How a Cosigner With Strong Credit Actually Moves the Interest Rate on a Personal Loan

A strong cosigner can drop your personal loan rate by 4 to 10 points—potentially saving thousands. Here's exactly how lenders reprice risk when you add one.

A strong cosigner can drop your personal loan rate by 4 to 10 points—potentially saving thousands. Here's exactly how lenders reprice risk when you add one.

Personal loan APRs hit 36% and reverse mortgage rates average 7.5% — here's why fixed income and debt-to-income rules push rates higher for borrowers over 60.

Standard rate locks cost nothing extra but won't capture drops. Float-downs run 0.25–1.00% but pay off in falling markets—if you do the math first.

When a balloon mortgage matures, 80–90% of your original balance comes due at once—and refinancing at higher rates can raise your monthly payment by $600 or more.

Unsecured loans average 12–21% APR vs 7–9% for secured loans — a gap that can cost thousands over five years. Here's how to choose the structure that actually saves you money.

Bridge loans typically run 8.5%–12.5% annually—up to 4 points above prime. Here's what move-up buyers need to understand before juggling two closings.

Unemployment can push personal loan rates from 12.31% to 36%—or trigger outright denial. Here's how lenders reprice risk when your income disappears.

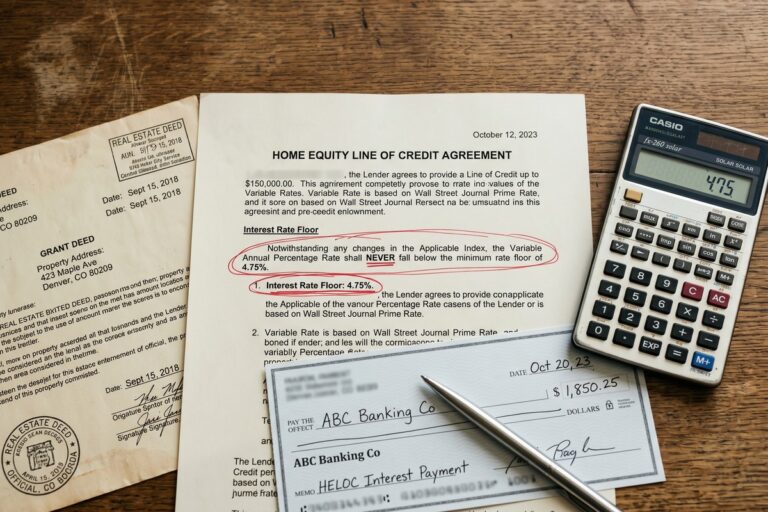

HELOC interest rate floors often cap out at 4–8% regardless of Fed cuts. See why borrowers who expected savings hit a ceiling, and how to protect yourself before signing.

Inheritance recipients are saving thousands by using lump-sum paydowns to drop 0.25%–0.75% in interest rates without refinancing. Here's how the strategy works.

Paying off a collection won't boost your mortgage rate right away. FICO 8 treats paid and unpaid collections identically, and it takes 30–90 days for updated status to reach lenders.