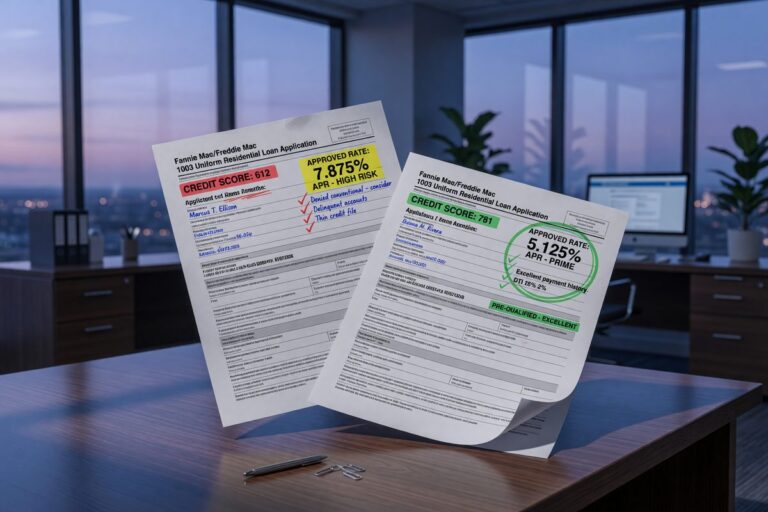

How Debt Consolidation Before Applying for a Mortgage Can Quietly Lower Your Rate

Consolidating high-interest debt before a mortgage application can lower your rate by improving DTI and credit utilization—even lenders price in 0.25% steps for modest credit improvements.