Fact-checked by the CapitalLendingNews editorial team

Quick Answer

A sinking fund is a dedicated savings bucket you fund incrementally for a known future expense, eliminating the need to borrow when that bill arrives. Saving $100/month for a $1,200 annual car insurance premium, for example, avoids up to $300 in interest that a credit card at 25% APR would cost if paid over 12 months.

The sinking fund budgeting strategy is one of the oldest, most reliable tools in personal finance: set aside a fixed amount each month toward a specific, predictable expense so the money is waiting when the bill arrives. The concept predates consumer credit cards by centuries, but it has never been more relevant. According to Bankrate’s 2026 Emergency Savings Report, only 47% of Americans have sufficient liquidity to cover a $1,000 emergency expense, which means most households are one predictable bill away from reaching for a credit card.

The gap between “knowing a bill is coming” and “having the money ready” is exactly where consumer debt is born. This guide explains how sinking funds work, how they differ from emergency funds, which expense categories deliver the biggest debt-avoidance payoff, and how to build a system that runs on automation rather than willpower.

Key Takeaways

- Only 47% of Americans have enough liquidity to cover a $1,000 emergency expense, leaving the majority vulnerable to high-interest borrowing for predictable costs (Bankrate, 2026).

- 24% of U.S. adults have no emergency savings at all, making a sinking fund the first real financial buffer many households will ever build (Bankrate, 2026).

- The national average credit card balance among cardholders who carry debt is $7,886, much of it driven by predictable expenses that a sinking fund would have covered (LendingTree citing Federal Reserve Bank of New York, Q3 2025).

- A $1,200 annual insurance premium saved at $100/month avoids an estimated $180 to $300 in interest that a credit card at 18–25% APR would add over a 6–12 month payoff window.

- 58% of U.S. adults report having the same or less emergency savings than a year ago, signaling that ad-hoc saving is failing at scale and a structured method is needed (Bankrate, 2026).

In This Guide

- What Is a Sinking Fund, Really?

- The Debt-Free Math: How Sinking Funds Replace Borrowing

- Sinking Funds vs. Emergency Funds: Know When to Use Each

- High-Impact Categories Most Households Overlook

- How to Build Your Sinking Fund System in Four Steps

- Mistakes That Undermine Sinking Funds (and Quick Fixes)

What Is a Sinking Fund, Really?

A sinking fund is a savings account or sub-account earmarked for one specific future expense, funded by regular contributions until the target amount is reached. Think of it as prepaying a bill in installments, on your own timeline, before the invoice arrives. The car registration due in October, the roof repair you know is coming in two years, the holiday gifts you buy every December without fail: each one is a candidate.

Where the Term Comes From

The phrase originates in corporate and government finance, where sinking funds were established to retire bond debt over time, preventing a single massive outlay at maturity. The Investopedia definition of a sinking fund traces this institutional use back to 18th-century Britain. The household version borrows the same logic: smooth out an irregular cash-flow spike by spreading the cost across many smaller, manageable periods.

How It Differs From a General Savings Account

A generic savings account is a pool. A sinking fund is a labeled bucket with a specific target amount and a deadline. That distinction matters behaviorally. When money sits in a general account, it competes with every other financial impulse. A named fund with a balance tracker changes the psychology: you can see exactly how close you are, and withdrawing from it for something unrelated feels like a genuine violation of a rule you set yourself.

The sinking fund concept is more than 300 years old. The British government used a formal sinking fund in 1717 to manage war debt, proving the strategy’s power to convert large obligations into predictable small payments.

Most banks and credit unions now support multiple sub-accounts or “savings buckets” under a single login, making the mechanics simple. The Federal Deposit Insurance Corporation (FDIC) insures deposits up to $250,000 per depositor per institution, so these sub-accounts carry the same protection as any standard savings account.

The Debt-Free Math: How Sinking Funds Replace Borrowing

Here’s the thing: the math on avoiding credit card interest is far more compelling than most budgeting guides show. Consider a single, concrete example.

You owe a $1,200 annual car insurance premium. If you charge it to a credit card at 20% APR and pay it down at roughly $110 per month, you will pay the balance off in about 12 months and spend approximately $120 to $130 in interest. Push the APR to 25% with minimum payments only, and the total interest climbs above $250. By contrast, saving $100 per month for 12 months in a high-yield savings account paying around 4.5% APY generates roughly $27 in interest income while you save, and the bill costs you exactly $1,200 on the day it is due. The difference between those two paths is $150 to $280 on a single annual bill.

Multiply that logic across four or five recurring expenses annually, and the sinking fund budgeting strategy can realistically keep $600 to $1,000 per year out of the hands of credit card issuers. For households already carrying the national average balance of $7,886 in credit card debt, redirecting even a portion of those interest payments toward debt reduction accelerates payoff significantly.

Saving $100/month for a $1,200 annual car insurance premium in a 4.5% APY high-yield account earns roughly $27 in interest over 12 months. Charging that same premium to a 25% APR credit card and paying it off over 12 months costs an estimated $150 to $300 in interest. The net difference: $177 to $327 per year, per expense.

Sinking Funds vs. Emergency Funds: Know When to Use Each

These two tools are frequently confused, but they serve entirely different functions in a personal finance system. An emergency fund covers unknowns: job loss, a medical event, a surprise repair. A sinking fund covers knowns: bills and purchases you can see coming on the calendar. The distinction shapes how each fund is sized, accessed, and replenished.

Side-by-Side Comparison

| Feature | Emergency Fund | Sinking Fund |

|---|---|---|

| Purpose | Unplanned, unpredictable expenses | Planned, predictable future expenses |

| Target Size | 3–6 months of living expenses | Exact cost of the target expense |

| Access Rule | Only for true emergencies | Fully accessible when the expense arrives |

| Replenishment | Rebuild after withdrawal | Restart contributions after withdrawal |

| Number of Accounts | One | One per expense category |

| Typical Monthly Contribution | Fixed until target is met | Target amount divided by months to deadline |

The danger of conflating the two is real. Raiding an emergency fund to pay for a predictable home repair leaves the household exposed if a genuine crisis arrives shortly after. Conversely, treating a sinking fund as a backup emergency account encourages under-saving in both categories. Both funds can coexist in the same bank app as separate sub-accounts; the labels do the heavy lifting.

If you are still building your emergency fund while also starting sinking funds, consider the guidance in this breakdown of how to prioritize saving versus debt payoff, which addresses the sequencing question directly.

High-Impact Categories Most Households Overlook

Four expense categories consistently ambush household budgets because they arrive infrequently but cost hundreds or thousands of dollars at once. Getting these into dedicated sinking funds first delivers the fastest debt-avoidance results.

Annual and Semi-Annual Bills

Car and homeowners insurance premiums are the clearest examples. Many insurers offer a modest discount for paying annually, but only households with a funded sinking fund can take advantage of it. A $1,800 homeowners premium, saved at $150/month, is $150 per month you never have to put on a credit card. The same logic applies to property tax installments, professional license renewals, and subscription bundles billed once per year.

Vehicle Maintenance and Home Repairs

The AAA’s annual vehicle cost data consistently shows that routine maintenance including tires, brakes, and oil changes averages well over $1,000 per year for most drivers. A sinking fund of $85 to $100 per month covers that without a single trip to the credit card. For home maintenance, a widely cited rule of thumb from housing economists suggests budgeting 1% to 2% of home value annually for upkeep. On a $350,000 home, that is $3,500 to $7,000 per year. A dedicated home repair sinking fund of $300/month captures the lower end of that range.

One gap most budgeting guides skip: these targets should be adjusted annually for inflation. Home repair costs in particular have tracked above general inflation since 2021. Reviewing your sinking fund targets each January and bumping them by 3% to 5% to account for rising material and labor costs is a simple discipline with real payoff over time.

Seasonal and Gift Expenses

Holiday spending is entirely predictable and entirely underfunded by most households. The National Retail Federation’s holiday spending research reports that average holiday spending per household runs well above $800 annually. Saving $70/month starting in January means December arrives with over $840 already set aside. Pet care, annual vacations, and family celebrations follow the same math.

How to Build Your Sinking Fund System in Four Steps

Start with last year’s bank and credit card statements. Pull up 12 months of transactions and flag every expense that was not a regular monthly bill: the car registration, the dentist visit, the holiday gifts, the annual software subscription. Total them by category. This exercise typically reveals $3,000 to $6,000 in annual expenses that felt like surprises but were entirely foreseeable.

Step 1: Identify and Prioritize Your Categories

From your spending audit, rank categories by two criteria: the size of the annual expense and the likelihood you would borrow if the money was not ready. Car insurance and vehicle maintenance usually top both lists. Start with two or three categories, not ten. Spreading thin across too many funds is a common error covered in the next section.

Step 2: Calculate Monthly Contributions

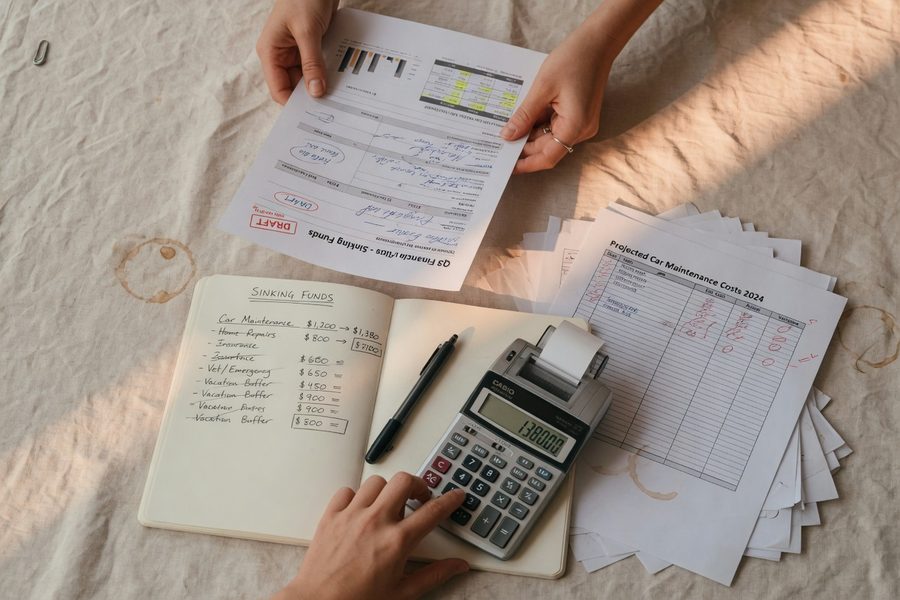

The math is straightforward. Divide the annual target by the number of months until you need the money. A $600 tire replacement expected in 8 months requires $75/month. A $2,400 vacation in 18 months requires $133/month. Write both numbers down before opening any accounts, so the budget impact is visible before you commit.

Step 3: Choose Your Storage and Automate

Here’s the thing: the account type matters less than whether it is automated. A high-yield savings account at an online bank currently paying 4% to 5% APY is the best option for most people, because the yield is meaningful and the funds are slightly less accessible than a checking account. Banks like Ally Financial, Marcus by Goldman Sachs, and SoFi all offer bucket or sub-account features that allow multiple named sinking funds under one login. Set automatic transfers to hit each sub-account on the same day as your paycheck. Manual transfers fail.

People who prefer to avoid adding another app can achieve the same result with a simple spreadsheet tracking a single high-yield account, using a running balance column per category. Low-tech works fine, as long as the automation is intact.

Step 4: Review Quarterly

Once per quarter, spend 15 minutes checking that each fund is on pace for its target date and that the targets themselves still reflect current costs. If car repair costs jumped in your area, bump the monthly contribution. If you spent less on gifts than expected, redirect the surplus. The review does not need to be detailed; it just needs to happen.

Open each sinking fund sub-account with a label that names the exact expense and the target date, for example “Tires, March 2027–$650.” Specificity makes it psychologically harder to raid the account for unrelated spending, and it eliminates ambiguity during quarterly reviews.

If irregular income makes consistent monthly transfers difficult, you are not alone and the challenge is real. Freelancers and gig workers often find percentage-based transfers more sustainable than fixed dollar amounts. Depositing 10% to 15% of every payment received into a combined sinking fund pool and allocating from there prevents the fund from stalling during low-income months. For a broader look at managing money during income gaps, this guide on building an emergency fund while paying debt covers the sequencing and automation tactics in detail.

Mistakes That Undermine Sinking Funds (and Quick Fixes)

The most common failure mode is underestimating the target. Households tend to recall the last time they paid a bill rather than adjusting for what it will cost next year. Home insurance premiums rose significantly in many U.S. states between 2023 and 2025; a sinking fund built on a two-year-old premium is already underfunded. Pull the actual current renewal notice, not a memory of the old one, when setting targets.

Treating the Fund as Flexible Spending

A sinking fund with a named purpose is only effective if that purpose is respected. Dipping into the “car repairs” fund for an impulse purchase is functionally the same as not having the fund at all. The fix is structural: keep sinking funds at a different bank from your checking account. The added friction of transferring between institutions creates a pause that most impulsive withdrawals do not survive.

Starting too many categories simultaneously is equally damaging. A household that opens eight sinking funds with $20 contributions each will find that none of them reach a meaningful balance before an expense arrives, and the exercise feels like a failure. Two well-funded categories beat eight underfunded ones every time. Add categories only after the first two are consistently on track.

One honest concession: this strategy depends on having surplus cash flow after essential bills. For households where income barely covers fixed expenses, building even a single sinking fund requires finding a spending cut first. That may mean a genuine trade-off, not just an optimization. If high-interest debt is already consuming significant cash flow, consider whether understanding how loan term length affects total interest cost could free up room in the budget before adding new savings commitments.

Households that automate even two sinking fund transfers report a measurable behavioral shift: they stop mentally categorizing annual bills as “unexpected.” That shift alone reduces emergency fund withdrawals and new credit card charges for predictable expenses.

For households already in debt, sinking funds and debt payoff are not mutually exclusive. A small sinking fund for car maintenance running alongside a debt snowball prevents the single worst pattern: paying down a card, then immediately charging a tire replacement back onto it. Sinking funds plug the leak that debt payoff strategies often ignore. If you are weighing borrowing versus saving as you pay down debt, the comparison of personal loans versus cash-out refinancing for financial emergencies is a useful parallel read for when the unexpected does occur despite best planning.

Frequently Asked Questions

How is a sinking fund different from a savings account?

A savings account is a general-purpose pool; a sinking fund is a labeled, purpose-specific bucket with a defined target and deadline. The difference is behavioral as much as mechanical. Naming a fund and assigning it a specific expense makes spending it for other purposes feel like a rule violation, which most general savings accounts do not.

How many sinking funds should I have?

Start with two to three. Most financial planners recommend identifying your top categories by annual dollar amount, funding those fully first, then expanding. Four to six active funds is a comfortable ceiling for most households before the tracking burden outweighs the benefit.

Should I keep sinking funds in a high-yield savings account?

Yes, for most people. A high-yield savings account paying 4% to 5% APY as of mid-2026 generates meaningful interest on balances that would otherwise sit idle in a checking account. Many online banks including Ally, Marcus by Goldman Sachs, and SoFi offer free sub-accounts or buckets, making it straightforward to keep multiple labeled funds in one place.

Can sinking funds coexist with an active debt payoff plan?

They can, and in most cases they should. A sinking fund for car maintenance or insurance running alongside a debt snowball or debt avalanche prevents the cycle where a paid-down card gets immediately recharged by a predictable expense. Even a $50/month contribution to a vehicle maintenance fund reduces the risk of derailing debt progress when tires wear out. For context on how savings levels interact with borrowing costs, this explanation of why high savings balances do not automatically lower your loan rate is worth reading.

What if my income is irregular and I cannot commit to fixed monthly transfers?

Percentage-based contributions work better than fixed dollar amounts for variable-income earners. Depositing 10% to 15% of every incoming payment into a sinking fund pool, then allocating proportionally to each category, keeps the system moving without requiring a predictable paycheck. Automation by percentage rather than fixed dollar amount is available through most modern budgeting apps and some bank transfer tools.