How Fintech Lenders Are Using Payroll Data to Approve Borrowers Banks Would Reject

Fintech lenders reject 60% fewer borrowers than banks by using payroll data instead of credit scores. See who benefits—and who still can't qualify.

Fintech lenders reject 60% fewer borrowers than banks by using payroll data instead of credit scores. See who benefits—and who still can't qualify.

Refinancing cuts your rate only if it drops 1-2%+ and you have 3+ years left. Origination fees up to 8% often erase monthly savings—here's how to do the math.

Lenders keep your financial data for at least 7 years after closing—and often sell it. Here's when to request deletion and how to protect yourself from marketing abuse.

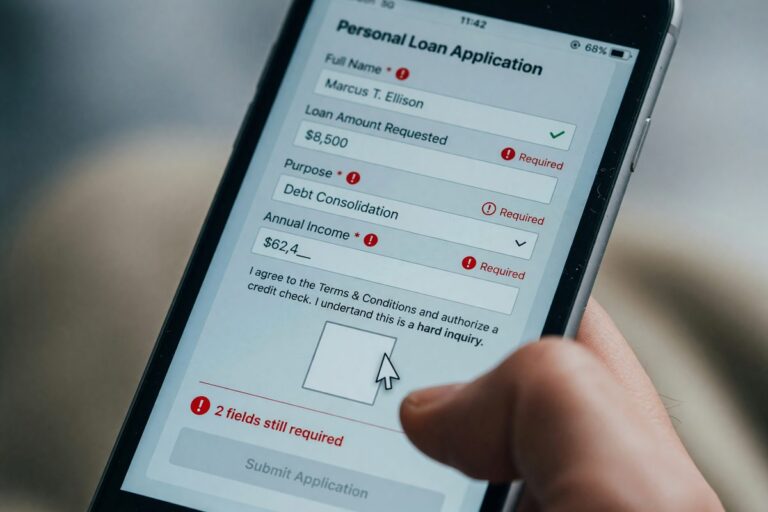

First-time borrowers with thin credit files lose more from pre-application errors than seasoned borrowers do. Here's what happens in those ten minutes before you click submit.

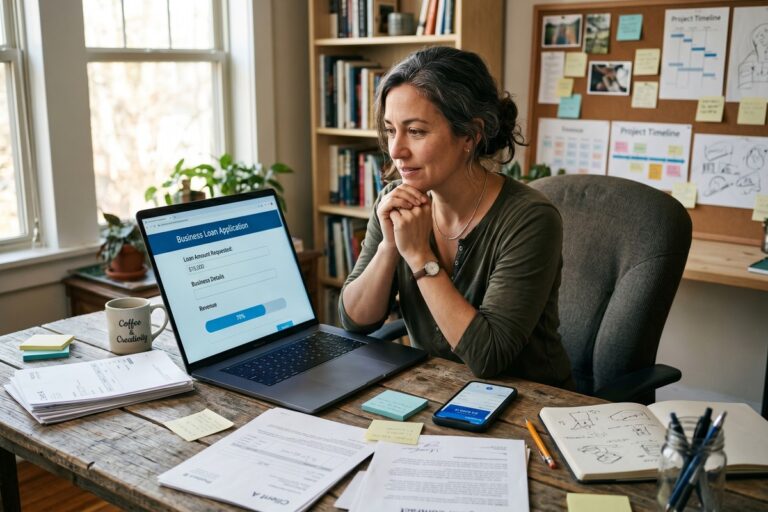

Gig workers average a 45% loan approval rate vs. 67% for W-2 earners—but it's a documentation gap, not a credit gap. Here's how to close it.

A 620 credit score and applying within 60 days of peak earnings can make or break your approval. Here's how timing—not creditworthiness—determines your odds.

A 1-point rate gap makes fintech refinancing worth it—but only if you carry no federal loans. Here's the one factor that determines whether you should do it.

Unplanned equipment downtime costs small businesses $8,000/hr. Fintech lenders now offer $5K–$500K in unsecured capital within 24–48 hours—no collateral required.

Fewer than 30% of approved borrowers actually receive same-day funds. See which platforms like LightStream, Upstart, and SoFi hold up under scrutiny.

A $7.2 trillion market by 2030—embedded lending is reshaping how people borrow, skipping banks entirely through apps like Shopify and Uber.