any meaningful amount. Borrowers who put down less than 20% at purchase are structurally unable to use a cash-out refi regardless of their credit score. For them, the personal loan is not just faster, it is the only path.

Who Should and Who Should Not

Good candidates for a personal loan in an emergency

Most people facing a genuine time-sensitive financial crisis fall into this group.

- Homeowners with recent purchase dates or limited equity who cannot meet the 20% post-close equity threshold for a cash-out refi.

- Borrowers needing $5,000 to $50,000 within one to two weeks for medical bills, urgent home repairs, or short-term income replacement.

- Anyone with a credit score above 680 who qualifies for competitive personal loan APRs and wants to keep their home off the table as collateral.

- Borrowers who experienced a recent job change, income reduction, or medical leave, circumstances that often trigger refi denial but may still clear personal loan underwriting.

- Renters, or homeowners who simply prefer not to restart a 30-year mortgage clock to access short-term cash.

Who should skip the personal loan and consider a cash-out refinance

There are situations where the slower process is worth tolerating.

- Homeowners with 40%+ equity and stable employment needing $75,000 or more, who can genuinely wait six to eight weeks for funds.

- Borrowers whose current mortgage rate is already at or above today’s refinance rate, so replacing it does not meaningfully increase their monthly payment.

- Those with excellent credit (FICO 760+) and strong documented income who will clear full mortgage underwriting without friction.

- Situations where the cash need is large enough that personal loan interest rates would cost substantially more in total interest over a five-plus year horizon.

The CFPB’s refinancing guidance makes the underlying principle clear: refinancing is worth pursuing only when it serves a specific financial goal and the borrower can sustain the new payment structure. In an emergency, both conditions are harder to meet than they appear.

Frequently Asked Questions

How long does it take to get money from a cash-out refinance versus a personal loan?

A personal loan typically funds in one to seven business days; same-day funding is available from several online lenders. A cash-out refinance averages 42 days from application to closing, and that excludes the one to two weeks of document gathering before a complete file is submitted. In a genuine emergency, that gap is usually decisive.

Is a personal loan or cash-out refi better if I have good credit?

Good credit improves your options on both products, but it does not change the timeline problem. Even with excellent credit, a cash-out refi still requires an appraisal, full underwriting, and title work. If speed matters, the personal loan is still the answer. If you have a FICO above 720 and can wait two months, a cash-out refi may offer a lower rate on large amounts.

What if I only have 10% equity in my home, can I do a cash-out refinance?

No. Most conventional lenders require you to retain at least 20% equity after the cash-out, meaning you need at least 25–30% equity before taking anything out. With 10% equity, a cash-out refi is not available regardless of your credit score or income. A personal loan or fintech credit alternatives designed for specific cash needs are the practical options in that scenario.

Does a cash-out refinance hurt your credit more than a personal loan?

Both involve a hard credit inquiry and both affect your credit utilization and average account age. The CFPB has found that cash-out refinance borrowers often improve their credit scores post-close, likely because the proceeds are used to pay down other debts. A personal loan that consolidates high-interest balances can have a similar positive effect. Neither product is dramatically worse for credit than the other when managed responsibly.

Can I use a personal loan to cover a medical emergency if I have a mortgage?

Yes, and for most medical emergencies, a personal loan is the better fit on every dimension that matters. The CFPB confirms personal installment loans can be used for unexpected expenses including medical bills, with fixed repayment schedules that make budgeting predictable. A cash-out refi in a medical emergency is a poor choice, underwriters often scrutinize income stability more closely when the emergency itself may have caused a work disruption, creating a real risk of mid-process denial. For borrowers navigating an income gap, fintech-based emergency fund strategies can also reduce reliance on high-cost borrowing during a crisis.

Sources

- Consumer Financial Protection Bureau, What Is a Personal Installment Loan?

- Consumer Financial Protection Bureau, Should I Refinance? (Handout)

- Federal Reserve, A Consumer’s Guide to Mortgage Refinancings

- Consumer Financial Protection Bureau, CFPB Report Finds Cash-Out Mortgage Refinance Borrowers Improve Credit Scores

- AmeriSave, How Long Does It Take to Refinance a House: Timeline Breakdown (ICE Mortgage Technology data)

- Experian, Personal Loan Usage Statistics (2025)

- Credible, Personal Loan Statistics (2026)