Fact-checked by the CapitalLendingNews editorial team

Quick Answer

Personal loans for single parents can bridge childcare gaps between jobs in as little as 1–2 business days after approval. In July 2025, single parents can borrow $1,000–$50,000 through online lenders, credit unions, or fintech platforms by gathering income documents, comparing APRs, pre-qualifying without a hard credit pull, and selecting a repayment term that fits a reduced income period.

Personal loans for single parents have become one of the most practical tools for covering childcare costs during job transitions — and for good reason. According to Child Care Aware of America’s 2024 report, the average annual cost of full-time center-based childcare now exceeds $15,000 in most U.S. states, a figure that does not pause when a parent loses or leaves a job. In July 2025, more single parents are turning to personal loans to maintain consistent childcare arrangements while they search for new employment, complete training programs, or wait for benefits to activate.

The urgency is real. Single-parent households represent roughly 27% of all U.S. families with children, according to U.S. Census Bureau data, and they are disproportionately affected by income disruptions. Pulling a child from daycare during a job search can make the search itself nearly impossible — creating a cycle that a short-term personal loan can break.

This guide is written specifically for single parents who need to cover childcare expenses during a gap between jobs. By the end, you will know exactly which loan types to consider, how to qualify with limited or transitional income, what lenders actually look for, and how to protect yourself from high-cost traps.

Key Takeaways

- The average cost of full-time center-based childcare exceeds $15,000 per year nationally, according to Child Care Aware of America, making short-term loan coverage a realistic bridge strategy.

- Personal loan APRs for borrowers with good credit (670+) typically range from 8% to 15%, while subprime borrowers may see rates from 20% to 36%, per Federal Reserve consumer credit data.

- Many online lenders and fintech platforms fund personal loans within 1–2 business days, making them faster than most government assistance programs, which can take 2–6 weeks to process.

- Single parents can often qualify using unemployment benefits, child support, or freelance income as documented income — not just traditional W-2 employment income.

- Pre-qualifying for a personal loan through a soft credit inquiry does not affect your credit score, allowing you to compare offers from multiple lenders safely before committing.

- Credit unions frequently offer personal loan rates 3–5 percentage points lower than traditional banks, with the National Credit Union Administration capping member loan rates at 18% APR.

In This Guide

- Step 1: How do I figure out exactly how much I need to borrow for childcare between jobs?

- Step 2: Can I qualify for a personal loan as a single parent with no current job?

- Step 3: Which lenders are best for personal loans for single parents in 2025?

- Step 4: How do I apply for a personal loan to cover childcare without hurting my credit?

- Step 5: How do I manage personal loan repayments while I am still between jobs?

- Step 6: Are there alternatives to personal loans for single parents covering childcare gaps?

- Frequently Asked Questions

Step 1: How Do I Figure Out Exactly How Much I Need to Borrow for Childcare Between Jobs?

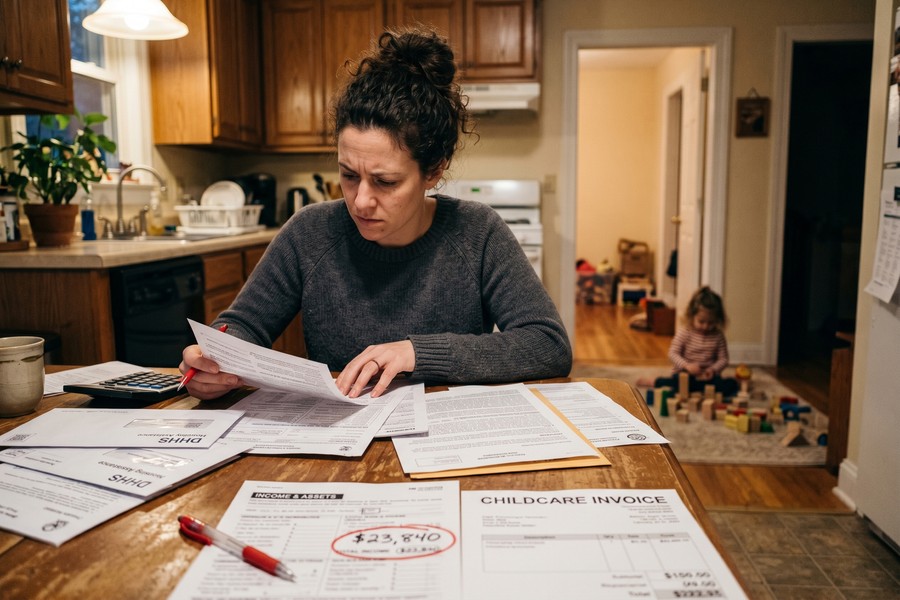

Start by calculating the precise monthly cost of your current childcare arrangement, then multiply it by the estimated number of months your job gap will last. Borrowing the exact amount you need — not a rough estimate — keeps interest costs low and prevents you from taking on unnecessary debt.

How to Do This

Gather your most recent childcare invoices or contracts and note the monthly total. Factor in any registration fees, late pickup charges, or supply fees that recur monthly. According to Child Care Aware of America’s state-by-state data, infant care averages $1,230 per month nationally, though this ranges from roughly $700 in Mississippi to over $2,400 in Massachusetts.

Next, estimate your job search timeline honestly. The Bureau of Labor Statistics reports that the average duration of unemployment in 2024 was approximately 21 weeks, though workers in competitive industries often find positions faster. A conservative borrowing plan assumes three to four months of childcare coverage.

Add a 15% buffer to your base calculation to account for unexpected costs — a sick day policy fee, a schedule change, or a brief delay in your start date. For example, if your monthly childcare bill is $1,200 and you estimate a three-month gap, your target loan amount would be approximately $4,140 after the buffer.

What to Watch Out For

Do not borrow the maximum amount a lender offers. Lenders pre-approve based on your creditworthiness, not your actual need, and accepting more than you need means paying interest on money you will not use. Also avoid confusing gross childcare costs with any subsidies already in place — only borrow to cover the out-of-pocket gap.

The average American family with one child in full-time daycare spends $10,000–$18,000 per year on childcare, representing up to 19% of median family income, according to Child Care Aware of America. For single-income households, that share is dramatically higher.

Step 2: Can I Qualify for a Personal Loan as a Single Parent With No Current Job?

Yes — many lenders accept non-employment income sources, and being between jobs does not automatically disqualify you. What lenders actually need is documented proof that you can repay the loan, not necessarily proof of a current employer.

How to Do This

Identify every income source you currently have access to. Lenders commonly accept the following as qualifying income for personal loans:

- Unemployment insurance benefits — document with your state benefits award letter

- Child support or alimony — document with a court order and three to six months of payment history

- Freelance or gig income — document with bank statements, 1099 forms, or a profit-and-loss statement

- Social Security or disability income — document with your benefits verification letter

- Investment or rental income — document with tax returns or lease agreements

Fintech lenders, in particular, have moved toward bank transaction-based underwriting, which means they review 60–90 days of account activity rather than relying solely on pay stubs. This shift benefits single parents with variable or transitional income significantly. You can learn more about how this works in our guide on how fintech lenders use bank transaction data to approve loans.

What to Watch Out For

Some lenders require that income be “stable and ongoing” — which may exclude one-time child support payments or sporadic freelance income. Always read the lender’s income eligibility requirements before applying. A rejection leaves a hard inquiry on your credit report that can lower your score by 5–10 points temporarily.

If your income is primarily from child support or freelance work, use a lender that explicitly accepts alternative income documentation — such as LendingClub, Upstart, or your local credit union. Call them directly before applying to confirm your income type qualifies.

Step 3: Which Lenders Are Best for Personal Loans for Single Parents in 2025?

The best lenders for personal loans for single parents in 2025 are those that accept alternative income documentation, offer low minimum APRs, and fund quickly. Your three primary categories are online fintech lenders, credit unions, and community development financial institutions (CDFIs).

How to Do This

Compare lenders across four key variables: minimum credit score requirement, income documentation flexibility, funding speed, and APR range. The table below provides a direct comparison of the most relevant lender categories for single parents navigating a job transition.

| Lender Type | Min. Credit Score | APR Range | Funding Speed | Alternative Income Accepted |

|---|---|---|---|---|

| Credit Union | 580–620 | 7%–18% | 1–3 business days | Yes (child support, benefits) |

| Online Fintech Lender | 580–660 | 8%–36% | Same day–2 days | Yes (bank statements, 1099) |

| Traditional Bank | 660–700 | 10%–25% | 3–7 business days | Limited (W-2 preferred) |

| CDFI / Nonprofit Lender | No minimum | 6%–20% | 3–10 business days | Yes (all income types) |

| Peer-to-Peer Platform | 600–640 | 8%–36% | 2–5 business days | Yes (freelance, benefits) |

Notable lenders to research include Upstart, which uses an AI underwriting model that weighs education and employment history alongside credit scores; LendingClub, which accepts a range of income types for its personal loan products; and Oportun, a CDFI-certified lender that specifically serves borrowers with limited credit history. For a deeper comparison of fintech lending platforms, see our breakdown of fintech loan apps vs. peer-to-peer lending platforms in 2026.

“Single parents often underestimate how many lenders will work with non-traditional income. The key is matching your income documentation to the lender’s underwriting model before you apply — not after. One well-targeted application beats five speculative ones every time.”

What to Watch Out For

Predatory lenders — including payday loan companies and some installment lenders — target single parents with urgent financial needs. Any lender advertising APRs above 36% should be avoided. The Consumer Financial Protection Bureau (CFPB) considers 36% APR the threshold above which loans become financially harmful for most borrowers.

Some lenders advertise “no credit check” personal loans with extremely fast approvals. These typically carry APRs of 100% or more and are structured as payday or installment loans, not true personal loans. Always verify the lender’s license with your state’s banking regulator before submitting any personal information.

Step 4: How Do I Apply for a Personal Loan to Cover Childcare Without Hurting My Credit?

Apply by pre-qualifying first — this uses a soft credit pull that does not affect your score, allowing you to compare real rate offers before submitting a formal application. Once you identify the best offer, submit one formal application to avoid multiple hard inquiries.

How to Do This

Follow this sequence to protect your credit score throughout the application process:

- Check your credit report for errors at AnnualCreditReport.com — the only federally authorized free report site. Dispute inaccuracies before applying.

- Pre-qualify with 2–3 lenders simultaneously using their soft-pull tools. Most fintech platforms (Upstart, LendingClub, Prosper) offer this on their websites.

- Compare your pre-qualified offers by total cost, not just monthly payment. A lower monthly payment with a longer term often costs more overall.

- Gather your documents before submitting the formal application: government-issued ID, Social Security number, proof of income (benefit letters, bank statements, child support orders), and your childcare provider’s contact information or invoices.

- Submit one formal application to your chosen lender. This triggers a hard inquiry, but a single inquiry typically reduces your credit score by fewer than 5 points.

If your credit score is below 620, consider adding a co-signer with stronger credit — a family member or trusted friend. A co-signer can help you qualify for a significantly lower rate. Understanding how your income type affects approval odds is also worth reviewing; our guide on digital loan approval odds by income type breaks this down in detail.

What to Watch Out For

Do not apply to five or more lenders simultaneously hoping for one approval. Multiple hard inquiries within a short window signal financial distress to future lenders. If you are unsure which lender will approve you, use a loan marketplace like LendingTree or Credible — these submit your information to multiple lenders with a single soft inquiry before you commit.

Multiple hard credit inquiries for the same loan type within a 14–45 day window are often treated as a single inquiry by FICO scoring models, according to myFICO’s credit education resources. This means you can safely shop multiple lenders within that period with minimal score impact.

Step 5: How Do I Manage Personal Loan Repayments While I Am Still Between Jobs?

Managing personal loan repayments between jobs requires choosing the right loan term upfront and communicating proactively with your lender if your financial situation changes. Most lenders offer hardship accommodations — but only if you ask before missing a payment.

How to Do This

When selecting your loan, choose the longest term that keeps the total cost acceptable. A 36-month term on a $5,000 loan at 14% APR results in monthly payments of approximately $171 — manageable even on unemployment benefits. A 24-month term raises that payment to roughly $241.

Set up autopay immediately after loan disbursement. Most lenders offer a 0.25%–0.50% APR discount for enrolling in automatic payments, and autopay eliminates the risk of forgetting a payment during a stressful job search period.

If you anticipate difficulty making a payment, contact your lender’s hardship department at least 15 days before the due date. Many personal loan lenders — including LendingClub, Marcus by Goldman Sachs, and SoFi — offer deferment or forbearance options that allow you to skip one or two payments without penalty. For managing multiple debt obligations during this period, understanding the debt avalanche vs. debt snowball methods can help you prioritize once you return to work.

What to Watch Out For

Never skip a payment without first getting written confirmation of a deferment agreement from your lender. Unauthorized missed payments are reported to credit bureaus after 30 days and can drop your credit score by 60–110 points, making future borrowing significantly more expensive.

When you do return to work, make one extra payment toward your personal loan principal in your first full paycheck month. Even a single additional payment on a 36-month loan can reduce your total interest paid by hundreds of dollars and shorten your payoff timeline by one to two months.

Step 6: Are There Alternatives to Personal Loans for Single Parents Covering Childcare Gaps?

Personal loans are not the only option — and for some single parents, a combination of government assistance, nonprofit grants, and payment plans may cover childcare gaps at a lower cost. Evaluating alternatives before borrowing is a critical step in responsible financial planning.

How to Do This

Work through the following alternatives in order of cost, starting with free options:

- Child Care and Development Fund (CCDF): A federal subsidy program administered by states that helps low-income families pay for childcare. Apply through your state’s childcare agency. Approval can take 2–6 weeks, so apply immediately when a job gap begins.

- Child Care Scholarship programs: Many states offer emergency childcare scholarships with faster turnaround than CCDF. Search your state’s childcare resource and referral agency through Child Care Aware’s state resource map.

- Nonprofit emergency assistance: Organizations like the United Way, Catholic Charities, and local community action agencies offer direct childcare assistance or emergency cash grants to single parents.

- Provider payment plans: Many daycare centers and in-home providers will work out a deferred payment arrangement for existing clients. Ask your current provider before assuming you must leave.

- Family and friends network: Informal childcare arrangements with trusted family members during a job transition are cost-free and may preserve your daycare slot for when you return to work.

If government assistance is not fast enough and nonprofit grants do not fully cover your gap, personal loans for single parents fill the difference. They also preserve your childcare slot — something that can take months to reclaim in areas with long waiting lists. Single parents who also have irregular income after returning to work may find the guidance in our article on how a freelancer with irregular income should handle a high-interest loan directly applicable.

What to Watch Out For

Government assistance programs often have income cutoffs that disqualify parents earning above a certain threshold — even if that income is insufficient to cover full childcare costs. Do not assume you will not qualify. Apply and let the program determine eligibility.

“The worst thing a single parent can do during a job transition is pull their child from childcare to save money. It makes the job search exponentially harder. If a short-term personal loan keeps that childcare slot intact, it is a genuine investment in getting back to financial stability faster.”

Frequently Asked Questions

Can I get a personal loan as a single parent if I only have unemployment benefits as income?

Yes — unemployment benefits count as qualifying income at many lenders, including credit unions, CDFIs, and several fintech platforms. You will need to provide your unemployment award letter showing the weekly benefit amount and the duration of benefits remaining. Lenders will calculate your monthly equivalent income from this documentation. The key is choosing lenders that explicitly accept government benefits as income before applying.

What credit score do I need to qualify for a personal loan to cover childcare expenses?

Most mainstream personal loan lenders require a minimum credit score of 580–620, though borrowers with scores above 670 receive the most competitive rates. If your score is below 580, a CDFI lender or credit union with a financial counseling component may be your best path. You can check your score for free through Experian, Credit Karma, or your bank’s credit monitoring tool without impacting your score.

How quickly can I get money from a personal loan if I need to pay childcare this week?

Same-day or next-business-day funding is available from several fintech lenders if you apply and are approved early in the day. LightStream (a division of Truist Bank) and Rocket Loans both advertise same-day funding for qualified applicants. Credit unions and traditional banks typically take three to seven business days. Submit your application as early in the morning as possible, with all documents ready, to maximize the chance of same-day disbursement.

Will taking a personal loan hurt my chances of getting a job or renting an apartment?

Employers are not permitted to see your debt balances — only certain employer credit checks are allowed, and they show payment history, not the existence of specific loans. A personal loan with on-time payments will not negatively affect an employer background check. Landlords may see your debt-to-income ratio through a rental application credit pull, but a single personal loan with current payments is unlikely to disqualify you from renting.

Should I use a credit card or a personal loan to cover childcare between jobs?

A personal loan is almost always cheaper than a credit card for covering several months of childcare. The average credit card APR in 2025 is approximately 21.5%, according to the Federal Reserve’s consumer credit report, while personal loan rates for good-credit borrowers start around 8%–12%. Personal loans also have fixed monthly payments, which makes budgeting during a job search significantly easier. For more on this comparison, see our analysis of which financing option is actually cheaper for large purchases.

What if I get a new job quickly and want to pay off my personal loan early?

Most personal lenders allow early repayment without penalty, though you should confirm this before signing your loan agreement. Look for the term “no prepayment penalty” in the loan terms. Paying off a personal loan early saves you the remaining interest and frees up your monthly cash flow. If your lender charges a prepayment fee, calculate whether the fee is less than the remaining interest before deciding to pay early.

Are there personal loans specifically designed for single parents?

There are no federally designated “single parent personal loans,” but several CDFIs and nonprofit lenders target single-parent households with below-market rates and flexible underwriting. Accion Opportunity Fund and regional community loan funds often serve this demographic. Additionally, some states — including California and New York — offer low-interest emergency loan programs through their social services agencies. Contact your local 211 helpline to identify programs available in your area.

How do I avoid getting scammed when applying for personal loans as a single parent?

Verify that any lender you use is licensed in your state by checking your state banking department’s website. Legitimate lenders never ask for upfront fees before disbursing a loan — this is the most common scam targeting borrowers in financial distress. The CFPB’s complaint database allows you to look up lender complaints before applying. Always confirm the lender’s physical address, phone number, and state license number.

Can personal loans for single parents affect my eligibility for government childcare assistance?

A personal loan is a liability, not income, so it does not count as income for CCDF or other childcare subsidy eligibility determinations. Loan proceeds deposited into your bank account could temporarily appear as a large balance, but caseworkers typically look at income history, not account balances, for eligibility. Disclose the loan if asked directly, and clarify with your caseworker that it is a repayable debt, not income.

Sources

- Child Care Aware of America — The U.S. and the High Cost of Child Care

- U.S. Census Bureau — Single-Parent Families

- Federal Reserve — Consumer Credit Statistical Release (G.19)

- Bureau of Labor Statistics — Unemployed Persons by Duration of Unemployment

- Consumer Financial Protection Bureau — What Is a Payday Loan?

- National Credit Union Administration — The Credit Union Difference

- AnnualCreditReport.com — Official Free Credit Report Site

- myFICO — Applying for New Credit and Credit Inquiries

- Child Care Aware of America — State Resource and Referral Map

- Consumer Financial Protection Bureau — Consumer Complaint Database