How a Newly Sober Borrower Rebuilt Finances Using a Credit-Builder Digital Loan

Newly sober borrowers who complete a credit-builder digital loan see average 48-point score gains in a year—but only if you can commit to reliable monthly payments.

Newly sober borrowers who complete a credit-builder digital loan see average 48-point score gains in a year—but only if you can commit to reliable monthly payments.

Most digital lender soft pull offers range $25,000–$50,000, but lenders build in a 20–30% safety buffer. See how to maximize your prequalified amount.

Fintech small business loans carry APRs of 14–99% versus 6.8–11% at banks. See when speed justifies the premium and when traditional lending wins.

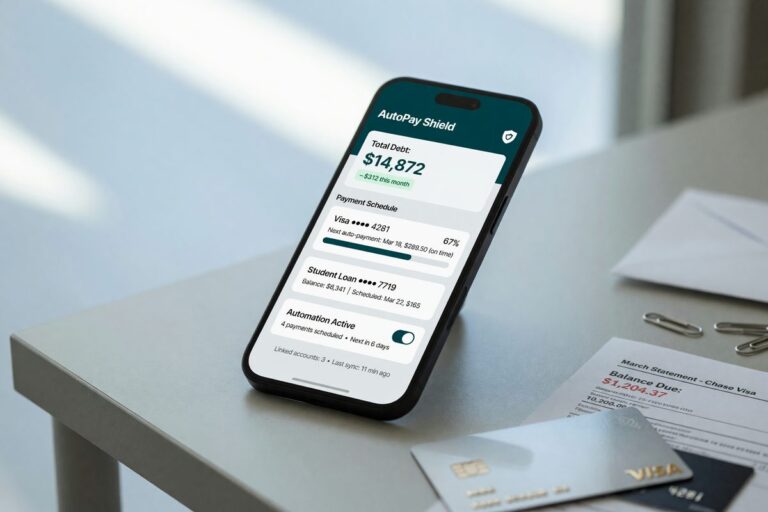

Automated fintech debt repayment pays off if you earn stable income and carry $5,000+ in debt—but app fees can erase savings faster than you think. See when it's worth it.

BNPL hit $156.7B in 2025 and earned wage access costs $1–$5 vs. 400% APR payday loans. See which fintech credit products match your actual cash problem.

Only 55% of single parents have savings for emergencies. See how fintech tools let you build a starter fund and tackle debt simultaneously without erasing progress.

Payroll advances cost less for one emergency, but repeat users hit APRs over 100%. Personal loans win if you need $500+ or multiple advances yearly.

43% of digital lenders now use cash flow, rent payments, and payroll data alongside credit scores. See how these alternative signals unlock approvals for credit-invisible borrowers.

Mainstream lenders auto-deny recent bankruptcies, but secured products and credit unions with manual review still approve. See which platforms say yes and what rates to expect.

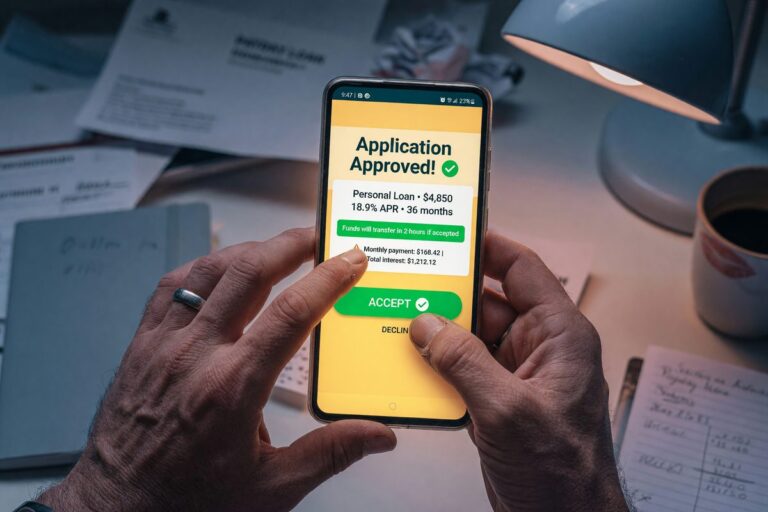

AI loan matching platforms deliver the biggest payoff for borrowers under 680 FICO or those comparing 10+ lenders at once. The real difference: whether you get genuinely different offers or just re-ranked duplicates.